Weekly Global Credit Wrap w/e 24 June 2022

Slightly better market tone in places...but its complicated.

*MARKET TONE*

Market tone improved slightly this week due to the relief rally in rates.

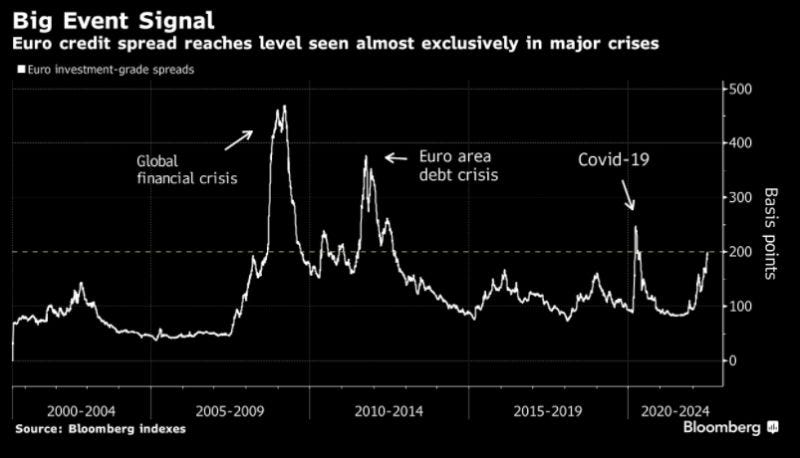

IG - Bit of a relief in USD IG this week but spreads in EUR IG have hit 200bps, which is the level last seen during the early stages of the pandemic. Despite the wider spreads, EUR IG market printed more than €34bn of issuance in the week, which was more than expectations.

Sub Financials - AT1 market is showing signs of thawing led by primary, with CS last week and this week Barclays issuing good size in £ at a wide coupon. However, secondary market activity seems subdued, likely linked to continued QT backdrop and difficult fund flows momentum.

HY - Despite the rally in stocks and rates, HY appears to be lagging as demonstrated by the CCC bond yields which hit 13% during the week. In the US leveraged finance market BBG reports that a number of LBO loans are sitting on bank balance sheets which are being marked down due to mark to market volatility. In order to get these loans off their books, Banks in some cases have had to sell at record discounts. On the other side of the trade, CLOs appear to be buying more HY bonds than before, tempted by the higher yields and greater price discounts. In Europe/UK a number of idiosyncratic blow ups has resulted in immense price volatility, this week’s examples include SBBBSS and Peach Property. UK £ HY yields have gone through 8.6% this week…with many issuers in that space affected by higher inflation (e.g. grocery stores like Co-Op Group/Iceland).

EM - Strength in middle East high grade this week as UAE (AA-) printed a dual tranche deal, MAF printed a hybrid and Oman came out with a tender for $1.75bn of securities. Asia EM posted yet another poor week of performance but this time not just due to China Property bonds, but they were joined by the likes of Vedanta and Fosun.

*MOVES THIS WEEK*

Credit spreads - CDX NA HY was nearly 50bps tighter on the week to close at +529bps and European 5 year Xover was 30bps tighter. IG and Financial CDS indices did not see as big moves. In cash credit spreads, none of the indices I tracked tightened, with EUR HY widening 36bps.

Rates Bond ETFs - With the rally in rates, a number of rates bond ETFs rallied led by the IGLT ETF which added 1.6 percentage points over 5 days. TLT was up 80bps but is still down 23.5% YTD.

Credit Bond ETFs - Best returns over 5 days came from CWB (+4.76%), JNK & HYG both up +1.7%, EMB +1.2%, IEAC +1.1%, VCIT +0.9%. Focusing on the YTD returns, its still interesting to see the contrast in performance between LQD (-16%) and HYG (-12.1%) and between EMB (-19.2%) and CEMB (-13.78%). The difference between LQD and HYG being the greater impact of rates on longer duration credit and the difference between EMB and CEMB likely explained by the exposure to Russia/Ukraine and a number of EM Sovereigns that have been under the kosh due to unsustainable debt/record inflation (e.g Sri Lanka and Pakistan).

