Weekly Global Credit Wrap w/e 30 April 2021

April scorecard, bond trading platforms, Tullow Oil..

*OVERVIEW*

Looking at monthly returns for April, it seems most fixed income subsectors generated positive returns barring German Bunds.

In fact most risk assets posted positive returns in April, confirming predictions by many strategists about the likelihood of positive returns from what has typically been a seasonally favourable month.

Source: BBG, Creditsights, Yahoo Finance

Within credit markets, spreads can only seem to go one way (lower) at the moment. Bloomberg journalists are going on overdrive to point out how expensive HY markets are currently, and they are not wrong. CCC bond spreads went below 500bps, that has only happened twice before in the last two decades according to the chart below.

With all this signaling, will credit market participants be ready to buy the dip when the inevitable sell-off comes? We shall see…

*MACRO*

Euro area bonds posted poor returns last week - Reuters

According to Reuters, Euro area government bonds notched up their worst monthly performance against U.S. Treasuries in a year. Extract from Reuters below:

“Ten-year U.S. Treasuries' yield premium over equivalent German bonds, a gauge often used to measure differences in economic outlook, shrank in April by the most since last March. It fell as low as 179 bps, from the highest in more than a year at over 200 basis points in early April.

The divergence is partly down to a Treasury rally that knocked U.S. yields off 14-month highs. But Bunds, with yields back to their highest since last March, have underperformed British, Australian and Japanese debt too.”

The reason for the weakness appears to be the rising pace of vaccinations in the region, after a slower start than the UK and US. Rising yields have direct implications for very low coupon European Corporate Debt, particularly in the IG Credit space.

FCA consultation on rolling back key Mifid-II reforms for UK Market participants

There is potentially great news for UK buyside participants with the FCA initiating a consultation on whether FICC research should be made free once again, rolling back regulations from European initiative Mifid-II.

Extract from Lawyers Ashurst on the topic:

“The FCA has issued a consultation paper "Changes to UK MiFID's conduct and organisational requirements" (CP 21/9), setting out proposals to roll-back MiFID II on research and best execution.

The changes follow the publication of the so-called EU MiFID Quick Fix rules in the Official Journal, which also contain relaxation of MiFID rules in relation to research and best execution reports (although there is some divergence between the EU and the UK).

….More significantly, Fixed Income, Currencies and Commodities (FICC) research is moved outside of the research rules when provided in connection with a "investment strategy". This could have a bigger impact in the FICC market.

….FICC instruments. The FCA is proposing to creating an exemption from the inducements rules for third party research received by a firm providing investment services or ancillary services to clients, where it is received in connection with an investment strategy primarily relating to FICC instruments. The FCA considers that FICC transactions are usually not paid for by an agency commission to the broker (and so "opacity risks" do not arise for these as they may do with transaction fees and research costs for equity research). Many of these arguments were put during the lead up to MiFID II… And it was always suggested by some that FICC research was not properly considered by MiFID II reforms.

Independent research providers exemption. The FCA is planning to loosen the restrictions for independent research providers who do not engage in execution services (and are part of a financial services group that includes an investment firm that offers execution or brokerage services).

Openly available written material. The FCA is proposing to exclude from the inducement rules material that is made openly available from a third party to any firms wishing to receive it, or to the general public. For these purposes, “openly available” means that there are no conditions or barriers to accessing the information (e.g. login, submission of user information).”

*FINANCIALS*

UK/European Bank earnings largely solid

Most UK/European banks have now reported their Q1s. Main themes that played out were; lower loan loss reserves, (some) investment bank divisions boosted by capital markets activity (e.g. SPAC issuance) and some surprising winners (DB) and losers (Credit Suisse). Yahoo Finance did a good summary, but its worth looking at each Bank’s respective comprehensive materials to assess the specifics.

Chart of DB vs CS shares

*HY*

There have been 41 first-time borrowers in US HY space YTD - BBG

Bloomberg wrote about how there are 41 first time borrowers in the US HY market. Most of these issuers previously only had loans outstanding. This is just a small part of a longer term trend post GFC where more issuers have entered the public bond markets. I believe this is beneficial for bond market participants as it expands the universe of tradeable bonds, improves tradeable relative value opportunities and increases price transparency. These trends benefit the main bond trading platforms out there too, I talk about this later when I discuss how MarketAxess and Tradeweb did during Q1.

