Weekly Global Credit Wrap w/e 6 May 2022

Positive real yields, corporate earnings trends, oil price strength and higher trading volatility...

Summary:

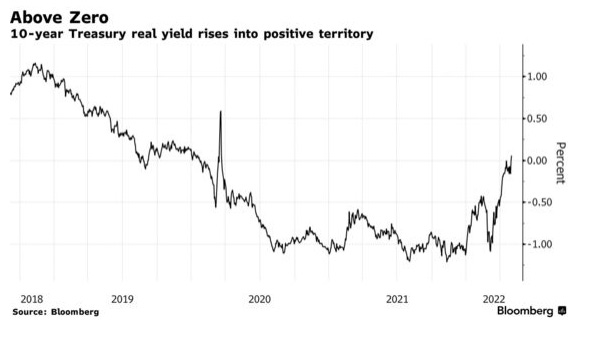

REAL YIELDS – 10 year yield broke above zero and closed at +0.267%. This was likely one of the drivers behind the major volatility in stocks this week.

RATE HIKES + QT – Fed and BoE hiked rates and outlined dates and quantities for their respective QT programs

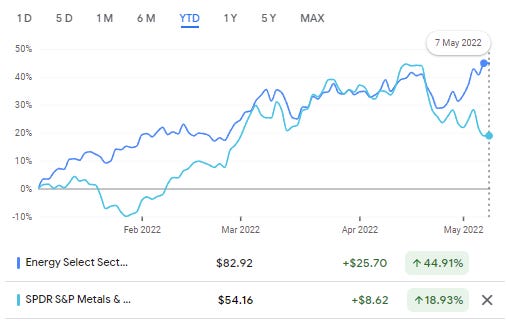

OILS vs INDUSTRIAL METALS DIVERGENCE – Oil price outperforming base metals prices. Number of indicators suggest an extremely tight oil market, whereas metals weakness maybe reflecting global growth concerns

XLE vs XME ETF:

CREDIT FUND FLOWS – Weekly outflows from IG rated bond Funds totaled >$8bn, largest since 2020.

HY - 20bps widening here this week with CDS gauges hitting highest in two years post the Fed meeting. 26% of the high yield market now trades between $80 and $90, the highest percentage on record says a US Bank. European HY underperformed US HY this week.

KEY CORPORATE TRENDS:

Online Retail - Weakness from likes of Amazon, Ebay, Shopify, strength in some in-store retailers (e.g. Next Plc)

Oil Majors – Continue to generate solid FCF in high oil px environment and reduce debt (e.g. BP/Shell)

Oil Services – Earnings report from Transocean reveals a very tight market for offshore drilling rigs

LNG – Cheniere Energy earnings guidance raised. Hoegh LNG signs contract for FSRUs with Germany

Travel / Leisure – Airlines/Hotels/Rental cars posting a mix of strong 1Qs, strong guidance for upcoming quarters

Insurers – Q1 earnings reveal difficult quarter for some investment portfolios due to rising bond yields and Ukraine/Russia conflict

Supermarkets / Convenience stores – First victim of supply chain/cost inflation goes into administration (McColls in the UK).

EM / CHINA:

Very weak Caixin Services PMI print (36.2)

Stronger China Property companies are modestly buying back their Dollar debt (Country Garden/Sino Ocean)

Sri Lanka - China backs Sri Lanka's decision to work with IMF to restructure debt

Private credit – extents its reach into India with Apollo single-handedly financing Mumbai Airport’s private placement

Cemex and Pemex reported figures

Bayport – EM specialist lender issued $300m of bonds (mostly rolled over from existing bonds) at pricing wider than IPT

FINANCIALS – More CoCos called (Santander UK) and a low reset SGD CoCo from HSBC. Q1 earnings reports from banks continue to be solid if not spectacular.

RATINGS – Ford put on positive outlook at Fitch (BB+). Set up to join IG index if stays on course.

TRADING – Trading volatility at highest since 2008 (according to Jane Fraser, CEO of Citi talking about her traders). Also note Tradeweb and MarketAxess, the two publicly listed giants of Bond E-Trading posted robust volume stats for April.

ESG:- Largest ever ESG Eurobond issued, award goes to Tennet..

*MACRO*

10 year real yield broke above zero, first time since March 2020

The below chart is from Tuesday, in fact 10 year real yield closed the week at 0.267%. This is likely to be linked to the huge stock volatility which took place this week.

