Weekly Global Credit Wrap w/e 9 April 2021

Shipping, EM, Legacy bank capital, Airlines, Airports and Travel Agents...

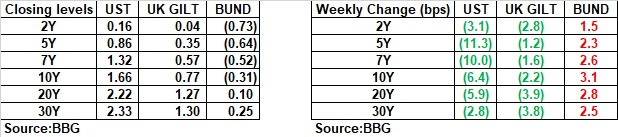

*OVERVIEW & MACRO*

Modest US rates rally results in some buying in credit

The rally in rates last week saw buyers step in into high yield and BBB bonds of intermediate maturities. My feeling is that the slowing of the steepening of the US yield curve has encouraged buyers to return to parts of the credit market. Also, the cliche of cash on the sidelines seem to be what most bank desks are reporting, which mirrors flow activity in Investment Grade and HY markets.

US HY continues to do well with the average junk bond yield dropping below 4% for the first time in two months and is just 11bps away from breaching the all-time low of $3.89%. Furthermore, CCC yields hit an all-time low and spreads are at a 7-year low of +512bps. Finally, junk bond spreads dipped below 300bps for the first time since July 2007 to +295b. All these stats are courtesy of @gowrinyc of Bloomberg.

Credit volatility in HY has also tailed off meaningfully, this topic is discussed in a useful podcast from Arbor Data.

Newsflow has definitely been lighter than normal, but this will pick up in the next week when Q1 reporting begins, led by the US Banks as usual.

Rising freight rates seeing dramatic increases in profitability at Cosco Shipping

At the start of the week, China’s Cosco Shipping reported figures. It expects profit to surge as freight rates have increased. The shipping sector is benefitting from earlier capacity cuts combined with stronger-than-expected demand according to the WSJ.

The market really liked what Cosco had to say as it sent its shares in China “limit up” of 10% on the day and 29% in its HK listed shares. Cosco Shipping expects this year’s first-quarter net profit to total 15.41 bn yuan, or the equivalent of $2.3 bn which compares to $44m in Q120.

Shipping rates rose nearly 54% compared with Q4 according to Cosco Shipping, citing the widely tracked China Containerized Freight Index. The company controls the world’s third-largest container carrier by capacity. More details in WSJ.

*EM*

Potential $650bn increase to IMF’s SDR…weaker EM nations to benefit

Reuters extract: “The world’s top finance ministers are set to back a new $650 billion allocation of the International Monetary Fund’s own currency, Special Drawing Rights, to help low-income countries hit by the coronavirus pandemic.”

Why is it important? Well it should help bolster the FX reserves of some of the EM nations with weaker financial positions. According to Citi’s analysts (cited in the Reuters article) they estimate that “the increase [in SDR] will more than double Zambia’s reserves and increase Zimbabwe’s more than six-fold. It is also good for countries like Argentina, Turkey, Sri Lanka South Africa, Pakistan and Nigeria, which will also see a 10% to 20% boost to their FX reserves.”

Other good resources on SDRs include:

IMF Explainer on SDRs or if you want a non-IMF source, check out Al Jazeera’s page on SDRs.

Philippines Plans U.S. Dollar Bonds ‘Before Rates Skyrocket’: Finance Chief

Extract: “(Bloomberg) -- Philippines Finance Secretary Carlos Dominguez said the government plans to sell dollar bonds before interest rates rise, and will look for new revenue sources and ways to wind down debt next year. “We will tap the U.S. bond market before rates skyrocket,” Dominguez said in an interview with Bloomberg Television’s Kathleen Hays on Tuesday…”

Why does this matter? Because many EM Sovereign Finance Chiefs probably share Mr Dominguez’ sentiment but are not brave enough to come out and actually say it! The Philippines Sovereign has timed some issuance brilliantly in the past and achieved very low coupons, e.g:

Philippines 1.648% 2031 (USD)

Philippines 0% 2023 (EUR)

India takes step down QE road with $14 billion bond-buy plan

Extract of ET Article: “India’s central bank took a step toward formalizing quantitative easing, pledging to buy up to 1 trillion rupees ($14 billion) of bonds this quarter to keep borrowing costs low and support the economy’s recovery. The debt purchases under the program in the secondary market will start from April 15, Reserve Bank of India Governor Shaktikanta Das said Wednesday, after policy makers held the benchmark repurchase rate at a record low 4%…

The RBI joins Indonesia, Poland, and Hungary among other emerging-market central banks that have experimented with some form of quantitative easing amid the pandemic. The International Monetary Fund in October estimated that 20 emerging markets had embarked on asset-purchase programs for the first time, judging them “generally proven effective,” including by providing some stability to local financial markets.”