*MACRO CREDIT*

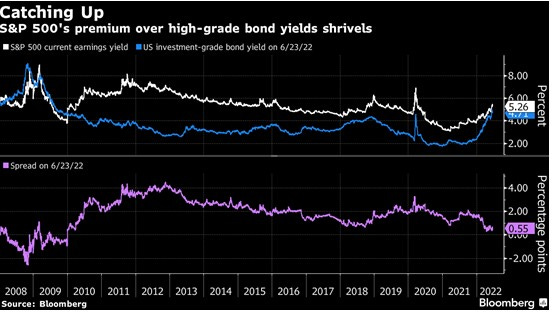

S&P 500’s premium over IG bond yield narrows

S&P 500’s earnings yield is around 5.3% at the moment, just 55 basis points above the average US investment-grade yield of 4.7%. That close to the narrowest gap since 2010. H/T @kgreifeldin her Weekly Fix Email..a good one!

Another surprise hike in Europe, this time from Norges Bank

Norges Bank unanimously decided to raise policy rates by 50bp, which was unexpected, taking the sight deposit rate to 1.25%. This move didn’t seem to cause as much of a stir as when the Swiss National Bank surprised the market and hiked more than expected last week.

UK - Politics/Eco roundup

Interesting week as Conservatives lost parliamentary seats in two by-elections to Labour and Lib Dem parties respectively.

On the economic front, UK consumer confidence dropped to a record low meaning sentiment is worse than it was during the height of the pandemic and the financial crisis.

The situation stems from record inflation (energy costs, rent, food). This is also what is driving the many ongoing negotiations between workforces/unions and companies/government agencies. Some of the active negotiations ongoing are: BT, Rolls Royce, the UK Rail network, Airline and Airport staff.

US Housing - Main takeaways from Lennar/KB Home

The slowdown in the US Housing Market already appears to have started, based on the earnings calls for US Homebuilders KBH and Lennar this week. The demand for property appears to vary across different states and cities mainly depending on how much the prices of the respective areas went up in the past few years. Some of the cities that went up the most like Austin and Los Angeles are seeing the greatest slowdowns. It is also apparent that the Homebuilders are not looking to buy up land at current levels and instead work through their existing land and inventory.

Lennar Earnings call transcript

Nevertheless, the rapid increase in interest rates, together with price appreciation have created at least sticker shock and perhaps a more structural cooling of demand.

So far in June, new orders, traffic, sales incentives and cancellations have worsened in many of our markets due to a rapid spike in mortgage rates and headwinds from negative economic headlines. Many markets have also slowed as we've entered a seasonably slower part of the year.

I'd now like to give you some color on our markets across the country. They really fall into three categories: one, markets reflecting no and minimal impacts; two, markets reflecting modest impacts; and three, markets reflecting more significant impacts…[mgmt go through the first two types of market, then the third as described below].

Our category 3 markets, which reflect the more significant market softening and correction includes seven markets. These include Raleigh, Minnesota, Austin, Los Angeles, the Central Valley, Sacramento and Seattle.

Higher rates in June and headlines on stock market declines and the distressed national economy has sidelined many buyers who are waiting for a reset in home value

Austin has been the most impacted market in Texas, following back-to-back years of 40% plus appreciation and bidding wars on available inventory.

While inventory is limited, cancellation rates have increased and we've reduced prices in many communities on a home-by-home basis and have offered extremely competitive mortgage programs

Our communities in Los Angeles, Central Valley and Sacramento have experienced a significant slowdown with traffic dropping off considerably in late May and into June. With the spike in interest rates, buyers in these markets have been extremely credit challenged and cancellation rates have increased with adjusted prices are using financing incentives

Seattle was one of the strongest markets in the country over the last two years. The market saw strong integration, solid job growth and sales prices that grew approximately 20% annually in each of the last few years. While market fundamentals with limited land supply and low inventory remains extremely strong, buyers have pushed back for a reset in pricing.

The higher priced and highly sought after locations around Seattle have seen a significant pullback in sales in May and early June. This pullback is a result of both continued price appreciation in the first quarter, causing concern over home values being overpriced and stock market corrections, which have had a direct impact on employee stock compensation plans. We've adjusted prices in some communities to Q4 pricing and has seen a sales uptick with this correction, which demonstrates the underlying strength of the market. Once again, in this market, we are at prices that are still significantly higher than the year-ago period.

KB Home Earnings call transcript

Order rates are moderating from the exceptional levels that the industry experienced beginning in late 2020, as higher interest rates and increased home prices along with other inflationary pressures are impacting current demand.

