Weekly Global Credit Wrap w/e 23 April 2021

Peru has a 100 year bond...

*OVERVIEW*

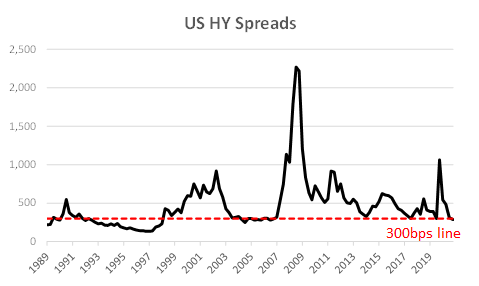

US HY spreads are hovering under 300bps. There have been previous instances such as between 1993 and 1998 when spreads stayed low for long periods. However, bear in mind that all in yields would have been much higher due to higher treasury yields on offer at the time (5yr bonds ranging between 4% to 8%!).

While broad spread levels are tight across a number of markets, there have been a number of idiosyncratic situations, especially in EM. None of these have been COVID19 related (Peru election, Huarong in China, Alpha Credit in Mexico).

Most of the market’s macro focus is on when the Fed will taper bond purchases / hike rates. There was some mild excitement on that front as the Bank of Canada came out with some hawkish commentary at its meeting…

*MACRO CREDIT*

Some excitement as Bank of Canada tapers bond purchases slightly early

CAD currency rallied this week as the Bank of Canada followed through on QE expectations, scaling back purchases to a CAD3 billion weekly run rate. BoC reiterated its pledge not to hike rates until slack is absorbed, it anticipates that could happen in 2022 with inflation at target by the latter half of that year. According to Bloomberg, that’s a pull-forward of expectations from “into 2023” in March. The rest of the statement also read quite hawkish, which referenced that consumption will recover strongly, business investment should strengthen and despite pandemic risks, the third wave should be “temporary”.

Of course, being next door to the US, some observers couldn’t help but read across to the next actions of the US Fed. Jay Powell has a much more complex task and clearly has the weight of rest of the world watching to see how he will react.

Source: Bloomberg

Earlier in the week, Fed's Waller said Economy 'Ready to Rip' - DJ

Christopher Waller, the Federal Reserve's newest governor, says he expects the U.S. economy to expand by 6.5% this year, and inflation to rise to about 2.5% by the end of the year, compared with the Fed's 2% target, thanks to vaccination programs. He also forecasts a decline in unemployment to the low 5% range, from the current 6%, by year's end. Source: DJ

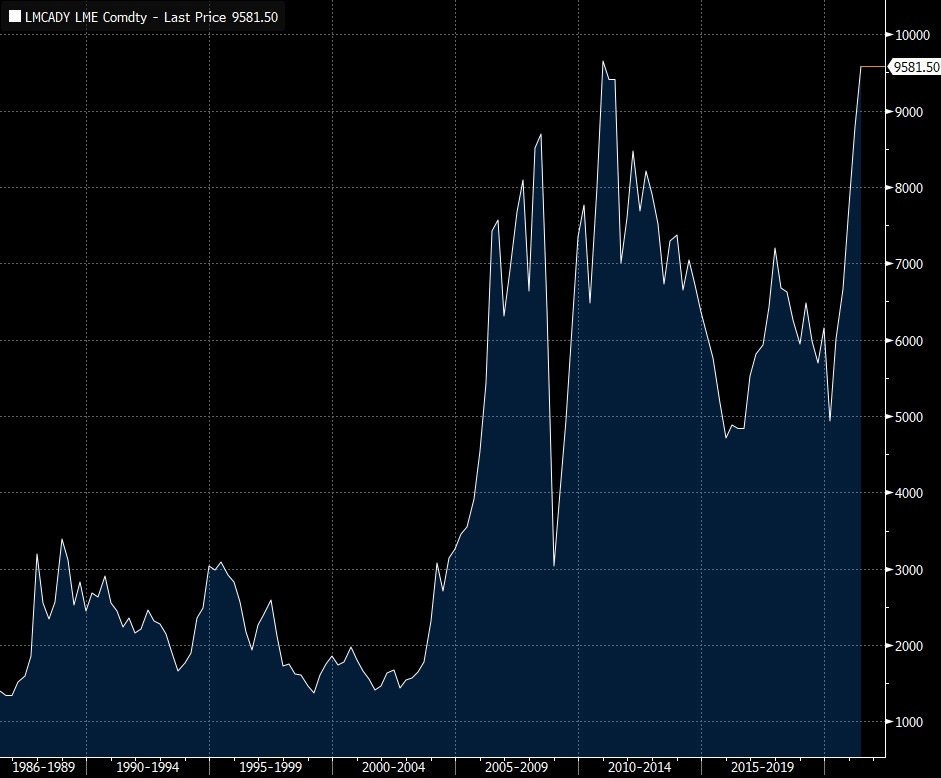

Excitement around Copper resumes…

I did not realise this but Copper has a real chance of breaking through its all time high set in 2011 of $10,190 (Source: Reuters).