Hurricane Energy - Proposed financial restructuring with convertible bond holders

North Sea Oil & Gas firm Hurricane Energy has agreed a proposed financial restructuring plan with a majority of convertible bondholders, who would take control of the London-listed firm. This is not a situation I have followed closely but it demonstrates what can go wrong with some of the exploration only type players in the oil and gas space. Taking a very high level look at the situation, the restructuring is being proposed due to an expectation that it will be unable to pay back its 2022 convertible bonds in full.

The proposed restructuring will likely provide some useful information to new and old investors in the energy bond sector.

The main components of the Restructuring are as follows:

The Company will execute a debt for equity conversion, which entails (amongst other things):

A $50 million release of the principal amount outstanding under the Convertible Bonds in exchange for the issue of ordinary shares in the Company (the "Exchange Shares") comprising 95% of the fully diluted pro forma equity of the Company immediately following the Restructuring.

An amendment to the terms and conditions of the remaining $180 million of Convertible Bonds in accordance with the revised terms detailed below, including the provision of security and subsidiary guarantees.

The Hurricane Energy statement goes into further detail regarding the proposed restructuring.

*BOND TRADING PLATFORMS*

I’ve dedicated some space here to the Q1 figures of two of the main bond trading platforms; MarketAxess and Tradeweb. Their results were not really discussed in the the financial press in the same amount of detail as the results for the big bank FICC trading desks.

The innovative solutions that MarketAxess and Tradeweb bring to the fixed income market place have profound implications for all current and future bond market participants spanning brokers, credit salespeople, dealers, traders, active and passive managers and just liquidity providers / takers more generally. The rise of trading on these platforms makes me start to question some age-old credit market conventions:

Dealing costs in credit should come down further - Bid/ask spreads should keep coming down as transparency around where bonds are ACTUALLY trading are made more transparent by these platforms in conjunction with help from systems like FINRA’s TRACE and Mifid-II’s APAs. During the volatile Q1/Q2 2020 period, I frequently found myself trawling through TRACE history and data provided on some of these systems to assess where the real markets were in certain securities, as dealer pricing could vary a lot between firms.

Will dealer pricing be replaced by Platform pricing? - I.e. instead of relying on dealers setting prices, could we get to a point where the platform sets indicative prices based on where ALL liquidity providers are trading (i.e buyside, sellside, alternative liquidity providers). To an extent I feel some of the “commercial” dealers are offering this sort of pricing anyway already.

Dealer balance sheet becomes less of a constraint - As buyside and alternative liquidity providers are allowed to put up more and more indications of interest (“IoIs”) or even firm pricing on a system, it should become easier to bypass the traditional bottleneck of investment bank dealer balance sheets. We are not yet there yet with this phenomenon since all-to-all trading relies on there being another side (buyside counteparty) to every trade, what can be referred to as “immediate liquidity.” This is why the dealer is able to make a spread since they are facilitating some element of market making i.e. being able to bid some inventory albeit in relatively small size in relation to the size of the bond market.

These aspects all have implications for credit markets during periods of stress. I.e. If the usual bottlenecks/limitations of bond dealers (buyside being hostage to dealer pricing / balance sheet restrictions) are less of a problem, could this reduce periods of extreme illiquidity / large market wide price gapping?

We are yet to see if this is the case, but one of the things we can glean from the March 2020 credit market meltdown and then subsequent melt-up is that credit market moves are much more rapid compared to history.

I believe that the bear story around contracting dealer balance sheets (post GCF) will hold less and less credibility as market participants reduce their reliance on dealers and instead find liquidity from a variety of providers on these types of platforms.

