Weekly Global Credit Wrap 2 Dec 2022

Yields lower, inflation readings lower, US IG spreads hit key level

*TLDR*

MACRO

Global yield curve became inverted, first time this millennium.

BHP Says China Growth Will Help Offset Wider Global Slowdown

2yr UST yields dropped to a 2 month low of 4.23% before ticking up post NFP

US IG Corp spreads at key resistance level, off which spreads have widened previously

NFP summary for November - Wages higher, jobs higher, unemployment in line

U.S. manufacturing sector contracted in November

INFLATION

US Core PCE Inflation data for October came in below expectations

US Prices paid component of ISM hit 30 month low in November

Eurozone Inflation eased slightly in November for first time since June 2021

Australia sees unexpected drop in October inflation

Wage negotiations by Unions putting upwards pressure in Spain/US/UK

NEW ISSUES/TENDERS

Record November for European Issuance

GBP - Low issuance and high amount of tenders/maturities provide supportive technical

European Utilities back in the market - EDF + Orsted issued Corporate Hybrids

Container names active with corporate actions

LATAM Nations Tendering and issuing

COMMODITIES

Europe on course to end winter with plenty of Gas

UK's Labour Party says Tories could have gone further with Windfall tax

FINS

Recent new Bank AT1s are up anywhere from 2 to 8pts

Blackstone limits withdrawals from large property fund

IG

LQD Bond ETF - Saw biggest one day outflow since inception ($3bn)

Netflix stands by limited theatrical releases

HY

New CLO sales since mid-September have topped €5bn

KKR executes a buyout with no debt for French Insurance Broker April

Energy M&A - Eni said to pursue $5bn Neptune Energy

Aroundtown Hybrids non-call and talk of possible coupon deferral, meanwhile other European RE firms sort out their finances ->

Adler Agrees on ‘Expensive, Complex’ Debt Deal With Bondholders

Brookfield to buy 49% stake in Swedish SBB's education unit for $870m

EM

Turkish cenbank's net FX reserves rise to $19.51 bln

Pakistan Central Bank Says It Paid $1 Billion-Dollar Bond

South Africa political volatilty causes ZAR to weaken

CHINA

China to allow home quarantine for some infected with COVID

RATINGS

Lots of updates this week

ESG

More funds get downgraded for ESG reasons

*MOVES OVER 5D*

CDS Indices - Xover 10bps tighter to 443bps, other than that most other indices were flat/slightly tighter.

Cash Credit Spread Indices - EM rallied well with EM aggregate 13bps tighter to 354bps and EM HY $ spreads tightening 27bps, LATAM perfomance is thought to be driving this performance. European IG tightened 5bps to 177bps. US Corp IG spreads are sitting on a key level (~130bps) and recent history suggests a bounce higher off these levels, but its hard to ignore the “year end” effect where spreads could grind tighter still.

November performance for credit assets was broadly positive based on DB’s charts.

In terms of other notable market measures this week:

JPY hit 134 after hitting 150 in October (Weak Dollar + Risk on rally)

Vix traded below 20 (subdued volatility)

*MACRO*

Global yield curve became inverted this week - BBG

Extract - “The average yield on sovereign debt maturing in 10 years or more has fallen below that of securities due in one-to-three years, according to Bloomberg Global Aggregate bond sub-indexes. That has never happened before based on data going back to the beginning of the millennium. “

Datatrek opines that Credit Spreads are not currently a useful indicator for stocks

Extract - “Corporate credit markets, long the asset class of choice for people looking for clean insights into the economy, have turned as murky as everything else in 2022…Most recently, spreads on investment-grade bonds reached their ceiling for the year at roughly 165 basis points on Oct. 12, while the S&P 500 touched 2022’s low just a day later. Similar episodes occurred in late June into July, March and early January.”

BHP Says China Growth Will Help Offset Wider Global Slowdown - RTRS

Extract - “BHP Group Ltd Chief Executive Mike Henry told the Reuters NEXT conference on Wednesday that "all fundamentals are in place" in China for continued economic growth over the next 20 years. China, the world's second biggest economy, accounts for more than 50% of global demand for raw materials.”