From a credit perspective, one hopes that Copper Miners and related companies who benefit from an increase in the Copper price use this boost to de-leverage. Meanwhile, shareholders are probably hoping for increased payouts via share buybacks or dividends. The metal got a boost this week from sentiment due to Biden’s Earth Summit on Thurs/Fri and bullish comments from Chinese smelter Jianxi Copper who said they were confident of the metal hitting $10k per metric ton.

Debt issuers with Copper exposure include Glencore, Antofagasta, Anglo American, BHP, Rio Tinto, Freeport McMoran, Southern Copper First Quantum and Copper Mountain (not an exhaustive list but those were the names I am aware of).

Maersk Expects Suez Congestions to Affect Market Into 3Q

From Bloomberg: “Maersk says it expects that the Suez Canal congestion will affect container shipping into 3Q, according to emailed note to customers.

“The new normal is still being determined, but we expect the situation to remain tight into the third quarter,” Maersk says.

“Ports and infrastructures remain bottlenecks and because of this, ocean and inland delays are likely to continue in and out from high demand locations”

Maersk says it has ordered more containers to help remove bottlenecks, expects to add 260,000 TEU-sized container by end of 2Q.

Equipment supply and repositioning of empty containers “a concern” for the market, Maersk says “

Shippers / logistics companies should continue to benefit from higher freight rates which they are passing onto consumers/corporates.

*HY*

French State becomes a holder of Air France subordinated bonds

According to a statement by the Air France KLM, the French state subscribed for €3bn of its deeply subordinated bonds. Deeply subordinated bonds could also be described as Corporate Hybrids. I believe this is the first time the French state has bought into the corporate hybrid asset class directly. AF-KLM Statement.

US Airlines snippets from Q1 earnings so far:

Southwest Airlines Co. reported that government aid helped it notch a profit of $116 million in Q1, its first quarterly profit since the pandemic

Southwest Airlines said it expects that by June its operation will stop losing more cash than it takes in

Southwest’s flying capacity was down nearly 40% in the first quarter from 2019 levels, but by June, the airline expects to fly 96% of its pre-pandemic schedule.

Re Business Travel - Southwest, which is making a big push to lure more corporate accounts, said it is planning for business travel demand to remain down 50% to 60% at the end of the year.

United Airlines, which earlier this week reported that it lost $1.4 billion in the first quarter, said it needs business and international traffic to recover to 65% of pre-pandemic levels to turn a profit. Both segments are down about 80% now, as many international borders are closed and many businesses are still keeping workers home until at least later this year.

American Airlines stated that it is no longer looking to raise liquidity. AAL stated it hade $19.5bn liquidity. AAL also said it expects to be cash flow positive in the second quarter, excluding debt payments, in part driven by seasonality. American Airlines Group reported a loss of $1.25 billion on revenue of $4 billion, a smaller loss than in previous quarters in the past year.

Discounter Spirit Airlines Inc., which primarily serves vacationers, said Thursday that it plans to fly nearly as much in the second quarter as it did before the pandemic, operating 94.5% of 2019 capacity.

Alaska Air Group Inc., which reported a $131 million loss in the latest quarter, said summer fares in some cases are surpassing 2019 levels

Bonds of US Airlines have been largely unchanged (as liquidity picture remains solid), but I note that their stocks are taking a breather after a huge run up over the past few months:

Sources: WSJ / Company statements. Note that Southwest still retains Investment Grade ratings.

