18 November 2022 Global Credit Wrap

Risk on leads to healthy issuance in Credit markets

*TLDR*

MOVES

Curve inverting - Short end selling off, long end rallying in US curve.

Duration rally supporting long dated IG Credit total returns.

Xover more than 80bps tighter MTD.

Financials rallying strongly with recent AT1 paper up 3-4pts vs new issue pricing

Rally in EM took a bit of a breather after the prior week’s strong rally

MACRO + INFLATION

Central Bankers still very much focused on bringing down inflation - e.g. Lagarde commentary this week

US PPI fell more than expected, continuing decelerating trend

UK CPI posts new cycle high, Japan core inflation posts 40 yr high

Germany’s largest labor union and employers agreed on two rounds of wage increases for industrial workers of more than 8% in total

Risk-on tone in credit is bolstering new issue credit markets in US and Europe (€45bn issuance in Europe last week)

IG

Telefonica prices high coupon EUR Hybrid, breathing life into the Corporate Hybrid market

Real estate senior bond issuance crawling back with German RE firm Vonovia pricing in Euros and tendering for front end debt with the proceeds

GBP Credit is an area of strength due to strong technicals (low supply and lots of bond tenders)

Take-up of bond tenders continues to be high as demonstrated by £1.4bn being tendered in HSBC bond tender

HY / CONVERTS

Air France and Carnival issue convertible bonds

Non bank lenders in the market with bond exchange offers - IPF and NewDay

A couple of Greek Banks issued senior paper this week

Consus Unit of Real Estate firm Adler said to be in advanced discussions regarding a secured financing

Rakuten out with a 12% yielding Junk bond, reprices Corporate Hybrid stack..

Crypto bonds update..Coinbase/Microstrategy

FINANCIALS

Nationwide CCDS - Possibility of buybacks subject to PRA authorization

ESG

Global ESG-Linked Bond Market Faces Its First Set of Penalties..

2023 Outlooks

Links to Credit outlooks from GS, MS and Pimco

*MOVES OVER 5D*

CDS Indices - Biggest moves took place in Europe with Xover (-10bps) and Sub Fin CDS (-9bps) over 5 days. Xover comfortably below 500bps and Sub Fin CDS comfortably below 200bps. MTD, Xover is tighter by 83bps followed by CDX EM (-41bps) and CDX HY (-40bps). CDX EM was 8bps wider, possibly showing some exhaustion in the rally that began before the last US CPI reading.

Cash Credit spreads - CoCos led the way here tightening 27bps on the week to +492bps. On the ground, this looks like strong outperformance of recent high coupon AT1 like the DB 10% EUR and BNP 9.25% USD trading up 3-4pts. EM HY (-26bps), EM Aggregate (-24bps), US HY(-18bps). Strangely enough European HY looks tad wider on the week, which seems a bit strange considering the move in CDS.

Bond ETFs - Biggest gainers consisted mainly of longer dated Treasury ETFs and long dated IG Corporate Bond ETFs: EDV+3.25%, VCLT+3.16%, IGLB+2.95%, BLV, +2.46%, TLT+2.04%. This makes sense since the 10y and 30 year Treasuries have rallied 45-50bps from the recent highs. Besides the inverse Treasury ETFs, Inflation Linked US Bonds and short dated Govt ETFs sold off over 5 days with modest losses: TIPS (-1.92%), IBTS (-1.63%), IBGE (-1.44%), SE15 (-1.20%), SGIL (-1.1%). The yield curve inversion going on in the US has seen short end yields sell off, impacting shorter dated Treasury strategies.

*MACRO*

Fed Balance Sheet update

2s10s yield curve inversion is a popular chart this week

US Mortgage Rates Post Biggest Drop Since 1981, Falling to 6.61% - BBG

Extract - “Mortgage rates in the US faced the biggest weekly decline in nearly 41 years, providing some relief after a rapid run-up that quickly priced out homebuyers.

The average rate for a 30-year fixed mortgage was 6.61%, the lowest level in almost two months, Freddie Mac said in a statement Thursday. Last week, the average was 7.08%.

