Weekly Global Credit Wrap w/e 4 March 2022

Tensions drive big moves in EM and heightens rates vol

*OVERVIEW/KEY MOVES*

CDS Indices - Key 5d Moves + commentary

Xover +67bps to 399

Sub Fins +40bps to 182

CDX EM +73bps to 73

CDX HY +33bps to 392

Moves in Xover, Sub Fins and EM more pronounced than in US HY.

Cash Credit spreads - Key 5d moves + commentary

US IG +9bps to 130

US HY +23bps to 376

EM USD +63bps to 410

Pan Euro HY +49bps to 465

CoCos +80bps to 446

A number of absolute credit spread indicators (EUR HY, EM HC and CoCos) above 400bps now. Meanwhile US HY staying below 400bps likely reflecting the more US domestic focus which some maybe considering a shelter away from Ukraine/Russia volatility.

Bond ETFs - Key 5d moves + commentary

Some higher quality bond ETFs positive over the past 5 days:

UK Gilt ETF (IGLT) +2%

iShares TIPS Bond ETF (TIPS) +0.7%

IG European Corp bond (IEAC) +0.6%

Despite some good flow information the prior week re LQD (US Investment Grade Bond ETF), it posted negative returns over 5 days and is down 6.3% YTD still.

US HY Bond ETFs are outperforming European ones, e.g HYG (-0.99%) vs IHYG(-1.35%).

EMB (HC EM Sovereign Bond ETF) now posting double digit losses YTD (-12.6%) after a minus 4.3% total return over 5 days. Drilling into the weakness it looked like Russia and Ukraine generated total returns of more than minus 50% each (over 5 days!) and dragged down a few other nations’ bonds which also saw double digit negative returns over 5 days; Egypt, Ghana and Pakistan. Possible reasons behind this are touched upon later.

The immense rates volatility YTD has weighed on rates and credit total returns. FinTwit (@callum_thomas) has highlighted the break out in the MOVE volatility index and historical patterns vs HY credit spreads…will history repeat?

*MACRO*

Fed - J Powell Testimony summarised by @SteveMatthews12

1) FOMC plans quarter-point hike in March;

2) Half-point hikes will be mulled if needed;

3) Balance sheet shrinkage after rate liftoff;

4) BS adjustment could take 3 years;

5) Ukraine impact on U.S. highly uncertain;

6) Elevated inflation expected to decline this year;

7) Fed has anti-inflation tools and will get price gains back under control;

8) Labor market is extremely tight, at full employment;

9) Fed's goal is soft landing for economy, not recession; that likely can be achieved.

Link to original tweet:

Fed Bostic favours 25bp hike in March. He is open to 50bp if monthly inflation readings fail to decline

Bank of Canada Raises Policy Rate to 0.5%, Sees More Hikes Ahead - BBG

Signs of stress emerging in the functioning of US Treasuries- BBG Quint

Extract: “Among the gauges of stress in the Treasuries market recent days:

-A measure of market depth - or the ability to trade without substantially moving prices compiled by JPMorgan Chase & Co. has deteriorated to levels similar to around April 2020, just after the rupture in trading when the Covid crisis hit

Counterparties to repurchase agreements are failing to follow through on their obligations at a level unseen in almost two years, a sign they’re having difficulty obtaining the Treasuries they need

Dealer trading in off-the-run securities -- those that aren’t the current benchmarks for the various maturities -- has tumbled, according to Bloomberg Intelligence analysis”

*ENERGY/INFLATION*

Wheat spiked to fresh 14-year high on deepening supply fears

Oil firmly above $100/bbl:

WTI Oil @ 116

Brent Crude @ 118

Costco pressured by supply bottlenecks - earnings transcript

CFO - “Inflation, of course, continues, as evidenced by our LIFO charge. The inflationary pressures that we and others continue to see include higher labor costs, higher freight costs, as well as higher transportation demand, along with the container shortages and port delays that I just mentioned, increased demand in certain product categories, various shortages of everything from computer chips to oils and chemicals to resins, higher commodity prices from foodservice oils to additives and motor oils, to plastics, to detergents, to paper products as well, on the fresh side proteins and butter and eggs and things like that, not very different than what you hear and read and see from others.”