*FINANCIALS*

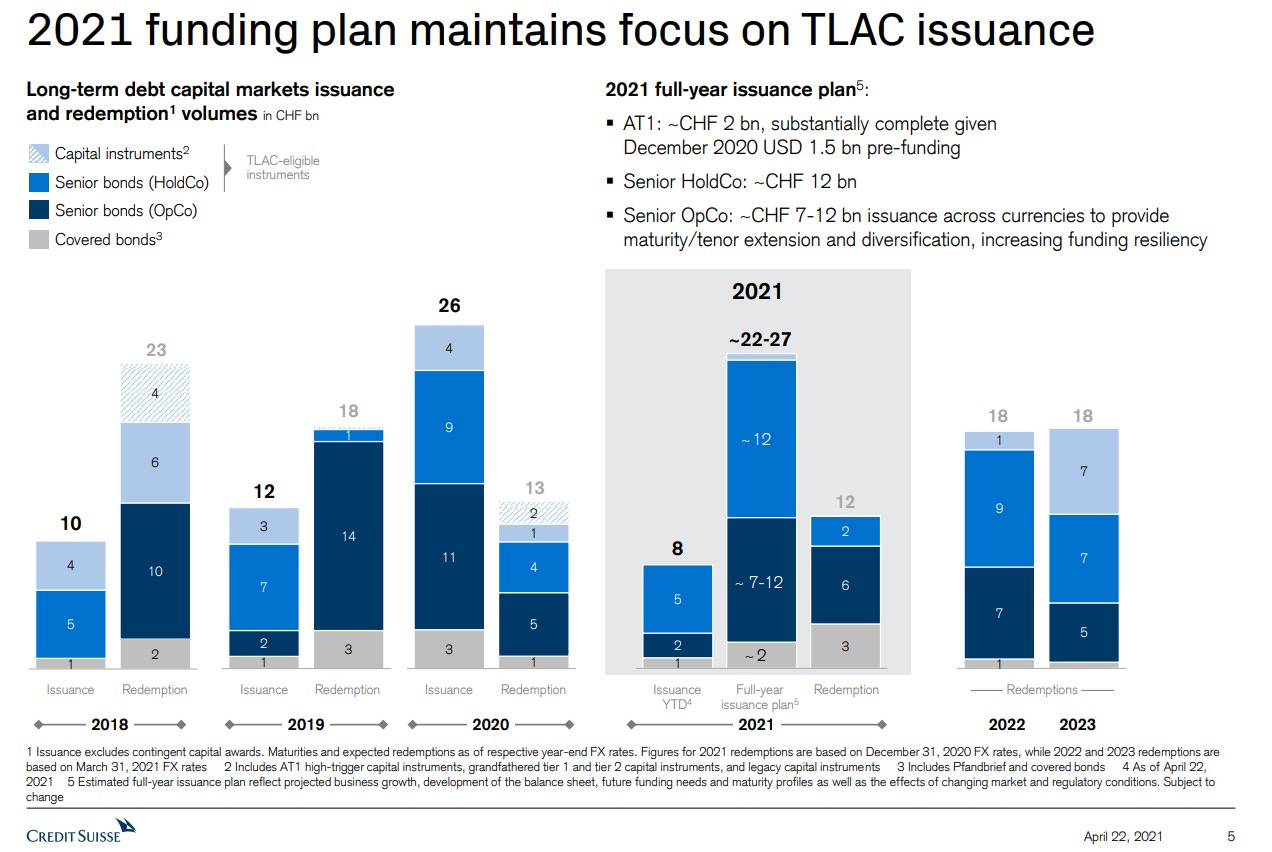

Credit Suisse Q1 Earnings call highlights - MCN, Archegos

Extract from Dow Jones re: Mandatory Convertible bonds (“MCN”)- “Credit Suisse Group AG said Thursday that it is raising capital via the placement of notes convertible into 203 million shares as it faces the hit from the collapse of U.S. investment firm Archegos Capital Management.

The notes were placed to a group of core shareholders, institutional investors and ultrahigh-net-worth individuals. "With the offering, we expect to further strengthen our capital position in line with our intention to achieve a CET1 ratio of approximately 13%," it said. The common equity Tier 1 ratio, a key measure of a bank's capital strength, was 12.2% at the end of March.

The bank said it expects a further impact of around 600 million Swiss francs ($654.3 million) from the Archegos issue in the second quarter, having already posted a CHF4.4 billion charge in the first quarter.”

Re: Archegos, these were some interesting snippets on the earnings call:

“I'm very satisfied that we have essentially gone out of the [Archegos] exposures now. We have, as we said, reduced the exposures by over 97% to a very moderate number now, which we are managing through to the coming weeks with the clear intention that we will get as quickly as possible to a zero level. “ - CEO Gottstein

“…I think the second point I'd make is, it is an exceptional event. I think the last time the industry has seen anything like this was LTCM in terms of its size and consequence. It is an industrywide issue. But that said, I think as Thomas has summarized, we've obviously conducted an immediate read-across to anything similar, any other immediate lessons learned to ensure that that is not the case within the rest of our prime portfolio” - CFO Mathers

There was much more discussed, including regarding CS’s Greensill exposure.

The proactive issuance of the mandatory convertible notes and the lack of further deterioration linked to Archegos/Greensill saw CS AT1 bond prices improve post the results.

