Weekly Global Credit Wrap w/e 28 May

Relief rally and a quieter week generally...

*TLDR SUMMARY*

Risk on rally this week - A number of narratives could be used to explain this week’s rally in rates and credit (more dove-ish Fed later this year (?) / cooling of economy + inflation/bear market rally).

Inflation - More countries doing their best to tackle inflation. UK and its windfall tax on Energy Cos and cash handouts to Energy consumers. India unveiling $26bn inflation fighting plan.

Economies slowing - Hiring freezes and job cuts in growth tech and large cap tech and Amazon signaling plans to sublet warehouse space to reduce excess capacity. Supermarket data in UK shows move towards discounters Aldi and Lidl. More subprime borrowers falling behind on payments on their cars in the US. However, Travel, particularly in the US seems to be an area where there is continued strength for now.

Corporate confidence seems to be rising - judging by the return of M&A deals recently in a range of sectors - Elon/Twitter, Broadcom/VmWare, Etisalat/Vodafone, Aramco/Valvoline, Firstgroup/I Squared to name a few.

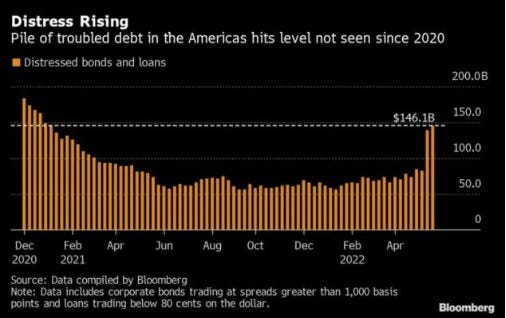

US HY - Saw a decent rally this week as a part of wider risk on, but pile of distressed debt is rising such that its the highest since late 2020...

Financials - Issuance getting completed by largest players, this week saw mainly Insurers. Some interesting tender activity on legacy bonds.

China Property - Greenland surprised the market (negatively) with a debt extension for an upcoming bond which subsequently fell ~60pts. Reuters news story on Evergrande re debt to equity swaps lifted Evergrande bond curve.

EM - Most countries continuing to hike such as Pakistan, however, Russia lowered rates from 14% to 11% this week.

*MACRO

Notable Credit market moves over 5 days (spreads/etfs)

€ 5 yr Itraxx Main CDS - Closed week at +87, retracing from recent highs of ~ +100bps

€ 5 yr Xover CDS - Closed week at +431, retracing from nearly +500bps over

€ 5 year Sub Fins - Closed week at +183 retracing from wides of over +200bps

$ 5 year CDX US HY - Closed week at +457, retracing from wides of over +500bps

Bond ETFs - Longer dated UST rallied (TLT +2.2%). IG Credit ETFs up 2-3% (LQD +2.9%, VCI +2.0%). Higher beta credit ETFs saw bigger moves (PGX Preferreds ETF +6.4%, JNK +4.5%, HYG +4.5%, EMB +2.9%)

Dollar Index has been weakening since the middle of May, more to come?

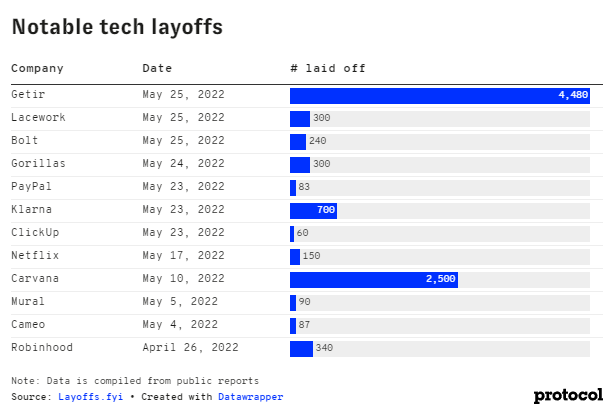

Jobs - A number of high growth tech cos are pausing hiring/cutting jobs

Extract from Protocol:

“Founders and investors are preparing for what looks like an economic downturn — and perhaps even a recession. Last week, Y Combinator sent an email to its portfolio founders warning them to “plan for the worst.” The startup accelerator cautioned that the downturn would likely most affect “international companies, asset heavy companies, low margin companies, hardtech, and other companies with high burn and long time to revenue."