My main take-away here is that different EM Central Banks seem to be adopting diverging policies. A few weeks back Brazil, Georgia, Russia and Turkey Central Banks tightened their policy rates, in contrast to the RBI’s step into what looks like QE.

Volatility in bonds of Chinese Asset Manager - Huarong

This week saw volatility in the bonds of China Huarong, which according to its Wikipedia page is a “majority state-owned financial asset management company in China, with a focus on distressed debt management. It was one of the four asset management companies that the Government of China established in 1999 in response to the 1997 Asian financial crisis.”

The problems began on April 1 when trading in China Huarong shares and structured products was halted in Hong Kong, when the company said its 2020 financial results were delayed because its auditor needed more time to finalize a transaction.

Taking a cursory look at its bonds, it seems to be a popular issuer with a number of USD bonds held by many institutional EM investors. It is an investment grade issuer as rated by two of the well known ratings agencies. Its perpetual bonds due 2022 appear to have traded down more than 10 points, which is at odds with an investment grade rating. However, being a China based issuer, with what looks like a colourful past (former chairman, Lai Xiaomin, was sentenced to death, according to BBG), there seems to be plenty of newsflow to keep holders and traders of this name on their toes. Definitely feels like a deep dive research project for a keen analyst out there…

ICYMI: Morocco got downgraded to Junk by S&P last week

Judging by the spread moves, most people didn’t seem to care much about the downgrade. This could be because the sovereign already has a HY rating from the other rating agencies. Click here for more detailed commentary.

*FINANCIALS*

More legacy bank debt instruments being redeemed

Further excitement this week in the legacy bank capital space with Natwest redeeming its series C prefs at par. GlobalCapital (paywall) summed up the situation well:

“Natwest Group plans to redeem a 36 year old perpetual bond as it continues to clean up its capital stack ahead of the CRR transitional deadline later this year. The British bank announced on Wednesday that it would repurchase series ‘C’ perpetual primary capital floating rate note, of which $285.3m remains outstanding.

This lifted prices in the rest of the legacy bank capital sector and holders of similar securities are likely to be sitting pretty waiting to be redeemed at some point…

*HY & Convertibles*

Ratings agencies upgrade a number of Miners as they play catch up with fundamentals…

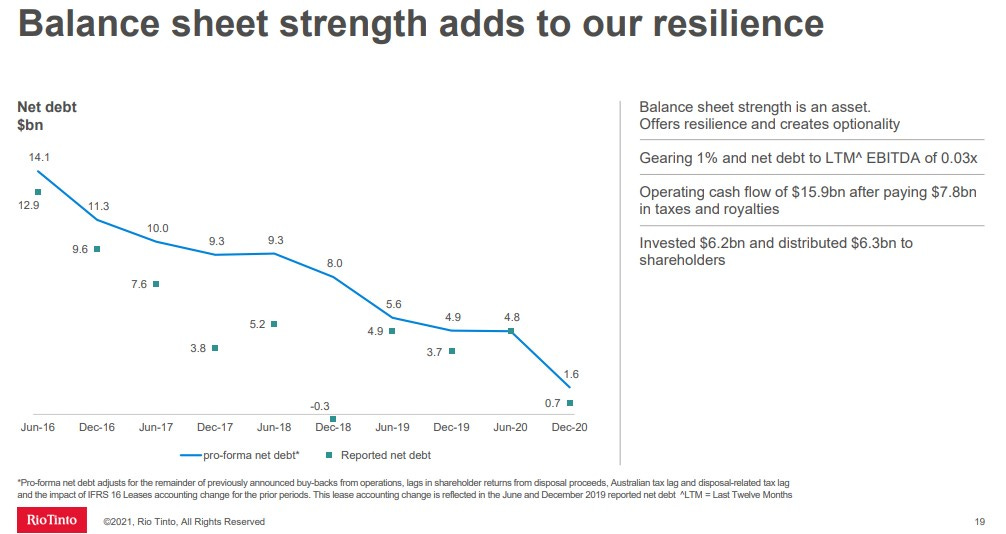

The commodity crash in late 2014/15 forced many metals & mining firms to prioritize the process of de-levering. The diversified miners demonstrated this the best with significant de-levering since that period (e.g. Rio Tinto), and also innovating by issuing corporate hybrids to reduce pressure on leverage ratios (e.g. BHP Billiton).