ECB’S Lagarde still committed to bring inflation down to medium-term target

Extract from ECB speech last week- “We are committed to bringing inflation down to our medium-term target, and we are determined to take the necessary measures to do so. We expect to raise rates further to the levels needed to ensure that inflation returns to our 2% medium-term target in a timely manner.”

European and UK house prices continue to cool off

UK House prices fell 1.4%, more than the 0.4% anticipated by economists, according to Nationwide BS data.

*NEW ISSUES / TENDERS*

November 2022 new issue recap

€130bn in new IG bond sales in Europe including UK, setting a new record for the month of November.

Corporate Hybrid market strength as Air France, EDF, Orsted and Telefonica and came to market with high coupon, high reset issuance

Corporate US IG market posted $100bn of issuance

Financials - Over €50bn issued in Europe, lots of issuance to prefinance upcoming calls and exchange offers from smaller institutions. Recent high coupon national Bank AT1 that have been issued are up anywhere from 2-8 points. Insurance bond issuance continues to lag.

Notable EUR/GBP Issuance / Tenders

Utils:

Orsted raised €500m Green Corporate Hybrid 1000NC6 to yield 5.25% after tendering for its €700 6.25% hybrid capital securities due 3013, callable 2023

EDF raised €1b PerpNC6 Hybrid at 7.5% - Which saw its short dated Corporate Hybrids rally on the expectation of reduced call risk.

GBP / Banks:

Investec Plc raised a new T2 bond (Investec 9.125% 2033) rated IG one agency callable in 2027. It had previously invited holders of its £420m fixed rate reset callable subordinated notes due 2028 for a cash tender offer.

Natwest raised a 10.5NC5.5 T2 at Gilts + 420bps (Natwest 7.416% 2033)

Orange: £386.6M outstanding 2023 Hybrid Notes Accepted, small rump issue left over.

TFL (Transport for London) tender for 7 series of notes targeting to buy back up to £800 million of notes from holders via tender offers (BBG)

Other IG:

Balder to Buy EU222.5m of 2023 Notes in Tender Offer (Real Estate)

Vodafone launches $2.3 billion buyback offer for 2028 notes

Nissan gets $1.44 bln green loan for zero-emission mobility investments | Reuters Extract - “Nissan Motor Co has signed a 200bn-yen ($1.44 billion) green loan agreement to fund zero-emission mobility investments. The syndicated loan was arranged by Mizuho Bank and MUFG Bank with contract periods of five and seven years, it said in a statement. The funds will be used for research and development of zero-emission vehicles, components for electric vehicles, and other carbon-neutral initiatives, Nissan added.”

Containers: Seaspan and Danaos - Tender / Bondholder meeting announcements

Listed Container name Danaos continues to prioritise de-leveraging. Seems similar story playing out in so many sectors, i.e corporates being good citizens with respect to balance sheet management while macro backdrop for the sector worsens (e.g Containers/US Homebuilders).

Meanwhile, Atlas Corp whose Container subsidiary Seaspan announced a bondholder meeting with a proposal for an 8% amendment fee in exchange for foregoing the 101 price put option, please see the release for full details, exact wording. Sidenote, European based Container operator CMA-CGM stated it had $17.8bn of liquidity in its update last week.

Notable EM Issuance / Tenders

El Salvador will tender some of its 2023 and 2025 dollar bonds - PRNewsWire

Mexico Government to Buy Back Up to 1.2B Euros in Bonds Dec. 29 - Mexico’s Finance Ministry will offer to buy back up to 1.2 billion euros of its 1.375% bonds due January 2025 on December 29, according to a statement. Bond buybacks this year will diminish debt amortization payments in 2025 by 70% (BBG)

Colombia raised $1.36bn 10 year bonds to yield 8.125% - Colombia is split rated (Baa2/BB+/BB+). Part of the proceeds was to pay for LME transactions to pay off all or part of Colombia 2.625% 2023s, 4% 2024s, 8.125% 2024s.

