Weekly Global Credit Wrap w/e 26 Feb 2021

*RATES*

End Of week US rates comment - Bond Blogger

I appreciate most people didn’t tune into this substack to hear about rates, but there is no getting away from it this week either….

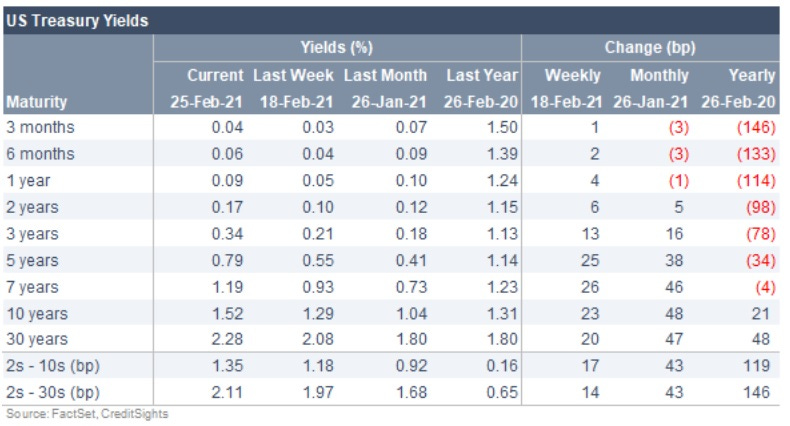

CreditSights produced an interesting table of yields as at 25 Feb 2021 and then looking back over the past year:

A few things stick out to me:

Short term rates (up to around 5 year maturity) remain very low (especially compared to a year ago).

30 year yields are higher than where they were a year ago.

Looking at the 5 year history of 30 year yields, the average yield has been 2.5% and topped out at 3.454% in November 2018 (on a close basis).

One could then say that short term rates need to play catch up (at some point) with the moves out in the long end.

Did we see evidence of that t apathy towards medium term yields this week? There was a strange move during the 7 year UST auction this week when the 10yr yield spiked to 1.61%, up from 1.38% at Wednesday’s close. According to a Barrons article: “the move happened shortly after 1 p.m., when a sale of $62 billion in 7-year notes was met with anemic demand. The Treasury Department reported $2.04 of bids for every dollar sold, the lowest since at least 2009, according to Bloomberg data.”

As markets closed on Friday, long dated Treasuries and credit rallied strongly. Even TLT+ the iShares 20+ year bond ETF posted a 3.3% daily gain on Friday, the first green daily close for the ETF since the 17th of Feb 2021 according to Yahoo Finance feeds. Lets see what next week brings…

There are some top notch links/content on rates which I’ve shared below and also in the links section, please share and like these people’s content.

Were some failed leveraged strategies behind the strange moves in US Treasuries this week?

Chief Fixed Income Strategist @ Janney (@lebas_janney) thinks some of the pain in UST maybe due to some de-grossing in leveraged “butterfly” trades

The US 2/5/10yr butterfly has moved +23bps today which looks like a record 1-day move by more than 10bps. Curve flys are a popular leveraged trade. They don't tend to move that much so can leverage them up pretty big and capitalize on small carry. Today, there was an extreme move that reflects someone (prolly several someone’s) forcibly liquidating that trade into weak bids.

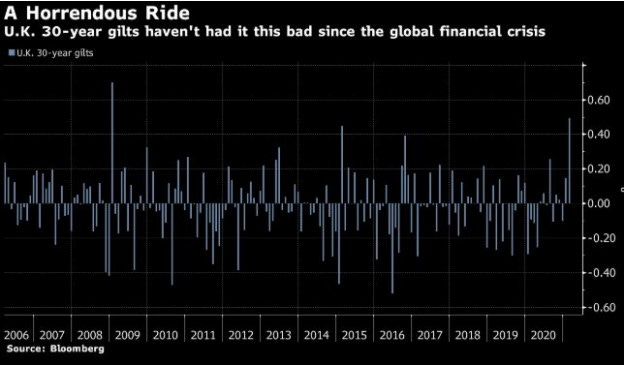

30 Year Gilts yields have not risen this much in a month since the GFC…

The 30-year Gilt has seen its yields climb significantly, surging almost 50bps in Feb (to Thursday 25 Feb). The rate is headed for the biggest increase since the global financial crisis…BBG

*INFLATION*

Costco lifts minimum wage above Amazon or Target to $16 per hour - RTRS

Extract: (Reuters) - Costco is raising the minimum wage for its hourly staff to $16 from next week, a dollar more than what its competitors Amazon and Target pay per hour. The membership-only retailer’s move comes as U.S. President Joe Biden plans to raise the minimum wage to $15 per hour by 2025, and a week after rival Walmart Inc raised its hourly wage to an average of $15. Reuters. Both Costco and Walmart have large workforces, so these moves could have implications for the wider economy.

