Weekly (ish) Global Credit Wrap to 3 May 2022

Narrative on bonds becoming more balanced..

*MACRO*

Rates

The meme below sums up just one of the many challenges that money managers face with regards to buying the current dip in bonds…

Charlie Bilello continues doing his great work in logging the longest drawdown in US bond market history:

I have started to notice more bullish commentary in spots from strategists and market commentators (here* and here). Hats off to Morgan Stanley for coming up with the title: “Putting the ‘Income’ Back in ‘Fixed Income’” on one of its research notes. The 10 year UST going through 3% yield got the Fintwit community excited (me included) today. However, as I tweeted today, shorter dated Treasuries are at or near 3% anyway, an unthinkable situation just a year ago…

* Ben Carlson of Ritholz Wealth is one of my favourite bloggers / podcasters. His stuff is really worth reading.

Credit spreads

Widening trend continues with a number of key indicators above 400bps again, i.e Xover at +428bps and CDX NA HY at +455bps. Sub Fin CDS indices flirting with +200bps. In cash credit spreads, European HY and Global Bank CoCos spreads are above 400bps but US HY and EM are at +388bps and +339bps respectively. Data to 3 May 2022.

Bond ETFs

No respite here either, weakness over past 5 days most evident in:

PGX -3.5% (DOWN 16.8% YTD) - Preferred securities

TLT -3.1% (down 20.5% YTD)

EMB -3.0% (down 16.2% YTD)

EMLC -2.5% (down 10.9% YTD)

LQD -2.4% (down 15.0% YTD)

HY

Euro HY New Issuance - Miller Homes brings it home…

BBG lead on a story that Miller Homes got its debt financing done last week, pricing wider than IPT.

Extract: ~$1bn of bonds split across a fixed rate Sterling and Floating Euro Denominated note. The deal terms were sweetened along with the wider pricing, which are good outcomes for investors. It is common for investors to gain the upper hand during periods of major market stress, as we saw in the aftermath of the pandemic, e.g. when these bonds were issued:

AMC 1st lien secured bonds at 10.5%

Carnival 1st lien secured at 11.5%

Delta Airlines 7% 2025s secured bonds on landing slots

Note that both the AMC and Carnival issues have already been redeemed early and the Delta Airlines 7% 2025 bond is being partially bought back by the issuer.

While it is too early to say if it’s “all systems go” for the European HY new issue market, the transaction demonstrates that deals can be done at a price and that we maybe embarking on an attractive vintage of deals for credit.

$ HY - Carvana - Apollo to the rescue?

Looking across the pond, the WSJ reported that Used Car specialist Carvana got its debt financing done, mostly due to Apollo stumping up a significant sum of money ($1.6bn) to get the deal over the line. Essentially the lead manager had initially proposed a preference share issue but then this plan was scrapped since there was not enough demand and instead Apollo supposedly became the anchor order for a new $ HY bond, but at eye-watering pricing of 10.5%. The WSJ article goes into much more detail on this transaction and is really worth a read. The trend of large investors providing capital to distressed companies on their terms is a well trodden path as demonstrated by Warren Buffet and his Goldman Sachs preference shares during the GFC.

On a behavioural level, it is interesting contrasting the recent behaviour of firms with locked up capital (more aggressive) vs those who have open-ended structures (outflow driven nervousness). The large Private Credit/Closed Ended Fund Investors appear to be finally using up some of that dry powder that they keep referring to on conference calls/presentations.

I noticed that the smart guys over at Petition did a nice looking detailed write up on Carvana (which I confess to not reading yet fully!).

Side-comment on European Loan Market - Still functioning..

At least two loans have been priced recently in the European HY market, with both Cupa (construction) and Clinigen (Healthcare) raising leveraged loans with single B ratings. Pricing was around 4.5% to 4.75% for TLBs which priced at a discount to par for 7 year tenors. Clinigen maybe known to UK Mid Cap Equity investors, but I had missed that they got taken over by a PE firm earlier this year.

*CHINA*

I've moved up the China section this week as there was some important news regarding a boost to infrastructure spending by the Chinese Government. Extract:

“Chinese President Xi Jinping on Tuesday called for all-out efforts to strengthen infrastructure construction in the country's building of a modern infrastructure system.”

CNN - “Citi analysts, meanwhile, believe China's infrastructure investment is likely to surge by 8% in 2022, sharply higher than the 0.4% increase seen in 2021.”

"The infrastructure push is real," they wrote Wednesday in a note. "The turning point for real policy actions may have arrived, and stimulus will likely come through more obviously from late Q2."