The results reflect a change in Freddie Mac’s methodology that the company says will provide a broader, more accurate view of the mortgage market. Instead of surveying lenders, it now uses data collected by its automated underwriting system to calculate average rates. “

October US Housing Starts: Record Number of Housing Units Under Construction

From CalculatedRisk Substack: “Currently there are 928 thousand multi-family units under construction. This is the highest level since December 1973! For multi-family, construction delays are probably also a factor. The completion of these units should help with rent pressure. Combined, there are 1.722 million units under construction. This is the all-time record number of units under construction.”

ECB's Lagarde Says Rates to Rise More, May Need to Become Restrictive-BBG

Extract - “We expect to raise rates further -- and withdrawing accommodation may not be enough,” Lagarde said in a speech in Frankfurt. “Ultimately, we will raise rates to levels that bring inflation back down to our medium-term target in a timely manner.”

October volume at the busiest U.S. seaport fell to its lowest level since 2009 - RTRS

Extracts - “LOS ANGELES, Nov 15 (Reuters) - October volume at the busiest U.S. seaport fell to its lowest level since 2009 as shippers sent cargo to alternate trade gateways to avoid potential disruptions from ongoing West Coast port labor talks, Port of Los Angeles Executive Director Gene Seroka said on Tuesday. Port of Los Angles data showed that the facility handled 678,429 20-foot equivalent units (TEUs) last month - almost 25% fewer than in October last year. The biggest drag was from incoming "cargo that has shifted to the East and Gulf Coasts due to protracted labor negotiations" between West Coast port workers and their employers, Seroka said. Retailers like Walmart brought goods in months earlier than usual to ensure they had products on hand for the all-important winter holiday season.”

*INFLATION*

US PPI decelerated in October by more than expected

German Industry Faces 8.5% Pay Increase From Union Deal - BBG

Extract - “Germany’s largest labor union and employers agreed on two rounds of wage increases for industrial workers, averting the threat of strike action in Europe’s biggest economy. The IG Metall union said Friday the deal in the state of Baden-Wuerttemberg will raise pay 5.2% next year and 3.3% in 2024, on top of €3,000 ($3,110) in tax-free bonus payments to counter inflationary pressures. The union has recommended the agreement to eventually cover some 3.9 million workers in Germany’s industrial sector to help compensate for soaring living costs.”

Japan core inflation rose to a 40Y high of 3.6% y/y in October | RTRS

Extracts - “The nationwide core consumer price index (CPI) was up 3.6% on a year earlier, exceeding the 3.5% rise expected by economists and the 3.0% gain seen in September.

The rise in the index, which excludes volatile fresh food prices but includes oil products, confirmed that inflation remained above the 2% goal of the Bank of Japan (BOJ) for a seventh consecutive month.

But economists do not expect the BOJ to join a global trend of raising interest rates, because it sees this year's acceleration in inflation as a cost-push episode that will fade as import costs stop pushing.”

UK October CPI hit 11.1% YoY, a new cycle high

Mercedes-Benz cut prices on two electric car models in China by as much as US33k

Extract of Autonews: “Mercedes-Benz cut prices on two electric car models in China by as much as $33,000, as heated competition in the world’s biggest EV market impacts sales. The automaker said in a statement on its website on Tuesday that it was reducing prices on certain models from its EQ range, effective Wednesday, and that it would provide subsidies to customers who recently bought the cars. The cuts seemed to be immediate, with the EQE priced at 478,000 yuan ($67,675) on Mercedes’ Chinese website Wednesday morning, compared to 528,000 yuan as recently as Tuesday. The EQS luxury edition model was listed at 956,000 yuan on Wednesday, down from 1.19 million yuan on Tuesday, equivalent to a reduction of around $33,000. Mercedes is making the cuts because sales have been disappointing in China, according to people familiar with the company’s plans, who asked not to be identified because the information is private. Some dealers have already been carrying out promotions to try and boost sales, with EQS deliveries at times dropping to as low as 100 a month, the people said. The EQS is the full-electric version of Mercedes’ flagship S-Class model, a vehicle that is meant to showcase the automaker’s most advanced technologies.”