Writer at PIEE thinks that inflation overshoot maybe temporary

The inflation overshoot, when it comes would likely be temporary citing the period during the Korean War: Inflation fears and the Biden stimulus: Look to the Korean War, not Vietnam:PIIE

10Yr US Inflation adjusted yield rose to highest level since June 2020, but remain deeply negative

30 Year TIPS yields went positive for the first time since June 2020 - Barrons

*CENTRAL BANK COMMENTARY*

US Fed Chairman Powell’s Testimony

- The Fed’s easy-money policies will remain in place until “substantial further progress has been made” toward its employment and inflation goals, Federal Reserve Chairman Jerome Powell told the House Financial Services Committee Wednesday. WSJ

Fed Voter Clarida made hawkish comments on Feb 24th

Fed's Clarida says U.S. economic prospects have brightened (Reuters)

- Despite “very near-term” downside risks to the U.S. economy from the spread of COVID-19 and emergence of new variants, effective vaccines and fiscal relief passed late last year have set the table for stronger growth, Federal Reserve Vice Chair Richard Clarida said on Wednesday.

“Prospects for the economy in 2021 and beyond have brightened and the downside risk to the outlook has diminished,” Clarida said in remarks prepared for delivery to the U.S. Chamber of Commerce.

Clarida said the U.S. central bank’s economic forecasts from December, which call for unemployment to fall below 4% and inflation to return to the Fed’s 2% target by the end of 2023, would represent a faster rebound than occurred after the financial crisis more than a decade ago. Kitco news (Reuters)

*ISSUANCE*

EasyJet raises 1.2 bln euros from bond deal (books nearly 6x covered)

Extract: “(Reuters) - EasyJet raised 1.2 billion euros from a seven-year bond sale on Wednesday. The deal attracted investor demand of 5.8 billion euros, a lead manager announcement seen by Reuters said, helping the company to reduce the yield on offer to 2%, from around 2.375% when the sale first started on Wednesday. The deal came at the top end of a 1.0 billion-1.2 billion euro target range. The positive response from bond investors comes after British Prime Minister Boris Johnson set out a phased plan on Monday to end England’s COVID-19 lockdown. Under the plan, Britain could see curbs on international travel removed as early as May 17.”

Saudi Arabia Borrows at Negative Rates for First Time as Oil Recovers | WSJ

Extract: “The kingdom raised €1.5 billion, equivalent to $1.8 billion, through a bond sale on Wednesday. The yields were minus 0.057% for three-year debt and 0.646% for nine-year, the cheapest borrowing costs it has achieved to date. It was the second time it has issued bonds in euros.” WSJ

Volatility in rates market didn’t stop Aston Martin raising money last week

A subsidiary of Aston Martin, successfully priced $98.5m of 10.5% Senior Secured Notes due 2025 (the "Notes") at a price of 109%, a premium which generated gross proceeds to the Issuer of $107.4 million (£76m equivalent). Link to company statement

Indian Miner, Vedanta came back to the new issue market to raise $1.2bn this week

Extract: “Vedanta Resources Finance II Plc, a subsidiary of London-based Vedanta Resources, had gone to the market for raising $1 billion. It got $2.6 billion in offers from about 150 accounts, representing the largest oversubscription on a recent US dollar bond offering by the company, banking sources said.” Live Mint

*INVESTMENT GRADE*

Impact on Duration Moves on Credit - Bond Blogger Comment

According the BBG, on Feb 26 2021, the U.S. high-grade bond index fell by the most since September 4 2020 , dropping 0.97% to hit the lowest since July 1 . The month to date total return through Thursday is negative 2.88%, the biggest loss since March 2020.

Some of the trends playing out that I have seen are:

Financials - Weakness in both long dated bullet bonds and callable bonds with long calls (7+ years). A good example of this is are a handful of 20 year Tier 2 USD bank bonds that were issued this year with sub 3% coupons that are trading in the mid to low 90s.