Turkey raises $2bn in tap of 9.875% January 2028 notes. Re-offer at 9% / $103.46

*INFLATION*

US Core PCE Inflation data for October came in below expectations

Prices paid component of ISM hit 30 month low in November

Eurozone Inflation eased slightly in November for first time since June 2021

German, Italian and Spanish inflation fell in the month to the surprise of forecasters. However it seems a lot of the move was due to base effects in energy and the price drop in recreational activities following the end of the Summer as per ING:

"Available regional data suggest that the drop in headline inflation was mainly driven by energy base effects and a drop in prices for leisure and entertainment after the Fall vacation period," Carsten Brzeski, global head of macro at ING, said in a note to clients. "Food price inflation still increased."

More from EN: “But it [inflation] remains in the double digits as rising food prices and high energy bills continue to squeeze budgets. Annual inflation is expected to have reached 10 per cent in November, down from 10.6 per cent in October, according to the latest estimate of the EU's statistics body Eurostat. Driven by energy and food, inflation had reached an all-time high since November 2021 every month. The situation had worsened since the spring with market disruptions related to the war in Ukraine.

Spanish inflation fell again sharply in November - ING

Australia sees unexpected drop in October inflation - ING

Extract - “Against expectations for an increase, both headline and core inflation rates for Australia's monthly inflation series fell in October. The headline inflation rate fell from 7.3% year-on-year in September to only 6.9% YoY in October. The monthly trimmed mean index inflation rate also fell slightly, to 5.3%YoY from 5.4%….The particular recreation sub-component that provided the biggest impact to the headline rate was holiday accommodation and travel. The Australian Bureau of Statistics (ABS) says of this component "The monthly fall in holiday travel and accommodation was driven by the conclusion of the school holiday period and the end of the peak tourist season for travel to Europe and America".

Prices for chicken breasts in the US have plunged ~70% since first week of June - WSJ via Yahoo Finance

Extract - “After a year in which supply-chain issues and high demand pushed the price of chicken up, poultry lovers are finally hearing some good news: The cost of chicken is dropping. Since the first week of June, the price of chicken breasts has decreased about 70 percent, according to data cited in a new Wall Street Journal report. And overall, after rising a whopping 14.5 percent in the year through October, chicken prices started to fall 1.3 percent last month, CNN noted.” Time to switch up Turkey for Chicken at Christmas? :)

Biden Signs Legislation Preventing Railroad Strike - WSJ

Extract - “President Biden on Friday signed legislation to prevent a nationwide strike by railroad workers, the last step in resolving a long-running dispute between workers and major freight railroads…The five-year [wage] agreement, which replaces a contract that covers the period from 2015 to 2019, offers railroad workers a 24% increase in wages from 2020 through 2024. It allows for one additional paid day off, on top of existing vacation and paid time off. Workers have been working under the terms of the old contract and will get back pay.”

Spanish Banks, Unions Agree to Raise Salaries by 4.5% in 2023 | RTRS

Extract - “Spanish banks and the country's two biggest unions on Tuesday reached an agreement to raise wages of employees in the sector by 4.5% in 2023 compared to 2022, the banking association AEB and the union CCOO said in a statement. Banks and unions were trying to reach an agreement with the banking associations to offset the loss of purchasing power caused by steep rates of inflation.”

Heineken plans to raise Beer prices due to higher input costs - BBG

*COMMODITIES*

Europe on course to end winter with plenty of gas: Reuters’ Kemp

Extract - Europe's gas inventories are on course to end the winter of 2022/23 at one of the highest levels on record - if prices stay high and provided pipeline deliveries from Russia continue. European Union and United Kingdom (EU28) stocks amounted to 1,061 terawatt-hours (TWh) on Nov. 26, a record for the time of year, storage data from Gas Infrastructure Europe (GIE) shows.

Germany, Poland aim to secure oil supply to Schwedt refinery, avoid Russian Oil | RTRS

Extract - “Germany and Poland have signed a deal aimed at securing the supply of oil to the Schwedt refinery after ending reliance on Russian oil, Germany's economy ministry said on Thursday. Berlin aims to eliminate imports of oil from Russia by the end of the year under European Union sanctions and has for months been working with Poland to try secure supply for Schwedt, which provides 90% of Berlin's fuel.”