*NEW ISSUES/TENDERS*

Risk-on tone in markets enabled some liability management (of near term maturities and new issuance this week for European Companies. It was not all plain sailing as Nova Ljubljanska was said to have postponed its EUR 10NC5 Tier 2 Bond.

Telefonica new EUR Corporate Hybrid issue and tender | Statement

New Telefonica EUR Corporate Hybrid priced at 7.125% with a 2028 call. This bond seemed to re-invigorate the Corporate Hybrid market, with market participants assessing relative value in the sector once again. I had referred to Telefonica in last week’s blog but didn’t expect a new issue/tender to come so soon.

Extract: Telefónica today successfully issued a sustainable hybrid bond, amounting to EUR 750 bn . The company has also announced a tender offer over three hybrid bonds which begins today and is expected to close on November 25th. With both transactions, Telefónica continues to proactively manage its hybrid capital base. The hybrid bond issuance has been very well received by institutional investors, with a book of over 175 orders and a broadly diversified investor base with over 90% international investor participation. With the proceeds obtained, Telefónica will finance or refinance projects with positive environmental and social impact in Spain, Germany and/or Brazil, which will contribute to SDG 9, SDG 8 and SDG 7.” SDG refers to Sustainable Development Goals, details of which can be found in the statement.

SocGen priced $1.5B PerpNC5.5 AT1 at 9.375%

This follows on from DB which raised AT1 paper at 10.0% in Euros and BNP which raised a $ AT1 at 9.25% last week.

HSBC Tender offer results - Around £1.4bn tendered by holders | Statement

The higher level of take-up is consistent with other bond tender offers over the past few months. Last week, HSBC offered some new high coupon bonds in EUR and GBP which some holders may recycled capital into.

Tender activity in and lack of new issuance driving spread tightening in GBP Credit

One firm highlighted the strength of the GBP Credit market, driven by a combination of a more political stability (compared to Truss/Kwarteng!), high level of bond tender activity (Abi Inbev, GSK, Tesco Property, GE and HSBC) and low new issue supply in Sterling.

SBB announces tender offers - EUR 631m accepted | Statement

Nordic Real Estate firm SBB accepted some EUR corporate hybrids as a part of its tender. This comment in the statement was also interesting: "The result of the tender offer shows that the bond prices at which investors are prepared to sell bonds are far above the prices shown on screen. SBB has succeeded in repurchasing bonds for approximately EUR 500m. The result from the tender offer means a positive effect on equity attributable to SBB's A and B shareholders of approximately SEK 1.4 billion or approximately SEK 1 per share," says Ilija Batljan, CEO and Founder the Company.

German Real Estate Landlord Vonovia tender for bonds and new issue

Issuance proceeds plus €500m from cash on hand to be used to tender for 2023 and 2024 bond maturities plus a potential repayment of other debt according to Vonovia. Vonovia raised two unsecured bonds in social and green format with aggregate proceeds of €1.5bn. Weighted average coupon of 4.875% in EUR and weighted avg. maturity of 6.3 years, books were said to be 6x covered.

Side note #1 - Consus Real Estate AG, a unit of troubled Real Estate firm Adler announced that it is in “Advanced negotiations on provision of secured debt financing.” This news, last week’s successful loan for SBB and Vonovia’s bond deal suggests that funding conditions are thawing slowly in the Real Estate sector, helped by risk-on credit markets..

Side note #2 - The STOXX Europe 600 Real Estate sector has outperformed the broader STOXX Europe 600 over 1 month (chart below)…but there is a lot of catching up on a YTD basis since it is down nearly -40% (as at 17 Nov) vs -12.5% for the broader index.

Travel and Leisure Converts issuance - Air France and Carnival

Air France and Carnival both hit the market with convertible bond issuance and predictably the shares of both sold off on the announcement.