It’s not just early-stage startups that are feeling the burn. Big tech companies including Meta, Salesforce and Netflix have also recently announced hiring freezes or layoffs in the midst of cost-cutting pressure and rising inflation, coupled with a looming bear market and rising interest rates”

UK cost of groceries has sky rocketed at its fastest rate for 13 years - Kantar

Extract: “According to Kantar, grocery price inflation reached 7% over the past month, to the highest level since May 2009. Supermarket sales dropped by 4.4% over the 12 weeks to 15 May, reflecting a a softer fall compared to previous periods, with sales over the last four weeks only down 1.7%. Kantar‘s recent study found that 22% of households are “struggling” to make ends meet, with the rising price of the weekly shop a concern for more than nine in 10 of these people, hence, the rise of customers using discount retailers. Lidl and Aldi were the strongest performing grocers for the period. Lidl sales increased by 6.0% in the 12 weeks to May 15, ahead of Aldi which increased sales by 5.8%.”

More Subprime Borrowers Are Missing Loan Payments - WSJ (19 May)

Extract: “Consumers with low credit scores are falling behind on payments for car loans, personal loans and credit cards, a sign that the healthiest consumer lending environment on record in the U.S. is coming to an end. The share of subprime credit cards and personal loans that are at least 60 days late is rising faster than normal, according to credit-reporting firm Equifax Inc. In March, those delinquencies rose month over month for the eighth time in a row, nearing their prepandemic levels.”

*COMMODITIES*

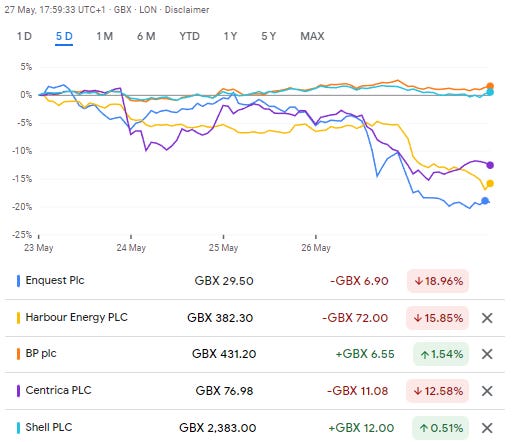

UK - Windfall Tax announcement has varied impact on Oil and Gas Firms

Initial read from market participants is that the windfall tax is a bigger issue for more North Sea focused mid cap Energy producers/firms than the large oil majors (BP/Shell). The list of companies below is not exhaustive, but clearly shows a differentiation in performance over 5 days. The risk is that North Sea firms decide to invest more outside of the UK, more here: Yahoo Finance

Meanwhile, there are murmurs that India is considering a windfall tax too

*NEW ISSUES / TENDERS*

Sidenote re bond tender offers - The reason for highlighting tender activity as well as new issues is to stress the importance of liquidity generated by tenders for holders of corporate bonds. While the market may offer less than desirable bid/offers during illiquid periods, attractively priced tender offers can offer a cost-effective route to liquidity, which can be put to work in a cheapening credit market.

Insurance issuance / redemption activity:

In general, issuers are having to pay more than where their existing bonds are trading in the secondary market, in order to print new bonds.

Axa issued €1.25bn of T2 notes (20.8NC10.8) at MS +260bps

Allianz issued €1.25bn of 30.1NC10.1 T2 @ MS+255

Athora Netherlands tendered for its $575m sub notes and subsequently issued €500mm of T2 10.25NC5.25 sub notes at MS+400.5

AXA (Old XL Insurance) make whole clause sees bonds trade +10pts and AIG cleaned up some of its legacy Sterling bonds. The € XL 3 ¼ 06/29/2047 bonds traded ~10pts to 109 due to a make whole clause (+50bps over reference benchmark).

Nationwide Tender -UK Building society is tendering for two of its USD notes.

Nationwide announces tender offer for certain of its dollar-denominated Notes up to the U.S. dollar equivalent of £700,000,000

Deutsche PBB Decides Not to Pursue Contemplated Tier 2 Offering - BBG

Deutsche PBB decided not to issue its €300m T2 bond offering due to a variety of factors including market conditions. Concurrently the issuer decided not to call its low reset T2 bonds.