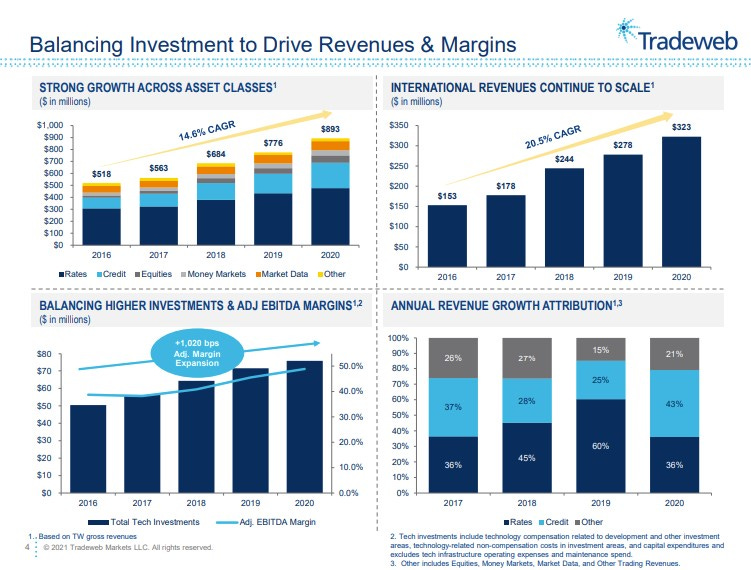

Tradeweb Q1

There is a lot to digest in here, but some of the key highlights include:

Credit posted another record quarter, with revenues growing 37.8% year-over-year

New quarterly (revenue) records for US electronic investment grade and high yield trading

TW is consistently hitting 10% electronic share milestone in investment grade credit

Tradeweb facilitated a record $70 billion in portfolio trades in Q1 2021

In the US, TW estimate that the industry portfolio trading now regularly comprises 4% to 5% of TRACE versus 2% at the beginning of 2019

Source: Tradeweb Q1

Bloomberg, MarketAxess, Tradeweb and Liquidnet seem to be the main competitors in the Fixed Income trading domain currently. Being a user of 3 of those systems, I feel that Bloomberg has some catching up to do with respect to the innovation and user interfaces of the other systems. However, as an all-in solution (news, bond descriptions, IB chat, bond data), Bloomberg is still a formidable system to beat. A key advantage of the competing systems like TW and MarketAxess is that they are free to most buyside users (except for the individual bid/offer trade costs). The billion dollar question is if (when?) will these strong competing forces force Bloomberg to reduce its prices and / or update its interface to be more hi-tech like its competitors?