Carnival priced up $1bn of convertible bonds at 5.75% for 2027 maturity The UoP is to refinance 2024 maturities according to the company. Air France raised 300 million euros with convertible bond issue - RTRS. "This transaction marks a further step in the group's initiatives to accelerate the repayment of French state aid, continue to strengthen equity capital and help optimise financial costs," the company said in a statement. The Convertible was priced with a 6.5% coupon in Euros.

EUR HY/EUR FINS - Round up of other notable issuance/corporate actions

The improved risk tone has allowed a number of European HY issuers to come out with bond exchange offers ahead of maturities last week:

IPF - Home credit and digital provider of consumer finance IPF announced a transaction to exchange holders of its current £ IPF 7.7% 2023 notes into a new £ 12% IPF 2027 notes.

Newday - Credit card provider New Day is offering 13.25% senior secured notes and proposing an exchange of its 7.375% notes due 2024.

Greek Bank Issuance - Senior Prefs

DCM desks tapped into investors demand for senior Greek Banks issuance this week:

National Bank of Greece raised €500m 5NC4 Sr Pref at 7.5%

Greek Bank Piraeus Bank raised €350m 4NC3 Sr Pref to Yield 8.5%

*FINANCIALS*

Allstate raises Auto insurance rates by 14% in October | Marketwatch

Extract: Allstate Corp disclosed Thursday that it has raised auto insurance rates by 14% across 15 locations in October, as it responds to "inflationary increases to loss costs." The insurer said the rate increases for Allstate-brand auto insurance since the beginning of the year have resulted in a premium impact of 12.1%.

Troubled Insurer Lincoln National issues new perp

In a sign that markets are definitely in risk on mode, Lincoln National issued $500m NC5 perps at Par to Yield 9.25%. The bond issue is rated IG 3 agencies at the moment. This is the Insurer whose stock dropped 33% in one day on 3 November 2022. According to one analyst the company took a $2.2bn charge related to lower lapse activity on older-age individual life insurance policyholders.

UK’s Nationwide reports results, possible buyback of CCDS being discussed..

Nationwide Building Society reported its interim 2022/2023 results which looked decent from a P&L, Balance Sheet and Capital perspective.

Their full statement and earnings call are worth listening to understand the health of related markets e.g. Housing and the state of the UK Consumer. Most importantly for bondholders there was some potential news about a buyback of its Nationwide 10.25% CCDS instrument issued in 2013. This is an extract from the comment made by Nationwide CFO on the earnings call:

“I have previously talked about our desire to manage our surplus CET-1 capital more flexibly through the ability to repurchase CCDS periodically at our discretion. I am pleased to confirm that we are actively exploring -- implementing a facility that would enable us to do so. And we have made an application to the PRA for general prior permission, which is one of the prerequisites. Subject to this permission and completion of internal governance, we are targeting having such a facility available to us from early 2023.”

This comment sent the Nationwide CCDS prices around 10pts higher on 18th November.

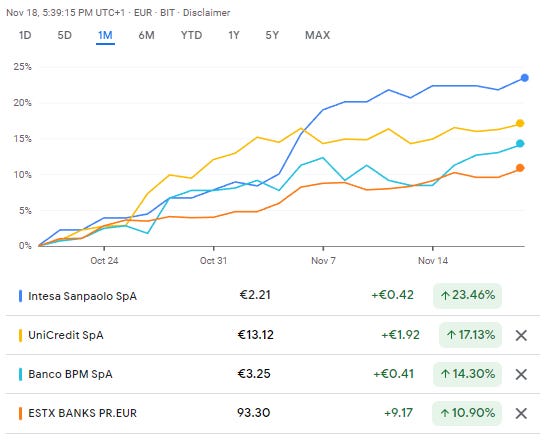

Notable stock moves in Financials

Italian Banks on a tear over 1 month, outperforming the Euro Stoxx Banks Index. Bank shares are performing well generally because of higher rates and modest loan loss provisions at this stage. The rally in periphery banks is usually indicative of a risk-on bias in markets.

UK Life Insurers are also enjoying a good month, likely boosted by the relaxation of some Solvency II measures and increased stability post the LDI fall-out.