Our net orders were 3,914, down 9% versus a year ago when we reported the highest second quarter net orders in the prior 14 years. While our gross orders were flat year over year, a higher cancellation rate created the negative net order comparison as some buyers were affected by the larger monthly payments from the increase in mortgage rates.

Our business model allows us to move with demand and responding to what buyers want and need. And this strength is reflected in our first time and first move-up buyer percentages, the largest demand segments, holding steady sequentially in the second quarter at 56% for first time buyers, and 78% for the two combined.

So I actually believe right now we're in a digestion period, similar to what happened in 2018 when prices ran and interest rates peaked. And they're just -- they're trying to figure it out, there is buyer we're dealing with today can afford these homes at today's rates. It's whether they're comfortable with everything else that they're trying to absorb on inflation and gas prices in Ukraine and maybe their job situation, I don't know.

Loan-to-value ratios held steady at 85% translating to an average cash down payment of roughly $75,000 and close to 100% of buyers use fixed-rate products. The average household income of these buyers was about 125,000 and their FICO score showed a slight sequential improvement to 734.

We already own and control everything we need for a nice growth rate in '23 and '24. So we're set for '23 and '24 and as we look at things, it doesn't make sense to drive more investment to try to grow even more until there is more clarity and where demand is going to end up and where land sellers end up in there.

Until there is real clarity in this market, is it a brief digestion or is it a structural shift in either case, what does it mean? We're going to take our time because we have the ability to do so right now. And we'll be pulling back on our land spend coming out of this year until we have clarity. And what that means is, you're set up to grow your company, you spend less on land, we should over time be in a nice position to have flexibility in how to reallocate the capital.

…We've gone through this latest cycle and there is still very, very thin layer of inventory that we have in our system out there

CATL Unveils EV Battery With One-Charge Range of 1,000 Kms: Clean Technica

CATL says its new Qirin battery has 13% more energy density than Tesla’s 4680 cells and can go 1000 km without recharging. This technology couldn’t come sooner with all the issues people are having with high gas costs.

*INFLATION*

Singapore's $1.5 bn inflation support package to help workers, households - BBG

Extract: “The Singapore government announced a S$1.5 billion support package to help businesses and residents cope with inflation amid rising prices. Deputy Prime Minister and Minister of Finance Lawrence Wong announced the measures during a press conference, noting that the Ukraine war had put “ tremendous stresses on global supply chains” and that protectionist measures by countries had “compounded supply chain disruptions”. “Global energy and food prices have risen sharply and we must expect global inflation to broaden to other areas and even to pick up further before it stabilises and gets better,” he added. While Singapore is in a “stronger position” to deal with these issues as compared to other countries, the city state has not been spared from the effects of higher prices.”

Singapore is often seen as a forward looking nation, which suggests to me other countries could likely follow a similar playbook. Early examples are the UK’s support for consumers who are being offered rebates on their Energy Bills to reduce their cost of living.

Freight rates between Asia to the US West Coast have halved vs average for year

Extract from Tradewinds: Freight rates from Asia to the US west coast slumped to $8,934 per 40-foot equivalent unit (feu) on 21 June, according to the Freightos Baltic Index. Some carriers are reportedly offering rates below $7,000 per feu, which is less than half the average of about $15,000 per feu for most of the year.

Asda Supermarket (UK) says some shoppers asking cashiers to stop at £30 - BBC

Extract: Some Asda shoppers are asking cashiers to stop scanning items when the till total hits £30 as they try to cut costs, the supermarket's chairman says. As well as putting less in their baskets, Lord Rose said more customers were switching to budget ranges with people worried about rising prices. "What we're seeing is a massive change in behaviour," he told the BBC.

United Airlines pilots to get raises of more than 14%, 8 weeks of maternity leave in new contract - CNBC

“The union representing United Airlines pilots has approved a tentative deal that would give the aviators pay raises of more than 14%, making it the first major U.S. carrier to reach a deal since the start of the Covid-19 pandemic and setting the bar for the rest of the industry.