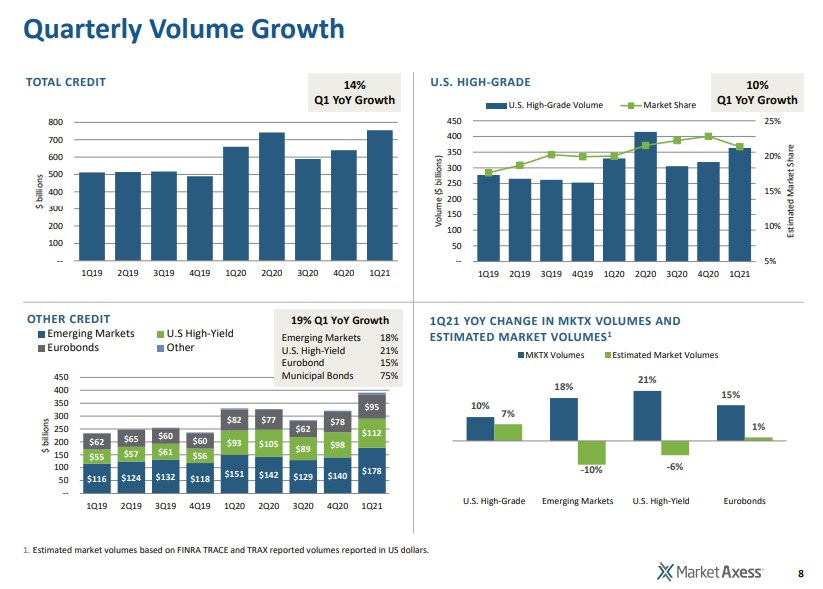

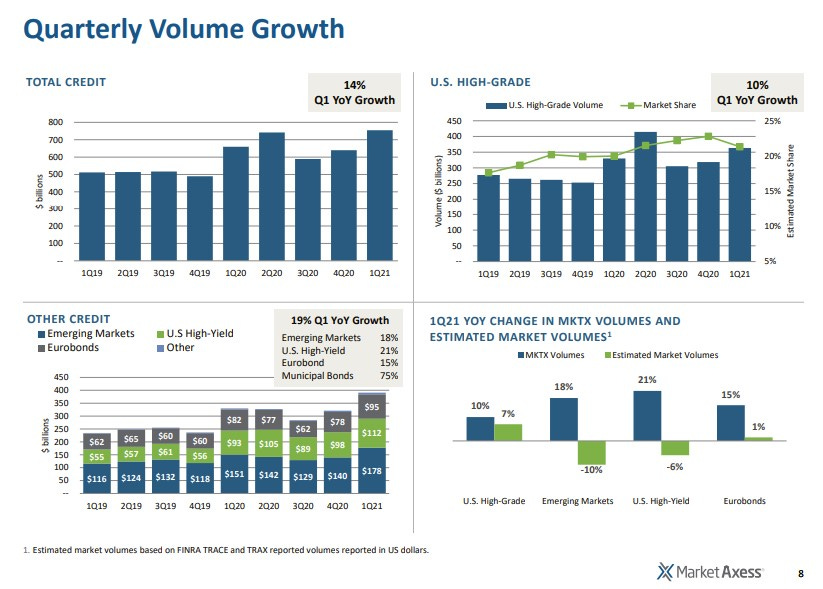

MarketAxess Q1 (released 22nd April)

Extracts of conference call:

“Business thrives when credit spread volatility increases”

“During Q1 last year, credit spread volatility was 10 times greater than this year, and credit spreads in high-grade were nearly 200 basis points wider. “

Open Trading (all-to-all marketplace) volumes grew 20% year-over-year

Open Trading set new records this quarter with an average of 34,000 orders per day totaling over $19 billion in notional value per day in credit products, high grade, high-yield, and emerging markets

In the first quarter, US credit volume from international clients was up 23%, emerging markets volume increased by 22%, and Eurobond volumes increased by 13%

Automated trading volumes rose to $39 billion in the first quarter, up from $31 billion in the first quarter of 2020

https://investor.marketaxess.com/static-files/c050bf47-07bc-4bdb-aa8d-1950686717ef

*EMERGING MARKETS*

Ukraine Sovereign came to the new issue market just as tensions with Russia faded…

On Monday, Ukraine successfully issued an eight year bond at 6.875% (tightening in from pricing talk of “low 7s”), only a few days after some Russian troops were removed from the border with Ukraine. Ukrainian corporates also moved off recent lows after tensions faded temporarily with Russia.

“How Qatar Airways, With Its Covid-19 Playbook, Dethroned Emirates as Biggest Long-Haul Airline” - WSJ

WSJ had an interesting story on how Qatar Airways through the pandemic overtook Emirates to be the largest long-haul airline. Some extracts of the article below:

….Qatar is flying planes that are often near-empty on routes around the globe to increase market share. It is using a downsizing at Emirates to hire staff. And while other airlines have reduced services to markets closed by Covid-19, state-backed Qatar is pursuing new landing rights to emerge stronger post pandemic.

In the past 12 months, Qatar has flown more seats further than any other airline on cross-border routes, according to data firm OAG.

In the week starting Monday, the carrier is scheduled to fly more than twice the international capacity of Air France, over two-thirds more than Delta Air Lines Inc. and over 13% more than Emirates. Across both domestic and long-haul travel, American Airlines Group Inc. remains the world’s largest flier.

“Regardless what will happen across the world, there will always be markets where people want to travel,” Mr. Al Baker (Qatar CEO) said. “We try to take every single dollar that is on the table.” Qatar’s aircraft are currently 40% full on average, with some flights operating around 15%, he added. The state-backed airline can afford to expand because gas-rich Qatar is one the world’s wealthiest nations.

It will be interesting to see how Emirates and other airlines react to Qatar Airways tactics here. I believe this is a phenomenon we will see more and more of as companies switch from playing defense to offense as they shake off their woes from the pandemic.