Turkey's inflation surges to 54%, highest in 20 years | RTRS

McDonald’s Japan to Raise Burger Prices This Month as Costs Soar

Germany orders €1.5 bn of non-Russian liquefied natural gas (LNG) | RTRS

Wintershall Dea stops payments to Russia, writes off $1.1 bln Nord Stream 2 loan | RTRS

Russia's War on Ukraine Could Triple Ocean Shipping Rates Say Expert - BI

Bofa via ZH Charts Stagflation from history

*NEW ISSUES*

Ukraine Raised UAH 8.143bn via Selling 2-Month 10% Paper, 1Y 11% War Bonds;

16 firms issued bonds in US IG market on Thursday, busiest day in 2022 - BBG

3 March - Trafigura Group Pte Ltd signs USD5.3 billion European Syndicated Revolving Credit Facilities - Link

*RUSSIA / UKRAINE*

World Bank Ukraine loan disbursement grows to 460 mln euros-sources | RTRS

S&P slashed Russia's credit rating by eight levels to CCC-

Some Russian Bond Trading Defrosts as Investors Hunt for Deals - WSJ

Gazprom Paves Way to New China Gas Deal as Sanctions Hit Russia - BBG

Gas giant signed contract to design link to China via Mongolia

New pipe to China would enable 50 bcm/year of extra gas flows

Gazprom 6.51% March 7 2022 bonds due March 7, 2022 jump 50pts on possible repayment article in BBG

Extract: “The company wired the cash on Feb. 28 to the settlement bank, which will probably release the funds on March 4, a person familiar with the matter said, declining to be identified because the information is private.”

Wall Street Is Pouncing on Russia’s Cheap Corporate Debt - BBG

Extract: “Goldman Sachs is primarily asking for corporate debt from the likes of Evraz Plc, Gazprom PJSC and Russian Railways that matures within the next two years, and has made bids for Russian sovereign notes, the people said.”

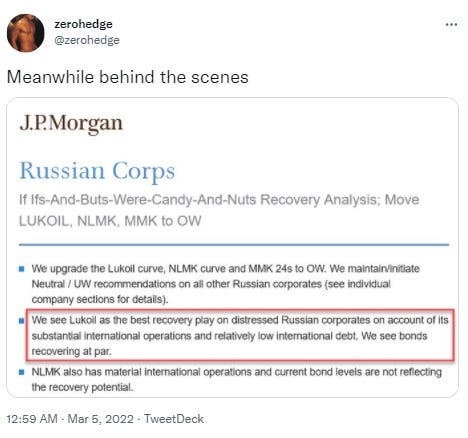

Some strategists suggesting buy recommendations in specific Russian Credits - Zerohedge

EU seeking to remove Russia’s most-favored nation status at the WTO

Georgia and Moldova submitted formal applications to join the EU

CMA CGM Suspends All Russia Bookings Until Further Notice - CNBC

Russia's biggest shipper Sovcomflot sees business dwindle as buyers snub Russia oil - S&P Platts

*EM / ASIA*

Hong Kong’s Economic Activity Slumps to 22-Month Low - The Standard

Vedanta Pays Out Dividend for a Third Time This Year - Said to help meet debt obligations at Parent - BBG

Extract: “…Vedanta Ltd. will pay a dividend to investors for a third time this financial year as a rally in commodity prices boosts earnings, with the payout potentially helping relieve some of the debt-repayment pressure on its parent.”