Source: CS Fixed Income Investor presentation

Bank legacy CMS - Another call, this time DB call one of its bonds

In what seems to be an almost weekly occurrence now, another legacy security has had a redemption notice. This time, its DB that have called its 300m sized DB Capital trust 1 CMS 1.75% issue. Link.

*EMERGING MARKETS*

A quick look at the situation in Peru

Peru’s hard currency bonds have traded down lately on fears that a socialist candidate might eventually become its leader. This extract from Reuters:

“Peruvian socialist presidential front-runner Pedro Castillo assured the Andean nation on Thursday he would not nationalize companies and would honor the rule of law, a move aimed at calming jittery markets after a second opinion poll showed his lead growing against right-wing rival Keiko Fujimori.

Castillo remains in pole position to win the presidency in a second round ballot set for June, according to a Datum International poll that showed him garnering 41% against 26% for former lawmaker and three-time presidential candidate Fujimori.

Peru's sprawling mining industry, the world's No. 2 copper producer, has expressed some alarm about Castillo, who has gained increasing support in Peru's rural hinterlands and has proposed to redraft the country's constitution.”

I’m no expert on Peru but know that in the bond market they tend to price with low coupons (in a similar fashion to Philippines). So when negative news hits (bond market does not tend to like socialist candidates), there is little margin of safety for bond investors that bought bonds with low single digit coupons.

I recall that the Peru bond issuance in April and November 2020 were extremely popular with many accounts getting zeroed. Many non-EM investors would be surprised to learn that Peru issued a July 2121 bond @ 3.23% in USD for a credit that is rated A3/BBB+/BBB+. This bond was issued last year at a price of 98.5 and now trades at around 81-82.

The great thing about EM is that there are some predictable patterns that tend to play out time and time again, especially related to elections. The flow diagram (in a good situation) usually goes like this:

EM Election Uncertainty -> Bonds sell off -> Socialist candidate looks like they might win -> Bonds sell off more -> Socialist candidate makes market friendly noises -> Bonds rally…

A big reason for the huge volatility in EM seems to be because of the large presence EM managers in DM locations (North America, London, Europe), where the propensity for volatility is that much less than managers in EM locations.

Russia hiked rates more than expected to 5.0%

The decision to raise the rate from 4.5% to 5% comes amid a weak rouble, high inflation and flaring geopolitical tensions, see the Al Jazeera article for more details.

Russia Orders Some Troops to Withdraw From Ukraine Border WSJ

Ruble and Ukrainian assets continued to rally towards the end of the week after some initial nervousness around further escalation of tensions and a possible conflict between Russia and Ukraine. WSJ

Fitch Affirms India at 'BBB-'; Outlook Negative

Extract: “India's rating balances a still strong medium-term growth outlook and external resilience from solid foreign-reserve buffers, against high public debt, a weak financial sector and some lagging structural factors. The Negative Outlook reflects lingering uncertainty around the debt trajectory following the sharp deterioration in India's public finance metrics due to the pandemic shock from a previous position of limited fiscal headroom. Wider fiscal deficits, and government plans for only a gradual narrowing of the deficit, put greater onus on India's ability to return to high levels of GDP growth over the medium term to stabilise and bring down the debt ratio.”

On the virus it said this: “a recent surge in coronavirus cases poses increasing downside risks to the FY22 outlook. This second wave of virus cases may delay the recovery, but it is unlikely in Fitch's view to derail it.”

It is interesting that Fitch made this comment,, which could have been the reason behind the modest strengthening in short dated Indian credit towards the end of the week.

Colombia Affirmed at BBB- by S&P After Govt Presents Tax Bill

Extract from Bloomberg -- Colombia’s long-term foreign currency debt rating was affirmed by S&P at BBB-, the lowest investment grade score, while the outlook remains negative.

“The Colombian government reaffirmed its commitment to fiscal sustainability with its recent tax reform proposal to Congress,” analysts Manuel Orozco, Joydeep Mukherji and Sebastian Briozzowrite in statement

“We expect the tax reform package that the government recently presented to Congress will pass, but considerable uncertainty remains about its final contents, given the likelihood of amendments made by legislators”

“We could lower our ratings on Colombia over the next 12 months if the recent weakening in public finances is not contained and reversed, resulting in the government’s debt burden exceeding our current expectations”

Nigerian Senate approves fresh loan of $1.5b, €995m

The loans were part of the external borrowings President Muhammadu Buhari had requested in May 2020, for the Red Chamber to approve for financing various priority projects of the Federal Government and to support the state governments facing fiscal challenges.

