Global Credit Wrap 11 November 2022

SBF/FTX free zone here...

*TLDR*

Slightly different and shortened format this week. Fixed income markets rallied strongly boosted by positivity around a lower than expected CPI print, a reasonably market-friendly outcome at the US Mid Terms, and China re-opening measures. The biggest gainers were Duration and EM (including China). To add to the mix, Russia retreated from a key City in Ukraine (Kherson). New issue markets across Corporates and Financials printed some high coupon issuance which rallied strongly in the risk-on move last week.

The rest of the year is likely to characterized by a mix of what the Fed does next, how real the China re-opening is and how much attention is lost from the Fixed Income Trading community to the Football (Soccer) World cup beginning in a week’s time as well as Thanksgiving, Hanukah and Christmas Holidays…

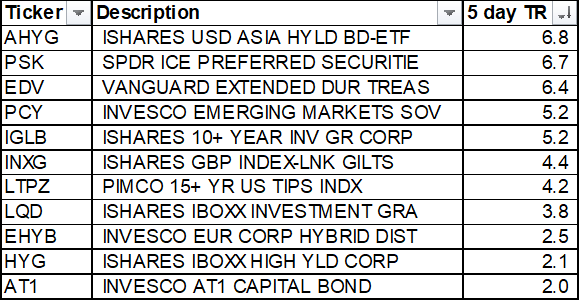

*MOVES OVER 5 DAYS*

Huge macro moves following the better than expected CPI last week

-Short dated UST rallied strongly; 2 year (-32bps), 3 year (-40bps tighter), 5 year (-39bps tighter).

-Japanese Yen went down to below 140 after touching 150 in the middle of October

CDS - Xover now at 482bps which represents a material tightening vs the high of around 670bps seen in September as the market was extrapolating a move higher towards the worst levels seen during the global pandemic. Sub Fin CDS below 200, Itraxx Main below 100bps. In the US, CDX IG at 83bps and strong rallies in CDX HY (-28bps) and CDX EM (-24bp)s over the week.

Cash Credit spreads - US HY spreads at +468bps is still well below the long term average of 502bps…debate rumbles on about whether we should be looking at all in yields or spreads…European HY spreads rallied 67bps to 535bps. EM HY has rallied 32bps to 779bps.

Bond ETFs

China, duration, rreference shares (a long duration asset) and EM seemed to be the main winners of the rally in Fixed Income last week

Popular high beta ETFs such as HYG and AT1 underperformed the sectors mentioned earlier.

*NEW ISSUES/TENDERS*

Sub Financials - AT1s

Deutsche Bank EUR 1.25b PNC (2028) AT1 @ 10% coupon

BNP Paribas $1bn PerpNC5 AT1 @ 9.25% coupon

DB AT1 might be the first AT1 to print in Euro (in recent history) with a double digit coupon. The BNP AT1 was its fourth this year. Both deals closed at a decent premium to par. Also notable that recent issuer Permanent TSB’s super high coupon 13.25% deal closed the week up nearly 7pts, riding the high beta rally post CPI.

Bank Tier 2s

The Sterling credit market is functioning a lot better vs Sept/October. Part of this is down to the large coupons being offered by issuers currently.

For example, Barclays issued a new £ BACR 8.407% 2032 T2 and HSBC issued in € and £:

New € HSBC 6.364% 11/16/32

New £ HSBC 8.201% 11/16/34

All the deals traded up ~2 points following issuance. There was a tender offer announced by HSBC for various older GBP and USD issuance including some retail denominated paper in GBP.

Credit Suisse

CS issued two very high coupon senior bonds signaling a return to market after a period of absence. Book sizes were large, with BBG reporting that the Dollar bond attracted demand 4x the issue size.

$ CS 9.016 11/15/33

€ CS 7.75 29

Both deals closed at a healthy premium in the secondary market. BBG covered the story here.

IG - Huge week of issuance in light of market conditions

US IG had a big week with over $45bn pricing, this included $7bn of debt for Oracle (vs $44bn of demand) and GE Healthcare which priced up over $8bn of bonds. Oracle borrowed the money to pay for its acquisition of Cerner and GE healthcare was using it to fund a sizeable debt buyback at parent company GE.