A number of EM Sovereigns (outside of restructuring candidates) have traded down to the 60 cents in the Dollar (or lower)

There have been some precipitous drops in mainly B rated EM sovereigns YTD, e.g:

Source: BBG

The more recent moves can be attributed to second order effects of the Russian invasion of Ukraine, e.g. the dramatic increase in wheat + oil and gas prices.

Clearly, importers are not standing still and are looking at alternative sources of wheat. This is where grain traders and commodity traders more broadly are likely to do very well as they use their extensive networks to source commodities. A longer term trend maybe more countries “growing their own” so to speak.

Other factors weighing on EM bonds could be; fund outflows, lowered risk appetite due to problems in other parts of portfolios (Ukraine/Russia exposure).

JPMorgan to Liquidate $454 Million Emerging Markets Debt Fund - BBG

Kosmos Energy (E&P Firm) reported figures Key Extracts from conf call:

“On production, we hit our year-end production target of 75,000 barrels of oil equivalent per day

Producing assets generated strong free cash flow of around $175 million during the year, excluding working capital, in line with guidance.

We have taken advantage of higher commodity prices to put in hedges at significantly higher floors and ceilings than we had in 2021.

Around 55% of our production is hedged with an average ceiling of around $80 per barrel with the rest exposed to current prices.

…Liquidity to over $750 million available at year end

we materially reduced leverage during the year, ending at around two and a half times as planned.

This quarter, we expect to complete the refinancing of the RCF pushing that maturity to late 2024.”

Sri Lanka CBSL hikes rates to tame inflation; urges govt to act | RTRS

Extract: “Sri Lanka's central bank sharply raised interest rates on Friday to staunch growing inflationary pressures and urged the government to consider measures including curbing non-essential imports and raising fuel prices to reduce pressure on the ailing economy. The Central Bank of Sri Lanka (CBSL) raised the standing deposit facility rate and the standing lending facility rate by 100 basis points (bps) each to 6.50% and 7.50%, respectively. The median estimate in a Reuters poll of 13 economists was for the two rates to be raised by 50 bps each.”

*FINANCIALS*

AT1s – A number of issuers published call notices for their instruments

Santander, ING, Deutsche Bank and Danske were just some of the issuers that have recently called CoCos. Remains to be seen where proceeds from these bond redemptions will be allocated, bearing in mind the halt in primary AT1 issuance, but also the presence of fund outflows.

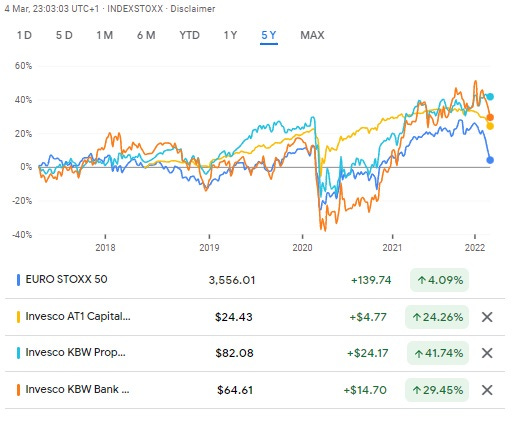

Eurostoxx Banks index led financial focused ETFs down this week

Google Finance struggles with showing full names, so the below instruments are:

Eurostoxx 50 Index

Invesco AT1 ETF

Invesco KBW P&C Insurers index

Invesco KBW Bank Index

Note, the performance percentages are over 5 years.

A number of European Banks reported / had CMDs this week and touched on their Russia exposure

Commerzbank (CMD) - Commerzbank said on Tuesday that its exposure to Russia and Ukraine were manageable, but that it would “continuously adapt” its strategy and risk assessment as events unfold. The German lender said that its net Russian exposure is 1.3 billion euros ($1.45 billion) | Reuters

Soc Gen - With a CET1 ratio of 13.7% at 31 December 2021, i.e. a buffer of around 470 basis points above the regulatory capital requirement, the Group has more than enough buffer to absorb the consequences of a potential extreme scenario, in which the Group would be stripped of property rights to its banking assets in Russia, with a capital impact estimated at around -50 basis points of the CET1 ratio and no effect on the payment of the dividend for the year 2021. | Statement