UK Labour Party Sees £17 Billion Hole in Sunak’s Energy-Windfall Tax - BBG

Extract- “Labour - which advocated the policy before the Conservative government adopted it -- on Tuesday said the government could be raking in billions more in tax revenue by backdating the levy to January, scrapping tax breaks Sunak introduced for firms that invest in oil extraction in the North Sea, and raising the rate. “Labour would be making fairer choices -- fairly taxing the windfall profits of war, instead of diving into working people’s pockets first,” Shadow Chancellor Rachel Reeves said in a statement.”

*US*

Good macro economic summary for the US last week from WH Advisor:

NFP summary for November - Wages higher, jobs higher, unemployment in line

One of the interesting points the pivot away from goods; Department stores jobs down 21.8k, warehousing and storage down 12.5k, couriers down 12.4k. h/t @nick_bunker, economic research director at Indeed.com

The strong labour market data for now runs contrary to the easing narrative in markets and gives the Fed plenty to think about. Axios summarised NFP well, but for a more detailed post on NFP check out the one from Macro Alf.

U.S. manufacturing sector contracts in November - ISM | RTRS

Extract - “U.S. manufacturing activity contracted for the first time in 2-1/2 years in November as higher borrowing costs weighed on demand for goods.. The Institute for Supply Management (ISM) said on Thursday that its manufacturing PMI fell to 49.0 last month. That was the first contraction and also the weakest reading since May 2020, when the economy was reeling from the initial wave of COVID-19 infections, and followed 50.2 in October.” Handover from high inflation to recessionary conditions continues.

Black Friday online sales top $9 billion in new record - CNBC

Extract - “Consumers spent a record $9.12 billion online shopping during Black Friday this year, according to Adobe. Overall online sales for Black Friday were up 2.3% year-over-year. Buy Now Pay Later payments increased by 78% compared with the past week, beginning Nov. 19, as consumers continue to grapple with high prices and inflation.”

Meta Platforms to vacate 250,000 sq, feet of its NYC office space - MarketWatch

The contraction of Tech spend continues to reverberate across different markets (e.g. employment/real estate).

Extract - Facebook’s parent company Meta is ditching office space that it rented out at the Hudson Yards complex in New York City — the latest sign of belt-tightening at the Silicon Valley-based tech giant that recently laid off thousands of employees. Meta will vacate 250,000 square feet of office space at 30 and 55 Hudson Yards, though it will maintain the bulk of its footprint — some 1.2 million square feet — at the unfinished 50 Hudson Yards, a source familiar with the matter told The Post. Meta has notified the building’s landlord, Related Cos., of its plans not to renew its lease at 30 and 55 Hudson Yards at the end of 2024. Meta told investors last month that it expects to take a $2 billion charge in consolidating its office space.”

*FINANCIALS*

Pershing Square Holdings Nov. Net Performance +8.2%

Compared to 5.6% Return for S&P 500 for same period.

Blackstone's $69 bln REIT curbs redemptions | RTRS

Extract - “Blackstone Inc (BX.N) limited withdrawals from its $69 billion unlisted real estate income trust (REIT) on Thursday after a surge in redemption requests, an unprecedented blow to a franchise that helped it turn into an asset management behemoth. The curbs came because redemptions hit pre-set limits, rather than Blackstone setting the limits on the day. Nonetheless, they fueled investor concerns about the future of the REIT, which makes up about 17% of Blackstone's earnings.”

RBC to Pay $10.1 Billion for HSBC Unit - WSJ

HSBC continues its planned shift toward Asia and the Middle East by selling its Canada Unit. Extract from WSJ: “Royal Bank of Canada said it would pay US$10.1 bn for HSBC Holdings PLC’s Canadian operations, a move meant to position Canada’s biggest bank to expand during an expected immigration surge. As part of the deal, it will refer clients who are moving to Canada to RBC, said Dave McKay, RBC’s chief executive. Canada’s government has said it expects to boost immigration to 500,000 people a year by 2025, up from 405,000 last year. “

*IG*

LQD Bond ETF - This week saw biggest one day outflow since inception ($3bn) | BBG

Extract - “More than $3 billion exited the $36 billion iShares iBoxx $ Investment Grade Corporate Bond ETF (ticker LQD) on Monday, Bloomberg data show. That’s the biggest one-day outflow since the fund’s inception in 2002.”