Other interesting bond market levels hit this week:

Australian 3 year bond and 10 year Italian BTP both went through 3%

Australia: RBA said it will need to raise interest rates further…

as unemployment is forecast to drop to the lowest level since 1974

Fed Meeting Outcome summarised by @Callum_Thomas

BoE will start selling off its £20bn corporate bond portfolio in September - BBG

Extract: “The Bank of England will start selling off its 20 billion-pound corporate bond portfolio in September, unwinding support for the credit market in place since the aftermath of the Brexit referendum.”

U.S. distillate fuel oil inventories have fallen to a 14-year low – Reuters h/t @johnkemp

Extract “…As refiners prove unable to satisfy strong demand from freight hauliers and manufacturers, sending diesel prices surging and pulling crude prices higher in their wake.”

US DOE outlines crude purchase plan to refill SPR after massive drawdown - S&P Platts

Extract: “The US Department of Energy plans to buy back 60 million barrels of crude for the Strategic Petroleum Reserve -- or one-third of the massive drawdown that just started flowing -- at lower prices, likely in the second half of 2023.”

Credit spreads – Notable moves in the week:

CDS:

5 year CDX HY +19bps over week to +480bps, setting up for a run at +500bps?

5 year Xover +35bps wider to +462bps

Cash:

EUR IG +10bps to +161bps

US HY +23bps bps to +402bps

EUR HY +38bps to +488bps

USD Bank Cocos +16bps to +423bps

US IG cash was broadly flat over the week. The immense volatility in stocks also likely played a part in move wider in spreads for the riskier ends of the credit market (HY, EM, Sub Fins).

Bond ETFs – Another down week for most bond ETF, notable moves:

TLT posted a minus 3% TR over 5 days such that it is down 22.8% YTD

IHYG posted a minus 1.7% TR over 5 days and is nearly down 10% YTD (-9.5%)

Other Bond ETFs which I track that were posted a minus 1% or more TR over 5 days included IEAC (European IG Corp bond), EHYB (European Corporate Hybrids), AT1 (Bank AT1 bonds) and IGLT (UK gilts).

While the QT actions/signaling continue to dominate the narrative, other factors such as a risk of a slowing economy and better yields on offer make the case for bonds more nuanced than in the past year or so.

*FINANCIALS*

Insurers’ / Reinsurers investment portfolios dampened by rising rates / higher equity vol

This week, Swiss Re and Beazley were two of the companies that reported YOY declines in investment income. Extract of Beazley comment:

“Our investments lost $92m, or 1.2%, in the first quarter, as US Treasury yields recorded their largest quarterly increase in more than forty years, generating significant losses in our fixed income investments. Inflation concerns were pushing yields higher even before the Russia-Ukraine conflict and this trend has become more prevalent since. We maintained very low duration in our portfolio throughout the period and this has materially improved our investment performance. Market yields are now more than 1.5 percentage points higher than at the end of last year, which will help our return to recover in the remainder of 2022 and into 2023, as well as improving the longer term outlook for investment returns. However, the global economic outlook remains uncertain and further market volatility is likely.”

Santander issues call notice on 7.375% GBP AT1 at first call

These bond calls are no longer really “news”, but fact that banks are calling at first call during periods of high volatility is still somewhat noteworthy. The bond had a relatively high reset of 5 year £ swap + 5.5%.

HSBC issues call notice on SGD 4.7% CoCo bond with low reset

Reset on the bond is 5 year SGD Swap + 2.87%.

“Bank AT1s Face Existential Crisis in Europe Amid Capital Shuffle” - Fitch

Dramatic headline! But this is their summary which they expand upon:

“Additional Tier 1 (AT1) capital faces an existential crisis within European bank prudential regimes, according to Fitch Ratings, as bank supervisors increasingly argue that AT1s do not meaningfully contribute to ongoing loss absorbency and overcomplicate banks’ utilisation of capital buffers during crises. However, changes to AT1s’ regulatory eligibility would require legislative changes, and AT1s would likely be phased out over as much as 10 years.”

Interesting topic and one to monitor…

*IG*

Outflows from US HG funds and ETFs jumped to -$8.16bn for w/e 4 May - Largest weekly outflow since 2020

EDF dialed back a profit warning from March - BBG

BP and Shell both reported strong figures

BP - Debt highlights (so much more in its Q1 release)

Reported a loss for 1Q mainly due to exit from Rosneft shareholding

Net debt reduced to $27.5bn from $30.6bn in 4Q 2021

Net debt fell for the eighth consecutive quarter

Operating cash flow of $8.2bn vs $6.1bn in 1Q 2021

As a side note, its interesting (yet logical) to see Oil Majors go back to re-investing in UK North Sea projects, as evidenced by BP, which is looking to move ahead with plans for the development of the Murlach oil field located in the UK North Sea, with first oil targeted in 2025.