Spain expects to agree with banks mortgage relief measures by end of week | RTRS

I wonder if the UK and other countries will follow suit with this sort of initiative…

Extract - “Spain's government expects to reach by the end of this week an agreement with banks on mortgage relief measures to help vulnerable households and middle-class clients cope with rising borrowing costs on such loans, the economy minister said. The government and lenders are readying a wider set of measures to help the most affected families deal with a rise on their variable mortgage loans triggered by aggressive interest rates from the European Central Bank.”

*HY*

Rakuten announces 12% yield on Junk Bond for its Mobile Unit

Extract from JT: “Rakuten Group is marketing a $500m (about ¥70.1bn) bond to bolster the Japanese internet firm’s struggling mobile unit, in a test of demand for a rare junk debt offering from the country and a borrower under financial strains. Amazon.com’s competitor in Japan is expected to price the two-year senior unsecured notes early next week, according to people with knowledge of the matter. The bond offering is gaining attention given the small, fledgling junk debt market in Japan, where weaker companies aren’t compelled to sell speculative-grade notes due to easy access to bank loans. The debt sale also comes after Rakuten reported widening losses for the third quarter and as it faces the risk of a credit rating downgrade…Rakuten's proposed bond sale would mark the latest addition to Japan’s tiny junk debt market. The outstanding amount of dollar bonds sold by the country’s speculative-grade issuers is $13.5bn, compared with about $2 tn globally, according to Bloomberg-compiled data. Rakuten and SoftBank Group are among the few Japanese junk issuers in the overseas market.

Rakuten’s Corporate Hybrids (e.g Rakuten 5.125%) did not seem to take it well as they dropped 10 points in a day (18th November).

UK Energy Explorer Waldorf Seeks Up to $2 Billion for M&A -BBG

“Waldorf Production, a prolific buyer of oil and gas exploration assets in the North Sea, is seeking to raise as much as $2 billion to help bankroll more deals, people with knowledge of the matter said. The British company is working with advisers to set up a vehicle that will raise capital from outside investors and make acquisitions, the people said, asking not to be identified because the information is private. It has has approached a number of hedge funds and specialist energy investors to gauge their interest in participating, the people said.”

The news article appeared to be published after the announcement of the Autumn Budget. Sidenote, the UK North Sea O&G companies shares did not take the news of higher taxes for longer well, bond prices were lower, but showed less muted moves.

Heimstaden Bostad & Allianz inject new equity into Swedish JV, using proceeds to repay debt

Allianz Real Estate and Heimstaden Bostad inject SEK 7,000m (EUR 650m) in new equity in their existing Swedish JV, using the proceeds to repay debt. Simultaneously, Allianz and Heimstaden Bostad form a new joint venture comprising Allianz’s German residential real estate portfolio. Source: Cision

US Homebuilding sector - JPM forms $1bn JV for Rental Homes in the US

Extract of BBG: “JPMorgan Chase & Co.’s asset-management arm entered into a deal to acquire more than $1 billion of single-family rentals, a sign that choppy markets haven’t scared investors away from suburban housing. Institutional investors advised by the bank formed a joint venture with Haven Realty Capital to buy and develop entire communities of new homes, according to a statement Tuesday. The partners are seeding the venture with three communities in the Atlanta area, and will eventually deploy $415 million in equity, enough to acquire more than 2,500 houses.”

*CHINA*

EM House Gramercy comments on impact of China measures last week

Extract: “We see the incremental zero COVID policy relief and the real estate measures as constructive. Further, the measures are in line with our expectation for a window for such actions after the conclusion of the Party Congress and a needed bridge to manage growth and liquidity conditions through the winter. While they are unlikely to have an immediate material effect on activity and the property market recovery, we think the policies should help limit default pressures in the coming months and represent a more material loosening of policy than witnessed thus far this year. Our base case remains for continued adjustment of COVID related measures to set the stage for a more meaningful evolution in 2023 upon improved seasonal and vaccination dynamics. At the same time, we see room for a broadening of the response to the property sector and a more material pick-up in sales as next year progresses.”