This story has been painted in a lot of ways, but I’m yet to hear from someone in the Bond ETF world comment on whether there was some sort of technical quirk to this outflow. The iShares LQD website reveals that the effective duration on this instrument is currently 8.6 and the weighted average maturity of the portfolio is 13.2 years. Duration has had one heck of a rally that has seen an 80-85bps rally in the 10y and 30 yr UST Treasuries off the highs. So the sale could be as simple as a large market participant expressing a view to tactically reduce Investment Grade exposure after a strong rally (LQD +10% total return since 20th October) to lock in a gain for 2022. With that last strong NFP report published on 2nd December and inflation still being at elevated levels, it could have been an astute move ahead of a possible steepening of the curve. The move could also have been a large RIA switching into a cheaper ETF product for a similar exposure.

Side note #1 : LQD is still down 15% YTD (total return).

Side note #2: BBG commented that November 2022 saw long dated credit post a 10% return.

Brookfield to buy 49% stake in Swedish SBB's education unit for $870 million | RTRS

This is interesting not only for SBB but also for the whole European Real Estate sector which is in net selling mode as companies look to reduce debt loads to counteract higher funding costs on their existing debt. Firms like Brookfield which are long cash are likely able to extract attractive terms as the dynamics are stacked in buyers’ favour.

Extract - “Brookfield Asset Management will buy a 49% stake in the education portfolio of Sweden’s SBB , for 9.2 billion Swedish crowns ($870.42 million) in cash, the Swedish real estate company said on Wednesday. Brookfield, through its infrastructure fund Brookfield Super-Core Infrastructure Partners, will also make two additional earn-out payments of up to 1.2 billion crowns in cash, SBB said in a statement.”