Shell - Debt highlights (again, much more in its Q1 release):

Net debt reduced by ~8%, from $52.6 bn in Q4 2021 to $48.5 bn in Q1 2021

AT&T to Increase Rates on Older Cellphone Plans - Verge

Extract: “In a bid to push people to its newer plans, AT&T is raising the price of some of its older Unlimited and Mobile Share plans. Single-line users will see up to a $6 a month increase, and people with family plans could have up to $12 a month added to their bills, according to Bloomberg.”

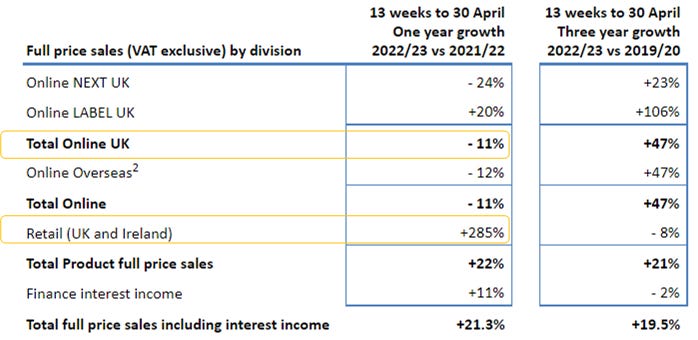

Next Plc (UK clothes retailer) - saw boost in sales in store but drop off in online sales

Source: Next plc

*HY*

Cheniere Reports First Quarter 2022 Results and Raises 2022 Financial Guidance

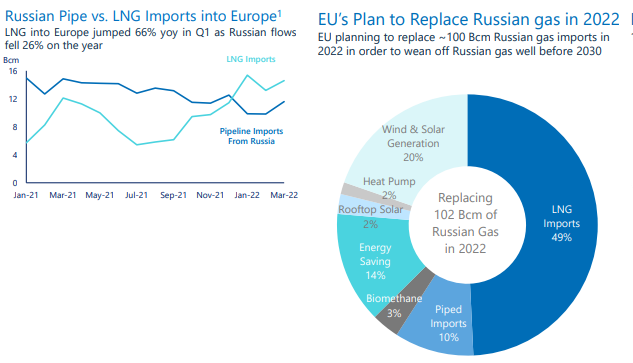

Cheniere’s latest investor presentation contains some useful macro information on LNG supply/demand dynamics in Europe such as that shown below:

LNG Sector - Germany to Charter Two FSRUs from Höegh LNG - Link

Extract: “The German government on Thursday signed agreements for the charters of four floating storage and regasification units (FSRUs), as it works to become less reliant on Russian gas, as FSRUs will enable it to import LNG from other sources.

The agreements were signed for the charters of two FSRUs owned by Oslo-listed firm Hoegh LNG, and two owned by Dynagas. Hoegh LNG FSRUs will be operated by RWE, while Uniper has facilitated the charter of two FSRUs managed by Dynagas Ltd.”

Transocean earnings call highlights for debt investors - Fool.com

“As further evidence that the market has reached an inflection point according to rig broker, Clarksons, for the first time in eight years, new contracts are on average being awarded at higher dayrates than the contract they are replacing”

“We ended the first quarter with total liquidity of approximately $2.6 billion, creating unrestricted cash and cash equivalents of approximately $110 million, approximately $280 million of restricted cash for debt service and $1.3 billion from our undrawn revolving credit facility.”

Energean -New Gas Sales and Purchase Agreement Signed and Karish Project Operational Update

Mathios Rigas, Chief Executive of Energean, commented:

"We are delighted to have signed a new GSPA of up to 0.8 bcm/yr for our flagship assets in Israel, delivering on one of our key milestones for 2022. This is the third in a row for us from the Israel Electric Corporation ("IEC") power plant privatisation programme…I'm pleased to also confirm that the Energean Power FPSO has sailed-away [from Singapore] and we look forward to delivering first gas from Karish, which remains on track for Q3 this year."

IAG, Lufthansa and Air France-KLM signal business travel revival - BTN Europe

Extract: “The region’s leading airline groups all reported strong corporate travel demand, largely due to the continued easing of government-imposed travel restrictions.”

Avis beat expectations on a number of financial metrics -Net Revenue, EBITDA, EPS

Extracts from CEO comment:

We ended the quarter with revenues 77% above the first quarter 2021, at $2.4 billion. Our revenues were driven by rental days as demand improved throughout the quarter and increased revenue per day.

Net income was $527 million and our Adjusted EBITDA was $810 million, our best first quarter Adjusted EBITDA in our history. Utilization for the quarter was 67.4% and in-line with first quarter 2021, showing our fleet is well positioned to meet seasonal peak demand.