Meanwhile in Europe, €58bn printed during the week including a deal for Orange (BBB+) which priced €750m at 9 year Midswaps +63bps ~ or a yield of 3.665%.

US HY

BBG reported that US HY issuance this week was the busiest since early June. There was a diverse set of issuers this week which included DISH (TMT), Spirit Airlines (Secured Airline EETC paper), Ball Corp (Aluminum packaging rated BB+). As per the tweet below, issuers were not messing around, and offered big yields to print size, e.g. Dish Secured bond @ 12.0%.

Also in a sign of the times, Ball Corp, which issued a super tight HY bond last year (Ball 3.125% 2031) had to pay more than double that this year to price up 10 year bonds (6.875%). BBG reported that $6bn was priced in US HY in the week, a substantial figure compared to prior weeks.

There are still prospective large deals said to be being marketed which include the $1bn secured note for Apollo’s Tenneco and a term loan for OpenText to fund the acquisition of listed UK Software firm Micro Focus International.

EM Issuance - Poland and Turkey issued in USD

There was a rare USD dual tranche issuance from Poland and Turkey issued $1.5bn of 5 year bonds at 99.454 to Yield 10%. For Poland it was its first return to the USD bond market for 6 years according to BBG. There is some life in EM loan markets too with tower firm IHS Holding entering into a new $600m the year bullet term loan in October, the terms of the loan stipulate an interest rate of 3.75% + 3 month SOFR and CAS. Could we see more issuers follow the bank loan path as bond markets remain tricky for higher beta credit sectors?

*IG*

Ryanair posted its largest ever profit for its key summer season…(RTRS)

…and said it expected very strong passenger and fare growth for years to come as customers switch from higher-cost rivals.

Travellers are likely to prefer the “value trade” offered by discount airlines if a recession were to hit in the UK/Europe.

Telefonica responds to questions on its Corporate Hybrids on its earnings call..

Laura Abasolo, CFCO of Telefonica was asked about the upcoming call (June 2023) on one of its Corporate Hybrids. Reading between the lines on her response, it seems the issuer remains committed to having hybrids in its capital structure and is very aware of the permitted flexibility from ratings agency S&P to redeem part of its debt. These were extracts from the earnings call:

“Hybrid is definitely a part of our capital structure and it has served its purpose and it has as you know a 50% debt component and also a 50% equity component

The cost of the [hybrid] layer is 3.56%, and it has been reduced very much in the last two years

Our intention is to refinance and exercise the calls [ph] in a manner that is consistent with best market prices [I assume they meant to say “practices” instead of “prices.”]

We are not in a hurry. We have time to decide as we still have time till June '23 to exercise our next hybrid call, part of that was already refinanced in the past. And we can also eventually make use of the permitted flexibility from S&P…”

Source: BBG

The topic of Hybrid refinancing seems to be top of mind for sell side, buyside and issuers alike right now.

European REIT Roundup

The UK/European REIT sector has become one of the closest watched sectors in the Credit markets as issuers contend with higher rates and the possibility of recession.

Many issuers are attempting to demonstrate their ability to service debts whether it be via property disposals and / or borrowing in other forms to pay down bond debt.

SBB Corporate Hybrids move higher after €750m loan to buyback bonds

Extract from BBG: “We understand that SBB will fund the transaction with a €750 m bridge facility (with a term of 12 plus six months), which will be refinanced via proceeds from disposals in the coming quarters,” according to a report by rating company Standard & Poor’s.

SBB published a tender offer for €650 million of hybrid notes and senior bonds. Its Hybrids appear to be trading at deeply discounted levels to par at around 40.0.

Corporate Hybrid issuer CPI Property Group gave an update on its disposals…financing and distributions this week, some key extracts:

“Executing disposals to reduce leverage is a top priority for CPIPG in the coming 12 to 24 months.”

“Since the Group’s announcement at the end of August, CPIPG has made significant progress on the disposal pipeline, closing sales with gross proceeds exceeding €300 million”

“CPIPG refinanced and upsized a portion of our €750 million bank loan in Berlin, which is due in 2024. The new loan totalling €515 million, with an additional €200 million of proceeds received, matures in 2029. The loan was concluded with the existing lender (BerlinHyp) at similar terms to the original loan in 2017.”