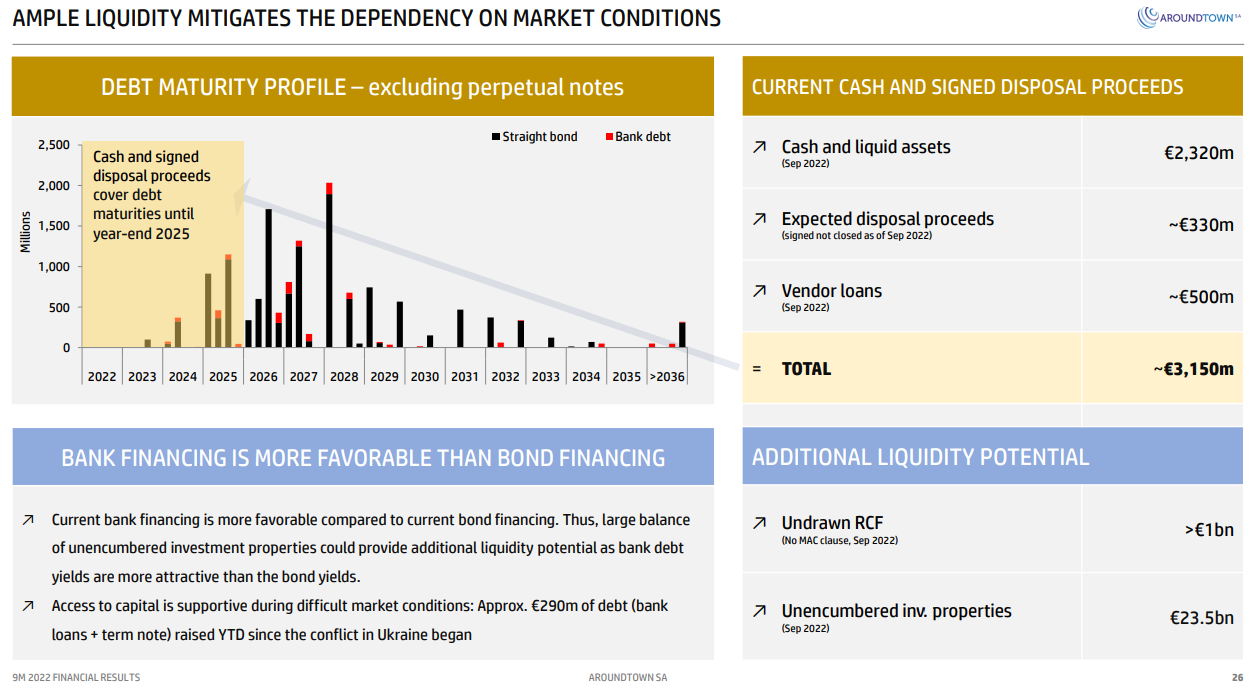

Aroundtown reported Q3s, non-call of hybrid and possible coupon deferral

European Real Estate firm Aroundtown’s Q3 update generated volatility in its own bond prices and the European RE sector by not calling one of its bonds and stating that it may consider the option to defer coupon payments closer to the respective interest payment date of the bond. According to the company, “the decision reflects Aroundtown’s strategy in the current volatile market environment to maintain high liquidity balance, low LTV-ratio and high headroom to its debt covenants.“ Separately, Aroundtown’s subsidiary Grand City Properties also announced a non-call of its 2023 Corporate Hybrid.

Source: Investor presentation

The main surprise to credit participants was the mention of a possibility of a coupon deferral. Prior to the update, debt of Aroundtown was already trading at cash prices in the 50s-75s reflecting a high probability of non-call, but bonds dropped further post announcement.

The company reported €2.3bn cash & liquid assets, >€1bn undrawn RCF, no MAC, and €23.5bn of unencumbered assets. Arguably the decision to conserve cash and liquidity in what could be a tough macro environment in Europe in 2023 was the right thing to do, but clearly it comes at a cost to Corporate Hybrid holders. This despite stating that the company is “committed to retain perpetual notes as part of its long-term capital structure.”

Source: Investor presentation

Toyota's Oct global vehicle production up 23%, above its target | Reuters

Extract - “Toyota Motor Corp reported on Tuesday a 23% rise in October global vehicle output, beating its own target for a third month in a row, as the industry strives to get past persistent chip shortages that have hobbled production.”

Toyota has been one of the best prepared of the Auto Manufacturers for the chip shortage due to its prior experience with the shortages caused by the Fukishima Earthquake and judging by the raised production target suggests some progress on supply chain shortages.

Netflix stands by limited theatrical releases - AVClub

Netflix CEO Reed Hastings re the recent Theatrical release of film Glass Onion: “It’s a promotional tactic like film festivals, and if it works well we will do more of it,” Hastings said of the film’s limited release (per The Hollywood Reporter). “We are not trying to build a theatrical business, we are trying to break through the noise.”

Rynair and Wizzair both reported strong Traffic figures this week - ThisIsMoney

Extract - “Nearly 3.7 million people flew with Hungarian low-cost airline Wizz Air during November, an increase of around 1.5 million on the same month last year, while 11.2 million travelled on a Ryanair flight, 10 per cent higher than in November 2021. The share of available seat capacity filled by customers also grew by 12 percentage points to 88 per cent at the former company and from 87 per cent to 92 per cent for the latter group.” Sidenote: Ryanair cautious on Q1, but sees strong Summer bookings - BBG

*HY / LEV LOANS*

New CLO sales since mid-September have topped €5 billion - BBG

Extract - “In Europe, Ares Capital Corp. and OakTree Capital Group sold new CLOs this month, even as other debt markets, including junk bonds, have been largely moribund. New CLO sales since mid-September have topped €5 billion ($5.2 billion).”

KKR executes a buyout with no debt for French Insurance Broker April - BBG

Extract - “KKR agreed to fund on its own the totality of the €2.3 billion ($2.4 billion) purchase price for April Group, according to people familiar with the matter. Few banks are in much of a position to extend multibillion-dollar loans for acquisitions these days, given that they’re still saddled with more than $40 billion of unwanted buyout debt on their balance sheets.”

Not the first time I’ve heard this notion of buyouts without any debt, no doubt KKR will look to borrow once debt markets have thawed a bit more. Like I pointed out last week, the WACC has gone up mainly due to the higher cost of debt, so makes less sense to load buyouts with debt at such high costs of funding.