Liquidity position at the end of the quarter was approximately $900 million, with an additional $1.7 billion of fleet funding capacity. We have well-laddered corporate debt and no meaningful maturities until 2024.

Hilton Worldwide seeing rebound in demand after Omicron - Barrons

CEO comment: “We think we’ll probably have the biggest leisure summer we’ve ever had. There’s still a lot of people that really want to get out and have experiences.”

Revpar rose 80.5% for the quarter versus the same period of 2021 due to increases in both occupancy and average daily rates

RevPar was down 17% compared with 2019 or prepandemic levels

U.S. occupancy rates rose to 61.8% in the first quarter as people started traveling more.

Demand from business travelers is likely to get stronger in the second half of the year, the company said. Revenue from large corporations was just 12% below the 2019 level in March, while Hilton said it noted continued strength in accounts for small and medium enterprises.

UK Convenience Store Chain McColls appoints Administrator, shares suspended

Extract from ES: “Convenience chain McColl’s confirmed it will collapse into administration, putting 1,100 shop and 16,000 workers at risk. McColl’s has struggled financially in recent years after witnessing soaring costs due to supply chain disruption, inflation and its large debt burden.”

However, after failing this week to come to a deal with its major partner; Supermarket Morrisons, it seems EG Group led by the Issa brothers are reported to be interested in acquiring an interest in the business according to the BBC post the administration.

*EM*

China backs Sri Lanka's decision to work with IMF to restructure debt – News 1st

Extract: “Ambassador to the Republic of China in Sri Lanka Qi Zhenhong met with Finance Minister M.U.M Ali Sabry, PC at the Ministry of Finance on Monday…Ambassador Zhenhong reiterated China’s full support to Sri Lanka in resolving the present economic issues and also reiterated that China clearly supports Sri Lanka’s decision to work with the IMF in restructuring its debt. Ambassador Zhenhong also assured Minister Ali Sabry that as a major shareholder of the IMF, China is willing to play an active role in encouraging the IMF to positively consider Sri Lanka’s position and to reach an agreement as soon as possible. “

Mumbai Airport Gets $750 Million in Apollo Private Placement - BBG

This development was after Mumbai Airport tried to issue public bonds earlier in the year, but did not go ahead.

Cemex reported earnings, highlights on debt position - IR

Net debt increased on a sequential basis primarily due to the negative FCF and share buybacks in the quarter

Consolidated leverage ratio ticked up

No substantial refinancing needs for the next three years

A strong liquidity position and minimal exposure to interest rates, as close to 90% of its debt is at a fixed rate.

During the quarter, Cemex launched a tender offer to purchase up to $500m of three of its notes…through which it repurchased approximately $440 million in notes at a discount. This exercise should result in more than $11 million dollars in annual interest expense savings and was be funded through its revolving credit facility at a lower rate than the coupon of the notes.

Pemex Swings to Highest Profit in 18 Years Amid Oil Rally - BBG

Pemex reported highest net income since first quarter of 2004 Oil output has stabilized with shallow water, onshore drilling.

Helios Towers - 1Q figs and capital markets day - IR Site

Debt highlights →

Net leverage increased by +0.7x YoY and +0.1x QoQ to 3.7x, the low end of the Group’s medium term target range of 3.5 - 4.5x

Liquidity of $483m cash on balance sheet and c.$345m undrawn debt facilities across the Group; c.$830m in available funds

Bayport (EM payroll lender) issued two bonds totaling $300m - PR News Wire

Most of the bond was thought to be rollover of existing bonds but an impressive feat to print the size they did during a volatile week for markets. Final pricing was wide of the initial price guidance, following a trend in the broader HY markets. The issue followed the small Green bond raised by Access Bank (Nigeria) the prior week.

*CHINA*

China: Caixin Apr. Services PMI registered 36.2, worst month on record (except Feb 2020)

Markit summary: “Quickest fall in service sector output for over two years as COVID-19 restrictions tighten, decline in new business also gathers pace, employment falls only slightly. “

Stronger China Property Firms buy back Dollar bonds

Bloomberg reported that Sino Ocean and Country Garden have been partially buying back bonds:

→ Sino-Ocean Capital has bought $67m of two dollar bonds issued by unit Mega Wisdom Global, according to a late Thursday filing to Singapore Exchange.

→ Country Garden reported that it has repurchased a total of $55.7m senior notes that were due in 2022, 2023 and 2026. Note that COGARD’s bond maturing on 25 July 2022 traded as low as 80 only in March 2022…now trades at 98.