The agreement comes as the airline and others grapple with a shortage of pilots, which some carriers say have forced them to trim flight schedules. The contract faces a vote by rank-and-file pilots that will conclude in mid-July. Under the agreement approved Friday, pilots would get more than 14.5% in pay increases within 18 months, according to the Air Line Pilots Association, which represents about 14,000 United pilots. Pilot pay at United as of 2020 ranged from about $73,000 a year for an early-career first officer on the carrier’s smallest aircraft to more than $337,000 for a wide-body captain, according to Kit Darby, a pilot pay consultant and retired United captain.” Source: CNBC

*RUSSIA/UKRAINE*

Are we nearing an end to the worst of the Ukraine/Russia conflict?

I’m sure I speak for many when I say that I would like to see this conflict end, to put an end to the unnecessary death and destruction that is taking place.

Reports on Friday stated that Ukraine had ordered its troops to withdraw from their remaining foothold in the city of Severodonetsk, ending a battle which lasted nearly two months. Various commentators referred to the win as “symbolic” rather than strategic. BBG opinion John Authers mentioned in a piece this week that soon enough, the news about the Russian/Ukraine conflict might be faded from the main western news headlines as it becomes yet another ongoing conflict going on globally.

This fading war narrative could also be a driver behind the fade in commodities sector (e.g Metals) as some market participants associate this with greater future availability of commodities.

Ukrainian Railways’ Liquidity Adequate For Coupon on July 2022 LPNs - Fitch

Extract: “There is a low risk of default on JSC Ukrainian Railways’ loan participation notes’ (LPN) upcoming July-coupon payments Fitch Ratings says. We assess Ukrainian Railways’ liquidity as adequate to meet the upcoming coupon payments, assuming that the adverse impact on the issuer from the ongoing Russian-Ukrainian war does not significantly worsen before the coupon payments’ due date. The Ukrainian government - the company’s sole owner – declared its intention to remain current on financial obligations, despite the ongoing war.”

Sidenote: Earlier in June, the EBRD stated it has repurposed part of an existing loan to provide €50 million of liquidity to Ukraine Rail.

*IG*

European Credit - IG issuers funding costs nearly double (BBG)

BBG cited the example of Chemicals company BASF which paid 140bps over midswaps this weeks to issue new 10 year bonds which is almost double what it paid to sell 9 year debt a bit over 3 months ago. EUR IG spreads are now at +200bps, a level last seen during the early stages of the pandemic.

Volkswagen International raised € 1.5bn via a green dual-tranche

It raised € 705m via a 2.75Y bond at a yield of 3.152% and € 750m via a 5.25% bond at a yield of 3.85%. The senior unsecured bonds are rated A3/BBB+ and received orders over € 5.4bn, 3.6x issue size. Net proceeds will be used to finance and/or refinance green eligible projects. A yield above 3% for a short dated senior IG corp in Euros was unthinkable less than a year ago…

Euro Credit - Number of Idiosyncratic situations increasing

This week saw large price falls for SAMHALLSBYGGNADSBOLAGET (SBBBSS) and PEACH PROPERTY. SBBBSS bonds, some of which have dropped ~20pts have been the target of another report from Viceroy Research. Peach Property is another one (not IG but BB rated) where bond prices have fallen around 9-10 points. With many credit investors sitting on large losses YTD, there is increasing loss aversion which is likely leading to the “sell first, ask questions later” mantra on any issuers associated with bad headlines.

Some leveraged Muni Funds facing double digit losses - WSJ

Extract from WSJ: “Closed-end funds typically employ leverage, borrowing an amount equivalent to about one-third of their value and investing it…In the first five months of 2022, closed-end muni funds returned minus 15.9%, counting share price changes and assuming distributions are reinvested, according to Morningstar Direct. That compares with a total return of minus 7.47% for the Bloomberg muni bond index.”

This is not hugely surprising considering the damage that rising rates have done to other parts of Fixed Income, but highlights how traditionally “safe” areas and structures in the bond market have not been sheltered from the pain.

*HY*

New York Fed to Launch Regular Publication of New Corporate Bond Market Functioning Measure

Taken from the NY Fed: “ On Wednesday, June 29 at 10:00 am EDT, the Federal Reserve Bank of New York will begin monthly publication of a new research product focused on identifying periods of widespread distress in the U.S. corporate bond market. The Corporate Bond Market Distress Index (CMDI) is a unified measure that uses weekly metrics to construct an aggregate index of corporate bond market conditions for both the primary and the secondary markets. The CMDI incorporates a wide range of indicators, including measures of primary market issuance and pricing, secondary market pricing and liquidity conditions, and the relative pricing between traded and nontraded bonds.”