Should this theory play out, then we could see commodities and cyclical plays continue to perform well, tempered by an expectation from some parts of a market of a slowdown in the US Economy.

But there has been plenty of other stuff going on in China too besides this, see the excellent weekly tweet from BBG’s Sofia Horta e Costa for the TL:DR:

*COMMODITIES/INFLATION*

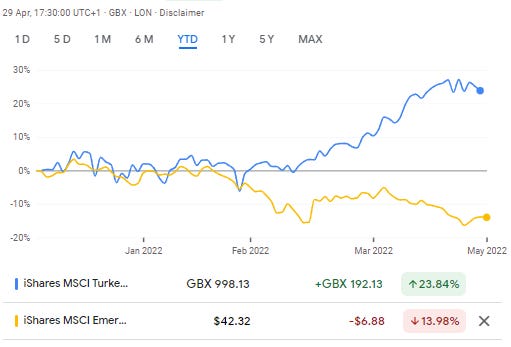

Surge in Dollar and oil price not treating all EMs the same..

One of the speakers at an oil conference I attended this week highlighted that countries such as Turkey and India have been buying cheap Russian oil at a large discount to the Brent Crude benchmark (around $30-$40 cheaper). So effectively, these countries that continue to buy Russian oil have not endured the same problem that has sent some countries into default (e.g. Sri Lanka). This could be one of the reasons behind the stunning performance of Turkish Assets vs EM as a whole. Chart of ITKY vs EEM Equity ETFs:

Capital Gearing Trust - on Inflation

Peter Spiller who has been managing the Capital Gearing Trust( Ticker: “CGT”) for 40 years talks inflation in CGT’s Quarterly Q1 report. Its worth listening to what he has to say due to his tenor on the Fund, which often carries a large exposure to inflation linked assets (35% in Inflation linked Govvies as at end of Q1 2022).

*IG*

Europe Company Bonds Suffer Worst Peak-to-Trough Drop in History - BBG

High-grade bonds have fallen a record 8.6% from latest peak

Drop worse than selloffs during Covid and financial crisis

*FINANCIALS*

Some $ AT1s are either trading below 80 cash or nearing it

A number of AT1s have seen their prices fall into or near the high 70s. For example: ING 3.875%, ING 4.25% and Nordea 3.75%. The common factor for all these bonds is a relatively low reset and longer duration vs previous vintages of AT1 paper. During periods of market stress, dealers maybe marking prices to a yield to perpetuity instead of yield to call, especially for this type of paper.

*EM*

Ukraine - Kernel and Ukraine Rail

Kernel, the world’s largest producer and exporter of Sunflower oil and a leading producer of Agricultural products from the Black Sea region announced its intention to sell material agricultural facilities. As per a filing submitted to the Warsaw exchange, Kernel decided to do this to improve its liquidity position. More here: Odessa Journal. Kernel bonds have rallied from lows of around 30 cents in the Dollar to the mid 50s.

Ukraine Rail - Interesting to see a number of foreign “VIPs” use Ukraine Rail services during their visits to Ukraine. Angelina Jolie and Nancy Pelosi follow a number of recent high profile dignitaries recently coming to Ukraine and meeting with senior Ukraine leaders.

I have not been following the Ukraine developments as closely, but was pretty surprised to see people listed above visiting, does that mean the security situation is improving?