AT&T announces expiration and upsizing of tender offers for notes - AT&T

…AT&T is increasing the Maximum Purchase Consideration for the Higher Coupon Offers from $5.0 billion to $5.5 billion and for the Discount Offers from $3.0 billion to $3.2 billion

*FINANCIALS*

Fixed Income/Credit Highlights from JPM Investor day

“Near-term credit outlook especially for the US consumer remains strong. And in fact, we are now projecting that the unusually low level of card charge-offs will persist into next year”

“higher rates are driving deposit margin expansion and NII growth”

“We expect full-year 2022 NII ex-markets to be above $56 billion, which takes into account Fed funds reaching 3% by year-end, in line with the current forward curve; high single-digit loan growth this year…Given these dynamics, we expect the fourth quarter run rate NII to be approximately $66 billion and that run rate serves as a good launch point heading into next year”

“…of the $56 billion 2022 NII outlook that Jeremy shared upfront, $38 billion of that is CCB (Corporate and Client Banking). This represents an increase of $5 billion over 2021 and that will grow to $10 billion when looking at our fourth quarter run rate”

“we (JPM) are the leading market franchise. Undeniable number one in fixed income, tied for one in equities…”

*CHINA*

China Property - The sector continues to trade heavy but with some vaguely positive (but so far unsubstantiated) news from an unusual source -Evergrande. There was less good news from a quasi SOE China property firm - Greenland.

Greenland bonds plunge after Chinese developer seeks extension - Business Standard

Heck of a move in Greenland 6.75% bonds due June 2022 following this news. They were trading at around 90 prior to the news, then dropped to ~30 cents.

Extract of article:

”GREENLAND Holdings, China’s 11th-largest builder, is seeking investor approval for a possible bond-repayment extension, triggering fresh concerns about its financial health.

The Shanghai-based real estate firm has asked holders of a US$488 million dollar note due June 25 to approve certain amendments and waivers that include a maturity extension, according to a filing to the Hong Kong stock exchange Friday. Fears over a possible extension had triggered record drops in the firm’s imminently maturing notes the previous day.

Greenland, which has a presence in 30 countries, is the latest property firm to show signs of rising stress as developers deal with a record wave of defaults. The company was previously seen as relatively immune to the clampdown on China’s debt-saddled real estate sector, in part because it’s viewed as a quasi state-owned enterprise. Builders have been scrambling to extend deadlines or exchange maturing notes to avoid an outright default as key channels of funding remain closed off to many builders.

The 6.75 per cent dollar bond Greenland is looking to extend fell a further 31.5 cents on the dollar to 39.1 cents Friday morning, after tumbling 18.9 cents the previous day, Bloomberg-compiled prices show.”

Evergrande discussing staggered payments, debt-to-equity swaps for $19 bln offshore bonds-sources

Evergrande bonds were up 7-8% on this news story, bearing in mind that the offshore bonds currently trade ~ 10-11 cents in the dollar…so rule of large % moves, small dollar price moves applies…

Extract: “(Reuters) - China Evergrande Group 3333.HK is considering repaying offshore public bondholders owed around $19 billion with cash instalments and equity in two of its Hong Kong-listed units, two sources said, as the world's most indebted developer looks to emerge from its financial woes. Evergrande, whose entire $22.7 billion worth of offshore debt including loans and private bonds is deemed to be in default after missing payment obligations late last year, said in March that it will unveil a preliminary debt restructuring proposal by the end of July. As part of the proposal, Evergrande is looking to repay offshore creditors the principal and interest by turning them into new bonds, which will then be repaid in instalments over a period of seven to 10 years, said one of the sources.”

*IG*

Amazon Plans to Sublet Warehouse Space to Reduce Excess Capacity - WSJ

Extract: “Amazon is attempting to shed some warehouse space following a slowdown the company has experienced in its e-commerce operations. The online retail giant is seeking to sublease a minimum of 10 million square feet of warehouse space and is also exploring options to end or renegotiate leases with outside warehouse owners, according to a person familiar with the matter.”

Southwest, JetBlue give upbeat revenue outlooks despite inflation worries - RTRS

Extracts: “Southwest Airlines Co and JetBlue Airways Corp on Thursday gave upbeat revenue forecasts for the current quarter on strong travel demand, despite concerns that rising inflation may weigh on consumer spending.”

"The improvement in the company's second quarter 2022 operating revenue guidance is primarily attributable to continued passenger yield strength," Southwest said

Southwest said it now expects current-quarter operating revenue to rise 12% to 15% versus pre-pandemic levels. It had earlier forecast an 8% to 12% rise.

JetBlue, which is locked in a takeover battle with Frontier Group Holdings Inc for rival Spirit Airlines Inc, said it expects revenue "at or above high-end of previous guidance" of an 11% to 16% rise.

Both the carriers said they expect a strong summer season.

*HY*

U.S. Bankruptcy Tracker: Distressed Debt Pile Highest Since 2020 - BBG

Extract: “About $7 billion of debt fell to distressed levels last week, pushing the pile of troubled debt to a level not seen since 2020.

The pile of dollar-denominated corporate bonds and loans in the Americas trading at distressed levels rose to $146.1 billion on Friday, about a 5% jump from $139.1 billion a week earlier, according to data compiled by Bloomberg.