Cemex targeting investment grade rating by 2023

Cemex, a stalwart amongst EM Corporate issuers announced Q1 results. One of the key comments made by management was around securing an investment grade rating in the near future. Extract:

“We are quite pleased with our first quarter results where we achieved some important milestones and advanced significantly against our Operation Resilience goals, despite persistent challenges from COVID in many markets” said Fernando A. González, CEO of CEMEX. “First quarter performance convinces me that we should be entering a period of sustainable growth for our major markets and we will likely reach two of our Operation Resilience goals well in advance of the 2023 timetable: achieving an investment grade capital structure and a higher than 20% consolidated EBITDA margin…

Net debt and leverage were reduced materially during the first quarter. Net debt plus perpetuals decreased US$547 million, while leverage ratio was reduced to 3.61 times, almost half-a-turn reduction compared to fourth quarter of 2020. ”

Cemex has been very active recently in sorting out its capital structure (redeeming its old high coupon debt and terming out its debt maturity profile). Please see its Q1 report for more details.

Tullow Oil New issue - Decent test of the market depth coming up…

In what is one of the most talked about credit stories within HY and Emerging Markets, Tullow Oil proposed a hefty $1.8bn debt issue to refinance some of its near term debt. This from the company:->

29 April 2021 - Tullow Oil plc (the "Company") announces today that it has commenced an offering of senior secured notes due 2026 (the "Notes") and has received $600 million of commitments in respect of a super senior revolving facilities agreement maturing in December 2024, comprised of (i) a $500 million revolving credit facility and (ii) a $100 million letter of credit facility (the "Revolving Credit Facility" and together with the offering of the Notes, the "Transactions").

The Notes and the Revolving Credit Facility will be senior secured obligations of the Company and will be guaranteed by certain of the Company's subsidiaries.

Use of Proceeds

The Company intends to enter into the Transactions and use the proceeds from the offering of Notes, together with cash on hand, to extend the maturity profile of its indebtedness. These transactions are expected to be net leverage neutral by:

(i) repaying all amounts outstanding under, and cancelling all commitments made available pursuant to, the Company's existing Reserves Based Lending Facility,

(ii) redeeming in full the Company's $650 million aggregate principal amount of 6¼% Senior Notes due 2022 at a redemption price of 100% of their principal amount plus accrued and unpaid interest and additional amounts, if any, to the date of redemption,

(iii) at their maturity, repaying in full and cancelling the Company's $300 million aggregate principal amount of 65/8% convertible bonds due 12 July 2021, and

(iv) paying fees and expenses incurred in connection with the Transactions.

Separately, the proceeds from these Transactions will not be used to pay any amounts under the $800 million of 7% Senior Notes due 2025.

Please see the full release including relevant disclaimers here.

Shortly following the announcement, ratings agencies Moody's and S&P put Tullow's Caa1 and CCC+ ratings, respectively, on watch positive.

My main take-aways from this proposed transaction are:

Bankers and company have timed this one well - The oil price is supportive, HY credit spreads are tight, and the search for yield remains as as strong as ever. While the previous senior management team appeared to lose the trust of many stakeholders, the new CEO seems to be steering the ship well so far. ESG will be a key area of focus, but in my mind seems to be less of an issue in EM (to date) since so many issuers are from the Oil & Gas sector.

Large deal size - $1.8bn appears to be at the larger end of the typical HY/EM corporate transaction size. This will be a good test of the depth of demand from HY and EM investors.

A lot of the demand may come from existing bondholders - The existing holders of 2021 and 2022 bondholders may switch into the new issue if they believe in the new CEO’s approach and if the pricing is attractive relative to comps and its 2025 bonds

Plenty of comparables - The HY EM oil sector is rich in comparables with Seplat and Kosmos being the most comparable firms due to region / ratings and then some of the oil firms with operations in Kurdistan.

I recall seeing Tullow’s bonds being indicated at a price as low as 11.0 during 2020, and I congratulate anyone that held on since those extremely dark days…Look forward to seeing the terms on this one once they are out.

*LINKS*

April YTD Returns - HY still grinding out positive return…

US inflation expectations

Traders are currently neutral the 10-year but short the 30 year: CFTC Data

Commodities outperforming bonds YTD

Great recap, appreciate also the parts around the trading platforms & fca/mifid developments.

Did you post the right article? 2021? Help I've fallen in time-hole and can't get up and out?