Full statement.

Eurofins refinanced a pair of hybrids with senior debt…

Interesting discussion topic on whether a corporate can use senior bond issuance to refinance a hybrid and still keep the equity content of other hybrids outstanding. Something to watch especially as Corporate Hybrid maturity schedule gathers speed in 2023.

Direct lending / LBOs - Impact on Banks

BBG reporting that some direct lenders in Europe are obtaining better investor protections in order to get deals done, while the public markets are effectively still frozen. The linked article cites the addition of a net leverage covenant in GE PE arm’s takeover of Pharmaceutical: Norgine BV.

The reason why Direct Lenders can call the shots at the moment is because some banks are licking their wounds from the re-pricing of buyout debt which is sitting on their balance sheets. This BBG article cites the example of Citrix systems which a group of Banks lent to, and still hold the loans on their balance sheets resulting in losses in excess of $100m. According to BBG:

“Underwriters on both sides of the Atlantic are now sitting on an estimated $80 billion of commitments backing leveraged buyouts that will be difficult to sell in a market for junk debt that is effectively frozen. While that’s a modest undertaking compared to the more than $200 billion stockpile heading into the 2008 crisis, the worry is that writedowns will grow as rates rise, acting as a drag on earnings.”

The only way banks have been able to sell these loans have been at a large discount to par. Deutsche Bank sold HY bonds backing the buyout of packaging firm Intertape Polymer Group Inc. at just 82 cents on the dollar and CS sold loans of Manuchar NV at the largest discount in a decade for the European market: 86 cents on the euro.

All this will have knock on effects for the pricing of debt in similar markets - HY bonds, lev loans etc.

US CLOs Are Piling Into Cheap Junk Bonds - BBG

According to a recent report from Bancorp (via BBG), CLOs have been adding HY bonds. ~34% of CLOs owned at least one corporate bond in May, up from less than 20% at end of 2021. “It’s affording a discount opportunity for CLOs that they haven’t had in many years,” said Phil Raciti, head of U.S. performing credit at Bardin Hill

Source: BBG, extracts only

*FINANCIALS*

Barclays AT1 followed Credit Suisse in issuing a very high coupon AT1

Barclays issued £1.25bn AT1 with an 8.875% coupon in GBP. The issue appeared to be well received with book coverage said to be ~3.4x. The pricing was tightened from the initial pricing talk of 9.25% area. The size printed is impressive considering how tricky market conditions are right now. As we close the week the bond is trading 1 point higher. As a side note, the CS 9.75% AT1 issued the week before is trading at a 3 point premium currently. It looks like the pricing in the primary is driving some more engagement in the secondary market, but its hard to establish if this is a trend or just a relief rally as levels of volatility and illiquidity remain high.

I believe we are in the early stages of creating a quality vintage for this asset class, which is interesting especially as there are discussions from some ratings agencies/regulators to remove the AT1 asset class altogether!

Marex Group issues At1 at 13.25% coupon

Commodities broking firm Marex issued a 13.25% coupon AT1 in $100m size. Again my take away here is that some issuers are managing to get issuance done, but at a very high cost of funding.

US Bank stress tests

The Fed said all banks passed the stress test and that 34 large US banks have strong capital levels and could continue lending in an economic downturn.

*EM*

Overview - More robust Middle East nations flexed their muscles this week in the debt market, namely; Oman which tendered for existing bonds and UAE which came to market with a dual tranche long dated set of bond issues.

Oman offering to buy up to $1.75bln of outstanding bonds - Zaywa

The note series being tendered are $1.25 billion notes due in 2025, $2.5 billion bonds maturing in 2026, $2 billion paper due in 2027, $1.45 billion also due in 2027, $2.5 billion due in 2028, $2.25 billion maturing in 2029, $1.75 billion due in 2031 and $1.05 billion notes due in 2032.

The UAE dual-tranche USD bond issuance achieves an oversubscription by 5x - Zaywa

The 10-year tranche bonds size was USD 1.75 billion, priced at a spread of 100 bps over US Treasuries, with final coupon at 4.050%.

The 30-year Formosa tranche size was USD 1.25 billion, priced at a spread of 175bps over US Treasuries, with final coupon at 4.951%.

The transaction looked to be a successful one since it was upsized and priced at the tighter end of the new issue concession. The highly rated sovereign (AA-) would have attracted interest from those looking for a flight to quality and the potential halo-effect of further tightening of Treasury yields.