Last week’s distressed supply increase was relatively small compared to the nearly 70% jump seen two weeks ago”

Nordic bonds - Pandion Energy successfully places 4 year $75mm bond

Successful issuance for Pandion which was refinancing a NOK bond providing some positive sentiment at a time when issuance conditions in broader HY markets have been tough. Pandion Energy is an independent E&P firm that operates on the Norwegian continental shelf.

Retail Apparel - Number of retailers warn

Gap, Abercrombie & Fitch and American Eagle were just some of the retailers that warned on profits this week. These were some extracts from Abercrombie and Gap:

Gap:

“Gap Inc slashed its annual results forecast on Thursday, sending shares 13% lower after hours as the clothing retailer blamed poor fashion choices at its Old Navy line and weak demand in the face of decades-high inflation”

“[Gap] also posted a much wider-than-expected quarterly loss, slammed by surging costs of air freight and deeper discounts.”

“Gap is also reeling from execution issues at Old Navy, its biggest brand…With shoppers now ditching casuals and athleisure for formals and partywear, product assortment at Old Navy "continues to be out of sync" with the shift in preference, Gap executives said on an earnings call.”

A&F:

“The company reported a decline in gross profit rate to 55.3%, driven by approximately £63 million of higher freight costs, partially offset by higher average unit retail on lower promotions.”

"Looking forward, we expect higher costs to remain a headwind through at least year-end. We expect freight relief in the fourth quarter as we anniversary increased air usage last year due to the Vietnam shutdown.“

“Beginning this quarter, the company will no longer provide a full year outlook on gross profit rate or operating expense.”

*EM*

Pakistan: central bank raised its policy rate by 150bp to 13.75%

This follows some other hikes in EM in the prior week:

Egypt increased the deposit and lending rates by 200 basis points each to 11.25% and 12.25% respectively (higher than market expectations)

Philippine central bank hiked its benchmark for the first time since 2018.

Indonesia Sets Islamic Bond Record with $3.25bn Issuance - Asia Financial

Extracts: The 5-year notes carry a coupon of 4.40%, while the 10-year notes have a 4.70% coupon, below the sovereign’s initial price guidance.

“The issuance … is the biggest global sukuk transaction by the government in history, an accomplishment achieved amid intraday (market) volatility,” the ministry said. Total order books reached $10.8 billion.

The 10Y green bond proceeds will go toward expenditures that have a green or blue focus.

India Unveils $26 Billion Inflation Plan - BBG

Extracts:

“India unveiled inflation-fighting fiscal measures estimated to cost $26 billion that includes lower fuel taxes and import levies… The measures announced…by Narendra Modi’s administration come after inflation climbed to an eight-year high, driven by commodities and supply-chain shocks, and the Reserve Bank of India began raising interest rates for the first time in almost four years.”

Tullow paid $100m of its 2026 notes in May | backs 2022 oil production guidance

On or around 15 May 2022 Tullow paid back $100m of the principal on its $1.8bn 2026 secured notes as per the original amortisation schedule. Amount outstanding now is $1.7bn. In an AGM statement in the week ended 27 May, Tullow said that its oil production guidance for 2022 remains in line with the previous forecast of 59,000-65,000 barrels a day.

*RATINGS*

Egypt's long-term foreign debt rating was affirmed by Moody's at B2 | Outlook to negative from stable

BBVA affirmed at BBB+ by Fitch

Fitch affirms Santander at A-; Outlook Stable

Fitch Affirms Rothesay at IFS 'A+'; Outlook Stable

*CREDIT TRADING*

HF Brevan Howard Gives $1 Billion to Credit Traders in Growth Push - BBG

Vaguely interesting to see Macro shops starting to look at Credit once again. Could we see more asset allocators do the same? Extract of article:

“Brevan Howard Asset Management is expanding its traditional macro business into credit trading. The investment firm has allocated more than $1 billion to a group of credit trading specialists, according to people with knowledge of the matter. The move is seen internally as a new growth area for Brevan Howard, which has until now mainly focused on rates trading,”

*LINKS*

Oaktree’s Howard Marks Latest - Bull market rhymes

Concise summary of why rates fell this week

More dovish market implied longer term inflation expectations

Treasury volatility subsiding for now..

Checking in on yields in different parts of Fixed Income vs 10 year history

US HY - Some short term (?) respite

US HY Refinancing Status

Light Dealer positioning - Illustrates why credit markets see such sharp rallies on the way up as well as big gaps on the way down…

Financial conditions - Tightening since 2021 is fastest since 1990: SSGA