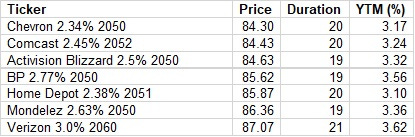

Corporate - More low coupon bonds trading at cash prices of 80 and 90 due to the high sensitivity to higher rates. I picked out some of the lowest priced (cash price) bonds in the LQD index to highlight the price impact of the steepening of rates:

With the duration on these bonds around the 20 mark, it becomes clear quite quickly how the losses can accumulate in a steepening yield environment. Of course if one is a buy-and-hold investor like a US pension fund or a new investor at these discounted levels, then the recent price action is less of a concern.

As many market commentators have remarked, credit spreads on IG have narrowed significantly, so it will be interesting to see where those go next. Of course several factors can contribute to the direction of broad credit spreads, e.g. level of central bank accommodation, credit market liquidity, unexpected events (e.g. the pandemic!).

Telefonica cut its dividend, was largely expected- Reuters

Extract from Reuters: “Telefonica has cut its dividend after reporting a 10% fall in 2020 earnings even though the Spanish telecoms group expects its business to stabilise this year.

Telefonica, like European rivals, was already facing growth issues before the pandemic struck, and is focusing on expanding in Brazil, Britain, Spain and Germany and selling assets to cut debt and fund an upgrade to next-generation 5G networks. It has cashed in on investor appetite for infrastructure, selling more than 30,000 mobile masts and a stake in its Chilean fibre optic network to help shrink its debt. Telefonica UK’s business O2 is planning to merge with Virgin Media. Investors welcomed the cut in the dividend to 0.30 euros per share on 2021 earnings from 0.40 in 2020 as a way to lighten a debt load which has weighed on Telefonica’s shares. Reuters

Verizon pledges whopping $45B in C-band auction: Fierce Wireless

Extract: “Verizon was always expected to “go big” in the auction because it needs mid-band spectrum more so than the other carriers. A lot of folks were betting that Verizon went big in the C-band auction, but it turns out it went even bigger than some of the highest expectations, laying out over $45.5 billion in gross bids. The FCC closed the assignment phase of the auction last week, with total winning bids reaching over $81.2 billion. The agency announced the names of the winning bidders Wednesday and said 21 bidders won all of the available 5,684 licenses. Verizon’s total tally was $45,454,843,197. In second place was AT&T, which spent more than $23.4 billion, followed by T-Mobile, which bid over $9.3 billion. The bid amounts drop significantly after that, with United States Cellular pledging over $1.28 billion. NewLevel II, a private equity firm specializing in broadband, bid more than $1.27 billion.”

The news flow re the C-band auction is important since the issuers mentioned (Verizon, AT&T, T-Mobile) are all big issuers in the US Credit market.

*HY / Distressed*

HY Credit Trading Observations - Bond Blogger Comment

Bonds with short durations, high coupons (typically lowly rated) were in demand this week as a shelter from falling bond prices in the longer duration portion of the credit market. This was evident in contrasting performance of different ratings tiers within US HY. BB yields are 15bps wider (cheaper) on the month, whereas B and CCC yields have tightened (rallied) in 2bps and 84bps respectively according to FTSE HY indices. This is not entirely illogical since many of the worst hit COVID19 impacted sectors like airlines, cinemas, restaurants and energy currently sit in those lowest rated tiers, and market participants are looking to benefit from spread tightening via the “re-opening” trade.

Shale companies re-emerge in publicly equity markets, generating large gains since trading - WSJ Article

Extract: “Former drilling giants are testing their footing in the public markets after a near record number of reorganizations in 2020. It was the second-largest year for oil-and-gas producer bankruptcies—measured by debt volume—since the law firm Haynes and Boone started tracking the numbers in 2015.

Chesapeake Energy, once the second-largest natural-gas producer in the U.S., started trading on the Nasdaq last week as a shell of its former self: Its market capitalization is roughly $4 billion, a little over a tenth of what it was at its peak. Whiting Petroleum WLL 5.13% and Oasis Petroleum emerged from bankruptcy in late 2020, also at fractions of their heyday valuations. Their shares are up 59% and 65%, respectively, since they started trading after emerging from bankruptcy.” WSJ"

Rising stars are projected to outweigh fallen angels…JPM Strategists

Extract: “The investment-grade bond market could see some new entrants—or returning names—in the next two years, as corporate credit ratings get upgraded. But the net downgrades aren’t over yet, according to J.P. Morgan Chase strategists.