MAF Global priced $500m PNC5.25 Green Hybrid @ 7.95%

Dubai's Majid Al Futtaim (MAF), which develops shopping malls across the Middle East, on Thursday sold $500 million in perpetual green hybrid bonds non-callable for 5-1/4 years at 7.95%, a bank document showed, source: Zaywa/BBG.

Books were said to be 2x covered for this deal which is set to pre-finance its existing hybrids which are callable in September this year. This is some achievement considering how tough the market conditions are for European Corporates to issue hybrids. This transaction is a testament to how well Dubai and UAE has fared during a testing time for many other nations around the world. Furthermore, the ECB stepping away from investing directly in the Euro Senior IG market is clearly having an impact on the European Corporate Hybrid sector at the moment.

Gulf Keystone Petroleum redeeming $100m bond early (July 2022)

Kurdish oil company Gulf Keystone has announced an intention to call its $100m bond at 102.0 in July 2022 instead of letting it mature in 2023. This would make the company debt free. As at 23rd June 2022, the firm had $247mm in cash. Gulf Keystone does not currently have a hedging programme, so appears to be reaping the full benefit of elevated oil prices.

Egypt - Central Bank keep all policy rates on hold

Egypt's central bank kept its overnight interest rates unchanged on Thursday, saying that for the next six months it would tolerate elevated inflation, caused mainly by the Ukrainian conflict, as the economy grows more slowly than expected.

The expectation from forecasters had been for a hike to the deposit rate of 50bps and the lending rate by 25bps.

"In accommodation of the first-round effects of supply shocks, the elevated annual headline inflation rate will be temporarily tolerated relative to the CBE's pre-announced target of 7 percent (±2 percentage points) on average in 2022 Q4, before declining thereafter," the committee statement said. Source: Zaywa

To me the “temporarily tolerated” sounds a bit like the “transitory inflation” chatter we got from the Fed last year..

Mexico - Banxico hiked its benchmark by 75 bps, as expected

It was the largest increase since 2008, and predicted inflation will pick up to 8.1% in the third quarter.

*CHINA*

China Property Sector sees sales increase

Nomura said property sales across 30 cities recovered quickly last week, with four top tier cities recording 20%-30% volumes higher than a year ago, and second-tier cities 30% on average. Source: Reuters

*CREDIT TRADING*

Top three venues in Fixed Income look to increase transparency in European bond market via consolidated Tape

Extract from Waters Technology : “The top three venues in fixed income by trade volume—MarketAxess, Tradeweb, and Bloomberg—have confirmed their plans to compete for the contract to deliver the regulator-backed consolidated tape (CT) for bonds in the EU. WatersTechnology first broke the news of this partnership back in November 2021.”

My understanding is that this is akin to the US FINRA Corporate bond TRACE system which prints trade information either immediately or with a delay depending on the size of the trade taking place. End result should be more price transparency for participants in the European Credit Market.

*RATINGS*

Moody's upgrades JSC Georgia Capital's CFR to B1, stable outlook

Fitch Upgrades Fidelity Bank to 'B' From 'B-'; Outlook Stable

Moody's has downgraded Coinbase Global, Inc.'s (Coinbase) Corporate Family Rating to Ba3 from Ba2, the ratings were placed under review for further downgrade.

Ocado: Fitch lowers the outlook on the B+ rating from stable to negative

Hapag-Lloyd Outlook to Positive by Moody's

Croatia May Be Raised to Investment Grade by Moody’s

*LINKS*

Great to see concept of price discovery return to the credit markets!

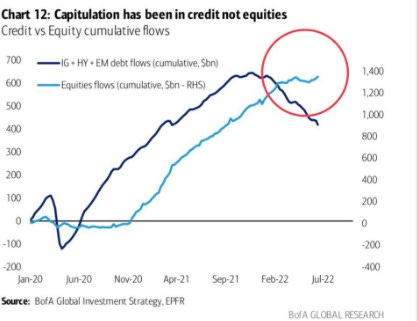

Bonds v Equities Flows - via Bofa

IG outflows..when will they end??

One chart that explains the sheer number of bonds trading below par

Who would have thought the 2 year Treasury would be so interesting?

Bull case for HY? But $330bn in these market conditions is still a large number!