Eni Is Said to Pursue $5 Bn Carlyle-Backed Explorer Neptune - BBG

Extract - “Deliberations are at initial stage and an official bid has not been submitted, according to the source. The Italian energy giant (ENI) is working with an undisclosed adviser to assess the feasibility of the acquisition, reported Bloomberg News, citing people involved in the matter. According to the people involved, Neptune Energy could also consider alternative transactions such as an initial public offering (IPO). The acquisition is expected to provide Eni with the opportunity to expand its natural gas business. Neptune’s owners have been working with advisers, including Goldman Sachs Group and Rothschild & Co., to gauge options for the company, including a potential sale. Owned by the China Investment Corporation (CIC), the Carlyle Group, and CVC Capital Partners , Neptune has operations in Norway, Indonesia, Algeria, and the Netherlands, among others.”

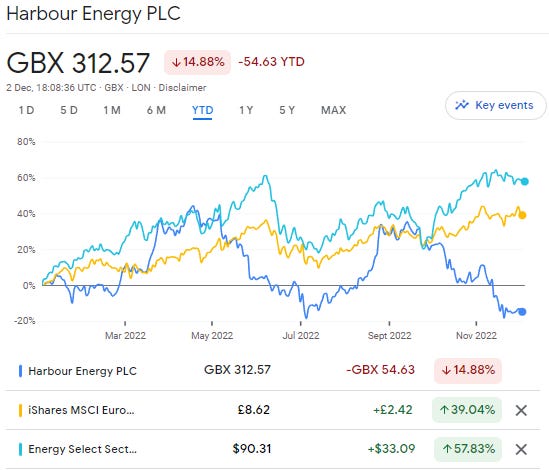

Sidenote: On the topic of E&P equities, Harbour Energy left the FTSE 100 index in the quarterly re-shuffle after only entering it recently. The announcement of a more prolonged Windfall tax and a more volatile oil price likely were the key reasons behind the move. HBR has underperformed both ESIE (iShares MSCI Europe Energy Sector ETF) and XLE (Energy Select Sector SPDR Fund) YTD meaningfully.

Vue sets sights on Cineworld - Sharecast

Extract - “Britain’s third-biggest cinema chain, Vue International, is reportedly ready to swoop on rival Vue ahead of a possible stock market flotation. Vue founder Tim Richards confirmed to The Times that the company was ready to take advantage of any opportunities that presented themselves as speculation mounts that Cineworld could be broken up. "We’ve done 14 deals in the last 20 years," Richards said. "[Mergers and acquisitions] is a part of the business we’re very good at. There are going to be opportunities for M&A activity of all sizes and scale in the next 18 months." Vue, which trails behind Odeon and Cineworld, has 91 venues across the UK and Ireland with 870 screens. Overall, it has 227 sites in nine countries with 10,000 employees.”

Copper Mountain receives bondholder approval for sale of Eva Copper Project…

Extracts - “and Australian Tenements, announces bond buyback offer. Summary of Bond Buyback Offer.

In connection with obtaining the Bondholder Approval, the Company has agreed, within 30 days after completion of the Transaction, to:

Pay a one-time amendment fee of 0.25% of the nominal amount of the outstanding Bonds, on a pro rata basis, to the bondholders; and

Make an offer to buyback Bonds for an aggregate minimum principal amount of US$87,000,000 (the "Buyback Offer") at an offered price of 103.00 per cent of the nominal amount of the Bonds (plus accrued interest on the repurchased amount).”

Adler Agrees on ‘Expensive, Complex’ Debt Deal With Bondholders - BBG

Extract - “The German landlord reached a pact with 45% of its bondholders to raise as much as €937.5 million ($976.1 million) of a secured loan to pay back the next bonds coming due, according to a statement published late on Friday. The new loan will give creditors rights over 25% of the shares, according to the statement.”

*EM / ASIA*

Turkish cenbank's net FX reserves rise to $19.51 bln | RTRS

Extract - The Turkish central bank's net international reserves rose some $760 million to $19.51 billion in the week to Nov. 25, hitting their highest since mid-February, central bank data showed on Thursday.