Source: Rio Tinto, FY Results

The ratings agencies moved to upgrade the larger diversified miners faster than the single resource miners. This is likely due to the diversified aspect of these companies which gives the agencies further comfort from a risk perspective.

However, this month, the ratings agencies have moved to upgrade some of the single resource mining companies (not meant to be exhaustive list):

Fitch Upgrades First Quantum to 'B'; Outlook Stable

First Quantum raised to B From CCC+ at S&P; Outlook Stable

Freeport McMoran Upgraded to BB+ by S&P, Outlook Stable (a possibility of investment grade status in future)

U.S. Steel Upgraded to B3 by Moody's, Outlook Positive

Tui Travel issued a EUR convertible bond with a 5% coupon

According to a release by the company, Tui successfully issued a 5% CB maturing in 2028 with proceeds of €400m.

The issue was upsized from 350m to 400m and was 2x over subscribed. The company said it plans to start the refinancing of the loans form the COVID19 stabilisation packages and it remarked that as at 22nd March, Tui’s liquidity amounted to €1.6bn, enough till the Summer of 2021.

Tui’s company profile: “TUI Group is the world’s leading integrated tourism group operating in more than 100 destinations worldwide. The company is headquartered in Germany. The TUI Group’s share is listed in the FTSE 250 index,

The Tui Convertible continues the issuance trend in Convertible bonds seen lately, although most of the issuance I have noted has been in the US. Convertibles seem to be popular with “re-opening” type issuers with Dufry (the Duty free operator) also recently issuing a convertible in CHF.

Air France gets European Union approval for €4bn in aid

Extract of France24 : “The EU approved a plan Tuesday by the French government to inject up to four billion euros into Air France, hit by a collapse in passenger traffic during the pandemic. The agreement, worth $4.7 billion, follows weeks of negotiations with the EU commission, which must ensure that state aid does not give companies an unfair advantage. In return for the green light, the commission, which is the EU's anti-trust regulator, said Air France would relinquish about 18 slots per day at Orly, Paris' second-largest airport after Charles de Gaulle. "This gives competing carriers the chance to expand their activities at this airport, ensuring fair prices and increased choice for European consumers," EU competition commissioner Margrethe Vestager said. French Finance Minister Bruno Le Maire said the EU had also allowed the French state to raise its stake in the national carrier to 30 percent, up from the current 14.9 percent.”

Ryanair founder and chief Michael O’Leary was unhappy with state aid being given to Air France:

“DUBLIN (Reuters) - A recapitalisation of Air France-KLM that will see France more than double its stake to nearly 30% will damage competition for decades to come, Europe's largest low-cost carrier Ryanair said on Tuesday.

"This latest tranche of state aid to Air France combined with these ineffective remedies will damage competition in the air transport market for decades to come," the airline said in an emailed statement.

"The 18 slots that Air France is being required to make available is nowhere near enough to allow others to offer a competitive challenge to Air France's dominance at Paris Charles de Gaulle and Paris Orly airports," the statement said.”

Can’t help but agree with Ryanair chief here…

The situation is different to the US where I believe all the airlines received funds as a part of the CARES act. Although Airlines like American have been active in paying that money back by raising money in the bond market.

Air New Zealand delays proposed capital raise, govt to extend a previously announced loan facility

Extract of Flight Global: “Air New Zealand has postponed a planned capital raise by three months, to give it more time “to assess market conditions” amid the coronavirus pandemic.

The carrier now expects to complete its equity capital raise by 30 September, instead of 30 June, as earlier indicated.

The New Zealand government, which earlier disclosed its commitment to remaining the carrier’s majority shareholder after the capital raise, will extend a previously-announced loan facility to support the airline through the fundraising.

The loan facility, also known as the Crown Standby Facility, will be increased by NZ$600 million ($423 million) to NZ$1.5 billion. The facility term has also been extended through September 2023, with interest rates adjusted to reflect market conditions.“

Continues here.

*INVESTMENT GRADE*

UK Airports issued debt comfortably this week…

Heathrow placed a EU500m Class A bond maturing in 2030 with a fixed coupon of 1.125%. This bond issue will be rated investment grade and provides enough liquidity for next 18-24 months according to a company statement. It also raised CAD 950m of bonds towards the end of the week.

Gatwick raised £300m of 9 year bonds at UK Gilt+180bps. The deal priced with a coupon of 2.50% for an issue that’s rated Baa2/BBB/BBB+. This appeared to be a very popular deal with book coverage greater than 11x.

Disclaimer: Not investment advice. I own positions in some of the securities listed above. These are my own views and not those of any employer.