The next two years could bring $284 billion of “rising stars,” or companies with ratings that get upgraded to investment-grade levels from junk, according to a Feb. 24 note from the bank’s credit strategists.” Barrons

Puerto Rico Rides Muni-Bond Rally to Bankruptcy Deal | WSJ

Extract: “Puerto Rico moved closer to resolving the largest municipal-debt default in U.S. history as creditors owed $11.7 billion coalesced around a settlement, the most Wall Street support yet amassed for a restructuring of the territory’s core public debts.

Creditors agreed to cut $18.8 billion in general obligation debt by around three-fifths to $7.4 billion, wagering that booming market demand for risky municipal debt will help generate profits for them while easing Puerto Rico’s exit from bankruptcy. “

*GREEN BONDS*

Ardagh Metals - Largest ever HY green bond and SPAC deal: RTRS

Ardagh Metal Packaging sold $2.8 billion worth of green bonds on Friday, the biggest green issuance in the high-yield market to date, as a part of its plan to merge with a blank-check firm backed by billionaire Alec Gores. Sub-investment-grade firms rarely issue green bonds, which fund environmentally-friendly projects. Just $12 billion was raised by such companies last year, according to Dealogic, a far cry from 2020’s overall green issuance of $270 billion, according to Climate Bonds Initiative.

The issue from Ardagh Metal Packaging, which is being spun off from Luxembourg-based global packaging group Ardagh Group, is triple the size of French recycling services group Paprec’s 2018 deal, the previous largest.

*EMERGING MARKETS*

Impact of duration on Emerging Markets Bonds

Many EM USD denominated bonds have been impacted by the duration sell-off. EM Sovereigns have been impacted more than EM corporates due to the higher duration of the former. Looking at the duration of popular EM Bond ETFs; EMB (8.5) and CEMB (5.1) its clear why the total return is so different YTD (-4.77% vs -0.77% respectively). Several investment grade sovereigns in particular issue very long term debt, e.g. likes of Panama and Mexico in LATAM, MENA issuers like Saudi Arabia, Abu Dhabi and Asian issuers such as Philippines, Indonesia.

Turkish Banks Race to Pay Out Dividend After Two-Year Ban Lifted - BBG

(Bloomberg) -- Turkish lenders proposed resuming cash dividends after the banking regulator removed a two-year ban on payouts.

Private lenders Akbank TAS, Yapi ve Kredi Bankasi AS and Turkiye Sinai Kalkinma Bankasi AS announced their plans in public filings to Borsa Istanbul. The banking regulator, known as BDDK, permitted banks last month to pay as much as 10% of last year’s net income as dividends. bbg

*RATINGS*

S&P Global Ratings raises New Zealand's credit rating to AA+ RNZ

Turkey – Rating set to stable, BB- by Fitch

Ecuador Outlook to Stable by Moody's

Belize’s Bonds Fall to Eight-Month Low as S&P Warns of Default

S&P PUTS VARIOUS TEXAS UTIL RTGS ON WATCH NEG AFTER STORM

Moody's upgrades Best Buy to A3

Teva Affirmed at BB- by Fitch

Barclays Outlook to Stable by S&P; L-T Rating Affirmed

Nordea's L-T Rated AA- by S&P, Outlook Stable

ABN AMRO Outlook to Stable by S&P

S&P hikes Deutsche Bank credit rating outlook to positive from negative

Commerzbank Affirmed at BBB+ by S&P

S&P: ROYAL CARIBBEAN CRUISES TO B/NEGATIVE FROM B+/WATCH NEG -

S&P: NOKIA TO BB+/STABLE FROM BB+/NEGATIVE

S&P Raises American Axle & Manufacturing Inc. Rtg To BB- From B+; Outlk Stable

*LINKS / TWEETS / PODCASTS*

Blog post on how stock market performs when interest rates rise (good read): awealthofcommonsense.com

Oaktree’s Howard Marks latest Podcast (24 Feb) - “You can’t predict, you can prepare.” Oaktree Capital

ECB Schnabel says that the secular decline in real interest rates requires us to rethink the optimal policy mix during economic downturns: ECB

Impressive tweet from the always impressive Charlie Bilello re US Bond Market Returns:

Great chart from Arbor Research about historic returns of the 30 year US Bond

GS Chart on Eurostoxx 600 sensitivity to changes in bond yields

10y yield back above S&P dividend yield: Liz Ann Sonders (Schwab)

60/40 portfolios tend to suffer when during periods of high and rising inflation: GS/Isabelnet

One for the LQD watchers. Who is right here, shorts or longs?

Disclaimer: This is not investment advice and these comments reflect the opinions of the author and not his/her employer. I may own positions in some of the securities mentioned in this substack.