*CHINA*

China Plans Sweeping Rescue Policies to Avert Property Crisis - BBG

It looks as if China is finally getting organised about opening up its country and now sorting out issues with its property market, extracts from article:

“The People’s Bank of China and the China Banking and Insurance Regulatory Commission on Friday jointly issued a notice to financial institutions laying out plans to ensure the “stable and healthy development” of the property sector, said the people, asking not to be identified as the matter is private. Unlike previous piecemeal steps, the latest notice includes 16 measures that range from addressing the liquidity crisis faced by developers to loosening down-payment requirements for homebuyers, the people said. As part of the rescue plan, developers’ outstanding bank loans and trust borrowings due within the next six months can be extended for a year, while repayment on their bonds can also be extended or swapped through negotiations, the people added.

One of the biggest policy changes in the latest notice is to allow a “temporary” easing of restrictions on bank lending to developers.

China began imposing caps on bank’s property lending in 2021, as authorities sought to tighten the reins on a bubble-prone industry and curb leverage at some of the nation’s largest developers. Banks not meeting the current restrictions will be given extra time to meet the requirement, said the people. “

*EM*

Romanian Central bank hikes rates amid high inflation, again - EurActiv

Extract: “Romania’s central bank raised its main interest rate by half a percentage point, to 6.75% as it continues to battle high inflation. The central bank expects the prices will continue to grow rapidly by the end of the year, with the inflation rate considerably above its target interval. In September, the annual inflation rate was 15.9%, up from 15.3% in August.”

Georgia Capital provided a useful update on the state of the Georgian economy

Extracts of the presentation:

Georgian Lari (currency) back to pre-pandemic levels

Tourism revenues rebounding to 98% of 2019 level in 9M22 (including 121% in July, 127% in August and 118% in September)

Tight monetary policy (cumulative hike of 300 basis points since March 2021 to 11% as of November 2022), supporting stronger GEL (currency)..

83.5k migrants have opened Georgian Bank accounts since the start of the Ukraine / Russia war (mainly Russians)

El Salvador says China offered to buy all its foreign debt…BBG

"China has offered to buy all our debt, but we need to tread carefully," Vice President Felix Ulloa said. "We are not going to sell to the first bidder, we need to see the conditions."

ELSALV 7.75% January 23 bonds trade at around 90 after being as low as 65 cents in the Dollar in July this year. El Salvador has bought back around $130m of these bonds in September, which likely helped lift the price of the bonds.

Pakistan secured $13bn in additional financial support from China & Saudi: Pakistan Finmin Dar - Khaama.com

Extracts of article:

According to Dar, Pakistan would be getting about $9bn from China and $4bn from Saudi on top of assurances for about $20bn in investments. During Prime Minister Shehbaz Sharif’s recent visit to Beijing, the Chinese leadership promised to roll over $4bn in sovereign loans, refinance $3.3bn commercial bank loans and increase currency swap by about $1.45bn – from 30bn yuan to 40bn yuan, as The Economic Times reported. “They promised the security of financial support,” Dar, who recently took over as the new finance minister of Pakistan from his predecessor Miftah Ismail, said and quoted Chinese President Xi Jinping as telling Sharif, “don’t worry, we will not let you down”.

After the experience that other EM nations have had with China, its probably worth waiting till the “money is in the bank” before quoting Chinese Officials!

Kosmos Energy Q3s - Stock up more than 50% vs September low..!

Debt highlights from statement: Kosmos exited the third quarter of 2022 with $2.1bn of net debt and available liquidity of approximately $1.0bn. The Company generated $32m of free cash flow in the third quarter, and around $320m through the first nine months of the year. With EBITDAX for the quarter almost four times higher than the same quarter last year and continued net debt reduction through 2022, the Company achieved its target net leverage ratio of 1.5x ahead of schedule with further progress expected in the next quarter at current prices.

US HY issuer Occidental also reported that it repaid $1.3 bn of debt during Q3, with YTD repayments of $9.6 bn through November 7, 2022, representing 34% reduction of total outstanding principal. A number of E&P issuers are following the same trend of paying down debt and bringing down leverage…