Pakistan Central Bank Says It Paid $1 Billion-Dollar Bond - BBG

Extract - “The nation transferred the money for the sukuk dollar bonds due Dec. 5 three days before their maturity to Citigroup Inc., which will distribute the funds to creditors, said Abid Qamar, a spokesperson at State Bank of Pakistan. The notes climbed to 98.9 cents on the dollar Friday, marking a nearly 16-cent comeback from a record low of 83 cents in October, according to indicative pricing data compiled by Bloomberg. “

Cyril Ramaphosa: South Africa leader won't resign, says spokesman (BBC)

Extract - “South Africa's President Cyril Ramaphosa will not resign despite a scandal over money stolen from his farm, his spokesman says. The row centres on claims he kept large sums of cash on his property then covered up its theft…The scandal erupted in June, when a former South African spy boss, Arthur Fraser, filed a complaint with police accusing the president of hiding a theft of $4m (£3.25m) in cash from his Phala Phala game farm in 2020.”

The Rand spiked to 17.5 from 17.0 following the news but retraced some of its losses towards the end of the week. As a side note, political volatility and inappropriate use of funds not just limited to EM, just look at the UK and the Liz Truss experience and the ongoing allegations of funds given to a House of Lords Peer for PPE…

Mexico Posts $5.35 Billion Record Remittances From Workers Abroad - BBG

Exract - “Money sent home by Mexicans who are mainly living in the US totaled $5.36 billion in October, beating analysts’ estimates of $5.11 billion and a previous record of $5.3 billion in July, according to central bank data published on Thursday.” Sidenote: This week the Mexican Peso hit a two year high but came off the highs on Friday post NFP and associated Dollar Strength.

*CHINA*

China to allow home quarantine for some infected with COVID | RTRS

This seems like a significant change, which the market picked up on and send China risk assets higher.

Extract - “China will allow some people who test positive for COVID-19 to quarantine at home, among supplementary measures to be announced in coming days, two sources with knowledge of the matter told Reuters.

Home isolation for the infected would be a significant change in China's quarantine protocols. Earlier this year, entire communities were locked down, sometimes for weeks, after even just one positive case was found. Last month, new and easier quarantine rules required just the lockdown of affected buildings.”

*RATINGS*

IG

BHP Group May Be Raised by Moody’s

S&P Upgrades AstraZeneca To 'A'; Outlook Stable 11

Fitch Affirms SBB at 'BBB-' on EduCo sale; Outlook Positive

X-S&PGR Affirms Orsted At 'BBB+/A-2'; Outlook Stable

LEG Immobilien Outlook to Negative by Moody's

Deutsche PBB Affirmed at BBB+ by S&P

Fitch Affirms Hannover Re's IFS Rating at 'AA-', Outlook Stable

Fitch Affirms Intesa Sanpaolo at 'BBB', Outlook Stable

Fitch Affirms Unicredit at 'BBB'; Outlook Stable

HY

Boparan Holdings's long-term corporate family rating was affirmed by Moody's at Caa1.

Fitch Assigns Casino, Guichard-Perrachon S.A. First-Time 'B-' Rating; Outlook Positive

Intrum Outlook to Negative by Fitch; L-T IDR Rating Affirmed

Lufthansa Upgraded to BB by S&P, Outlook Positive

EM

Sri Lanka: local debt cut by FITCH to CC

Fitch upgrades Tunisia to CCC+ from CCC as IMF deal will unlock large external support

Moody’s downgraded Tullow’s ratings to Caa1 from B3, reflecting Moody’s downgrade of Ghana’s rating to Ca from Caa2

Ghana Downgraded to Ca by Moody's, Outlook Stable

Oman Upgraded to BB by S&P

Bahrain Outlook to Positive by S&P; FC L-T Debt Rating Affirmed

Bahrain's long-term foreign currency debt rating was affirmed by S&P at B+.

South Africa Affirmed at BB- by Fitch

Eskom Holdings Outlook to Stable by S&P

*ESG*

More funds get downgraded for ESG purposes - BBG

Exract - “The asset management units of Deutsche Bank AG and BNP Paribas SA are adding to a tidal wave of ESG fund downgrades, bringing industry assets under management to have been hit by such reclassifications to well over $100 billion. BNP said it was stripping Europe’s top ESG designation from $16 billion worth of funds, while DWS Group’s reclassification will hit eight funds holding about $265 million, after announcing $2.1 billion in downgrades last week. The industry has blamed unclear rules for the chaos, as investors start to voice their anger.”