Vedanta Debt Tender and other Miners paying down debt

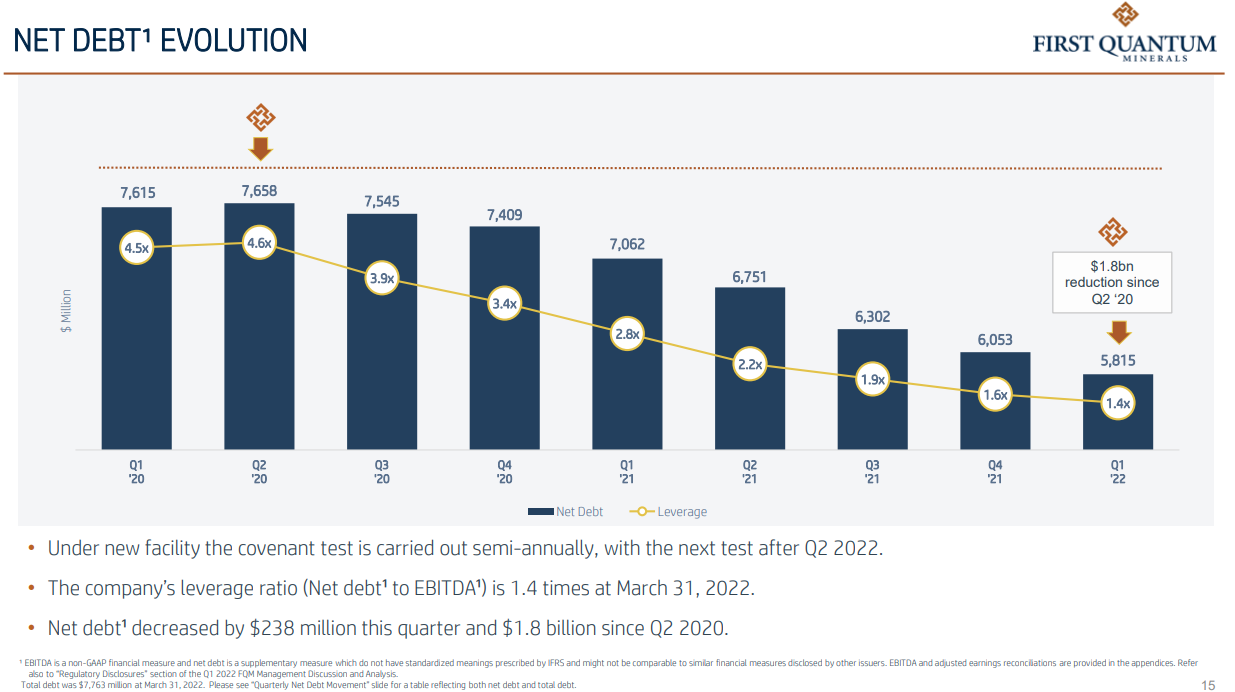

Vedanta, the well known survivor of the EM HY Metals/Mining world announced a tender for its July 2022 bonds which lifted the whole VEDLN curve. The notes are set to be bought back at par if the bonds are tendered by the early tender deadline. Ratings Agency Moody’s seem to like the action from Vedanta too. On a related note, B rated Copper Miner First Quantum highlighted how it has used supernormal profits from high copper prices to pay down its debt.

Source: First Quantum IR Page

Garanti Sub Debt - Non call

Turkish Bank Garanti decided not to call its 2027 subs (with a 2022 call) citing a number of reasons including global risks and uncertainties and an economic call policy. This reminds me of the time that Santander, Stanchart and DB did not call bonds at the first call, which sent the whole callable sector lower. In Garanti’s case, the bonds dropped ~6 points to around 95 but have recovered a point or so of losses. I have not looked at the rest of the Turkish subs sector, but there is likely to be some re-evaluation of expectations with regards to bond calls there. Gramercy went into more detail about this issue in their weekly.

GOL Airlines Posted Its Best Operational Results Since The Pandemic - Simplyflying

Extract: “Sales levels in January and February increased by ten and 30%, respectively, compared to the same period in 2019, while in March, they expanded by 60% due to the increase in sales to the corporate segment.”

Bahamas - Economist Omits Imf Bail-Out For Bahamas Forecast After 2 Years - Tribune

A prominent Caribbean economist yesterday omitted predictions that The Bahamas will require an International Monetary Fund (IMF) restructuring programme for the first time since the COVID-19 pandemic began.

Nigeria’s Access Bank Sells $50m 5-Year Green Bond for Sustainable Projects - BusinessPost

Bonds printed with a 5.5% coupon for 2027 senior unsecured paper.

Angola earns 10 bln USD in crude oil export in Q1 2022 - Xinhua

Extract: “Angola exported more than 98.3 million barrels of crude oil in the first quarter of 2022, bringing in a gross revenue of over 10 billion U.S. dollars, the Angolan Ministry of Mineral Resources, Petroleum and Gas announced Tuesday. According to official data, the average price of crude oil stood at 103 dollars, an increase of 67 percent over the same period last year, while the export volume fell 0.21 percent year-on-year. The ministry said China was the main destination of Angola's oil exports, followed by India and France.”

Mark Mobius likes the look of Sri Lanka Stocks and Bonds - EconomyNext

Mobius appears to be putting his money where his mouth is by buying an apartment in Sri Lanka too!

*LINKS*

Nowhere to hide in bond market - Total returns in April and YTD

- Sourced from the excellent Topdown Charts

Not many places to hide generally…

German CPI

Last week, Euro headed closer to parity with the Dollar

Raoul Pal & Why The Bond Market is the Ultimate Truth Teller - Real Vision

Sri Lanka - Informative update on the Sri Lankan Economy from Asia Securities