ING - It (ING) said it has 5.3 bn euros in loans to Russian borrowers, representing 0.9% of its total group loan book. In Ukraine it said it had 500 million in loans, representing 0.1% of its loan book. | Reuters

Admiral’s (UK Motor Insurer)' shares tank after reporting figures taking competitor Direct Line down with it

Write up by Sharecast

*CHINA*

Immense volatility continues in China Property bonds, but there was a bit of relief for some issuers after news of M&A funding from state backed Chinese banks for two of the larger developers.

China developers Country Garden, Midea secure $3.3 bln M&A funding | RTRS

Chinese property developers Country Garden and Midea Real Estate secured separate mergers and acquisition (M&A) financing facilities worth 21 billion yuan ($3.3 billion) in total, sending their shares sharply higher in Hong Kong.

The financing accords, both with state-backed China Merchants Bank, comes as Beijing steps up efforts to stabilise and tighten control over the property sector, accounting for a quarter of its economy, which has been roiled by the debt crisis at heavyweight developer Evergrande.

Howard Marks Calls China Market a ‘Buy’ in Oaktree WeChat Debut – BBG

Oaktree Capital Management’s co-founder vowed to participate in China’s market in the long run by “always buying,” as the distressed-debt investor launched a WeChat social media account.

*HY*

US HY market functioning better than EUR HY Market currently

Yet another “donut” for European HY with no issues priced. Meanwhile the US HY market saw a number of issuers price deals including Bellring, Macy’s and Energizer. In fact, Energizer upsized its deal size. BBG reported that it’s the first back to back weekly gains for the US HY sector since December, with a supportive narrative being J Powell’s lean towards a 25bps hike and the more domestic nature of the US HY market.

Occidental Petroleum bonds advance on $2.5B buyback effort - S&P Platts Global

On a related note, note Berkshire Hathaway re-initiated a large stake in Oxy:

AMC Cinemas reported $1.8 bn of cash and undrawn revolver on its earnings call

Gunvor (Commodity Trader) - Makes statement on Ukraine War and extent of Russian exposure/dealings - Gunvor Group

*RATINGS*

Moody's affirms BP's rating and maintains stable outlook - Link

S&P Ratings affirmed BP's A- long-term and A-2 short-term ratings, with a stable outlook

EDF Outlook to Negative by Fitch; L-T IDR Rating Affirmed - Only agency not to cut in recent round of ratings updates.

Fitch Downgrades Ukrainian Railway to 'CCC' on Sovereign Rating Action

Fitch Downgrades Shimao Group to 'CCC' on Rising Refinancing Risk; Off Rating Watch Negative

Moody's upgrades Lenovo to Baa2; outlook stable

*TRADING*

Tradeweb reports Total Volume of $22.6 Trillion and Average Daily Volume of $1.17 Trillion in February 2022 - Link

Highlights:

U.S. government bond ADV was up 30.4% YoY to $153.8 billion (bn),[1] and European government bond ADV was up 24.9% YoY to $42.0bn.

Fully electronic U.S. Credit ADV was up 27.0% YoY to $4.0bn and European credit ADV was up 1.0% YoY to $2.1bn

MarketAxess Announces Monthly Volume Statistics for February 2022

· Total monthly trading volume +17% to $716.8 bn, compared to February 2021, driven by a $110.3 bn, or 29%, increase in rates trading volume to $495.4 bn.

· Total monthly credit trading volume of $221.4 bn, decreased 2%, compared to February 2021; combined estimated U.S. high-grade and U.S. high-yield TRACE volume down 8%.

· 92% of the credit trading volume on the platform during the month involved institutional investor clients.

Full release:

*COVID*

US warns against Hong Kong travel over Covid rules, child separations - AFP