*RATINGS*

X-S&PGR Revises EnQuest Outlook To Pos; Unsec Notes Up To 'B'

S&PG Places T-Mobile Rtgs On Watch Pos On Strong Q1 Results

*CREDIT TRADING*

Citi Traders Are Dealing With the Highest Volatility Since 2008 - BBG

Traders are coping with inflation that’s at its highest level in a generation and investors who are increasingly worried about the likelihood of a global recession, Fraser said Monday at the Milken Institute Global Conference in Beverly Hills, California. As an example of volatility, she mentioned trading on Friday, when bonds sold off at the same time as equities. Normally, the two have an inverse relationship.

MarketAxess and Tradeweb Volume Stats

MarketAxess highlights:

U.S. high-grade ADV of $6.0 billion, up 14%; estimated market share of 22.6%, up from 21.0%.

U.S. high-yield ADV of $1.6 billion, up 6%; estimated market share of 16.9%, up from 15.0%.

Emerging markets ADV of $2.9 billion, up 15%, with estimated market ADV down 11%.

Eurobond ADV of $1.4 billion, up 1%, with estimated market ADV down 20%.

$25.5 billion in U.S. Treasury ADV, up 91% with record market share.

*All comparisons versus April 2021 unless otherwise noted.

Tradeweb highlights:

Total trading volume for April 2022 was $21.6 trillion (tn). Average daily volume (ADV) for the month was $1.09tn, an increase of 22.1 percent (%) year-over-year (YoY).

U.S. government bond ADV was up 41.5% YoY to $135.9 billion (bn),1 and European government bond ADV was up 18.2% YoY to $33.5bn.

Fully electronic U.S. Credit ADV was up 23.0% YoY to $4.0bn and European credit ADV was down 0.2% YoY (up 8.1% YoY in EUR terms) to $1.9bn.

*BUYSIDE*

Apollo to offer products to wealthy investors next year - MSN

Private Credit - BlackRock wants to raise about US$ 4bn for the latest vintage of its Global Credit Opportunities fund - BBG

Extract: “The world’s largest asset manager is looking to raise about $4 billion for the latest vintage of its Global Credit Opportunities fund, as the market for private credit instruments swells to more than $1 trillion.

BlackRock has already raised about $2 billion -- half of the targeted amount -- for the new private credit fund….”

Third Point HF - April update shows Fund increased allocation to structured credit

Structured credit allocation has been increased from 19.1% as at 31 December 2021 to 23.2% in April 2022 (21.9% in March 2022). The increase appears to be driven by an increase in exposure to Residential Mortgage ABS. Source: https://thirdpointlimited.com/portfolio-updates

*ESG*

TenneT successfully issued the largest corporate Green Eurobond transaction ever - Tennet

*LINKS*

Corporate bonds now falling as much as they did in the March 2020 crash h/t @TaviCosta

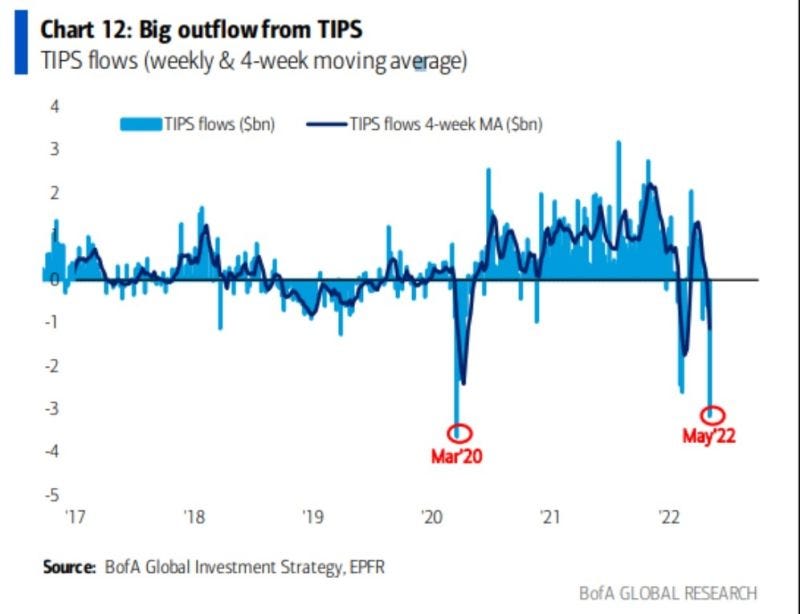

Outflows from TIPS, part of wider market liquidation or something else? h/t @MikeZaccardi / BoFA

4 Takeaways from Milken Conference - Barrons

Rick Rieder post NFP

Oah Hill Advisors CEO at Milken - “No imminent distress” in US markets