Sidenote: Iron ore price gained for third week mainly on the hope of China Property sector improving.

*CRYPTO*

Crypto bonds update

With last week’s news of several Crypto platforms being in trouble, I decided to check in on how bonds of Crypto related issuers are doing.

Coinbase (BB rated issuer) bonds are trading between 50 and 55 with yields of 13-15%. Its busted converts are trading at 55 which is well off the highs seen in 2021 of 125.0. Microstrategy’s 2028 bonds are posting a total return of minus 15% so far this month to date as at 18 November 2022 and trade around 72.0, therefore a higher cash price than those on Coinbase. This is likely a reflection of Coinbase running an exchange which may have more contagion impact from events seen at FTX and other exchanges whereas MSTR just owns BTC.

*EM*

Tullow Oil Balance Sheet / cashflow Q3 highlights from statement

Full year FCF guidance has been increased to c.$250m, subject to year-end working capital movements, assuming an average oil price of $95/bbl for November and December.

Balance sheet strengthening is on track to achieve cash gearing of less than 1.5x by year end.

*PRIVATE CREDIT*

Blackstone Private Credit Taps 7.05% Notes of 2025 to raise $200m @ +310bps

Intermediate capital Group CEO says firm has been preparing for a downturn

UK listed Asset Manager provided a Q3 update. Extracts below:

"Looking ahead, rising costs of capital, higher inflation and lower growth are putting pressure on consumers and businesses alike. We have been preparing for a downturn for some time," says CEO Benoît Durteste

Providing solutions within market-wide backdrop of tighter financial conditions and lower transaction velocity helped Group execute bespoke transactions for portfolio companies

Group saw "strong pipeline within direct lending, providing senior debt financing to upper mid-market companies where the high-yield bond and leveraged-loan markets have been largely shut"

*ESG*

Global ESG-Linked Bond Market Faces Its First Set of Penalties - BBG

Extract: “The revival of fossil fuels in European energy policy risks triggering the first wave of financial penalties in the global market for ESG bonds. A test case is about to unfold in Greece, where energy supplier Public Power Corp. may find it “virtually impossible” to meet the end-of-year emissions target on some of its debt, according to an analysis conducted by the Anthropocene Fixed Income Institute…

The debt in question is a sustainability-linked bond. SLBs typically see issuers pay a penalty if they miss pre-determined environmental, social or governance goals. But with Europe’s decision to ramp up coal production in response to the current energy crisis, near-term climate commitments are being derailed. And that’s left many utilities with little choice but to adapt.

The current situation “may result in the step-up clause on our SLB bonds to be put in place,” the spokesperson said. “However, given our stated commitments, we do not see issues with our credit institutions, debt holders or credit agencies from the enforcement of the step-up.”

EIB is contributing to modernisation costs with an unsecured loan of €600m to Vonovia

Extract: The EIB is supporting Vonovia SE's multi-year energy-efficient building modernisation programme with an unsecured loan of € 600m. The loan has a term of 8 years with (unspecified) attractive interest rates

*LINKS*

Pimco 2023 Asset Allocation Outlook - Link

“Risk‑Off, Yield‑On With interest rates higher amid a challenging macro environment, we see a compelling case for bond allocations and are cautious about higher-risk investments.”

GS 2023 Credit Outlook via James Wong of Linkedin

“Goldman’s 2023 Credit Outlook: There will be Yield 🤩 Solid total returns, low but positive excess returns, and still elevated dispersion Our core message throughout the year has been that, barring a material reset in valuations or convincing signs of improvement in the interaction between the inflation backdrop and the policy path, spreads would continue to build more premium and drift wider. The timing and the magnitude of this improvement were, and still are, uncertain, but our best guess is that risk sentiment will eventually recover in early 2023 as the soft-landing path in the US becomes more visible. We continue to think that the asymmetry remains negative in the medium term, as the prospect of an extended hiking cycle will likely act as a binding constraint on any material easing in financial conditions.”

Continues on the link above..

MS’ Credit Forecast for Q4 2023

Awesome work!