€995 million is to be sourced from the Export-Import Bank of Brazil is to finance the Federal Government’s Green Imperative Project and the $1.5bn will be sourced from the World Bank to finance critical infrastructure in the aftermath of the COVID-19 pandemic across the 36 states and the Federal Capital Territory (FCT). See link for details.

Kenya is looking to extend its debt maturity profile

In a similar move to Ghana, Kenya is looking to reduce near term debt liabilities and extend out its debt profile. Kenya has a 2024 bond which appears the most likely candidate for a tender if they manage to issue longer dated bonds successfully. See link for more detail.

AlphaCredit Bonds Fell 40pts after $ 200M Derivatives Error

Extract of Bloomberg: “Alpha Holding SA’s bonds plunged after the Mexican non-bank borrower recognized accounting errors in derivative positions that will require it to review its 2018 and 2019 financial statements.

The company’s $ 300 million in dollar bonds due 2022 fell more than 40 cents to 35.75 cents on the dollar on Wednesday, according to Trace, while $ 400 million of notes due 2025 plummeted about 34 pennies. In a statement, the company said it expects an impairment of most of the 4.1 billion pesos (US $ 206 million) reported as other assets and accounts receivable on its September 30 balance sheet.

AlphaCredit, as the firm is known, said it had found the errors after an internal review and after discussions with audit firms KPMG and Deloitte. The errors relate to the company’s reserves for credit losses, reserves for certain accounts receivable and the amortization of certain capitalized expenses, according to the press release.

“The company is working diligently with its current and predecessor audit firms to complete the analysis of accounting errors,” AlphaCredit said in the statement. Representatives for the lender declined to comment beyond the published press release.

There was chatter (from an EM publication) that a bondholder group is grouping together ahead of a potential restructuring.

The additional vaguely interesting point about Alpha Credit is that Softbank had previously made a $100m equivalent investment in Alphacredit.

*RATINGS*

Caterpillar Upgraded to A2 by Moody's

HeidelbergCement Upgraded to Baa2 by Moody's, Outlook Stable

U.S. Steel's long-term rating was affirmed by S&P at B- | Outlook to positive from stable

Fitch Ratings: Pressure on Credit Suisse Continues Despite Capital Increase

Moody's affirms Southwest Airlines' Baa1 senior unsecured ratings, changes rating outlook to stable

Moody's affirms W. P. Carey's Baa2 ratings; outlook revised to positive

Daimler Outlook Raised to Positive by S&P

Fitch Affirms CRH at 'BBB+'

S&P Upgrades Greece To 'BB'; Outlook Positive

Romania Affirmed at BBB- by Fitch

Botswana Downgraded to A3 by Moody's, Outlook Stable

United Kingdom Affirmed at AA by S&P

Italy Affirmed at BBB by S&P

*GREEN BONDS*

EU publishes rulebook to classify ‘green’ investments - Euractiv

“The European Commission on Wednesday (21 April) unveiled a first batch of implementing rules under the EU’s sustainable finance taxonomy, spelling out detailed technical criteria that companies need to comply with in order to win a green investment label in Europe.

The taxonomy rule book introduces a labelling system for investment that could divert hundreds of billions in funds to industries and companies that win a “sustainable” label for all or part of their activities.

It covers 13 sectors, including renewable energy, transport, forestry, manufacturing, buildings, insurance and even the arts, which together account for nearly 80% of EU greenhouse gas emissions, the European Commission said.

A decision on gas and nuclear, the two most controversial aspects of the taxonomy, was delayed and will be dealt with separately.

“The taxonomy describes which economic activities are in line with the Paris Agreement,” and its objective of limiting global warming to 1.5°C, said Vladis Dombrovskis, the European Commission vice-president in charge of the economy.

It will do its part by “helping companies and investors to know whether their investments and activities are really green,” Dombrovskis said.

In short, “it sorts green from greenwash,” he added.

“Today’s new rules are a game changer in finance,” said Mairead McGuiness, the EU’s financial services commissioner, who pointed out that “significant investments are required” to meet the EU’s climate goals.

Indeed, meeting the EU’s 2030 climate goal will require €350 billion of investments every year, according to the Commission. And all companies should be able to contribute, even those that are not yet 100% green, McGuiness said.

“We need all companies to play their part, both those already advanced in greening their activities and those who need to do more to achieve sustainability,” she said in a statement.”

It is only a matter of time until we see a global standard for green investing , just like IFRS accounting standards that enable companies to be compared and appraised on a like for like basis. With respect to the EU, it will be interesting to see how they deal with Gas and Nuclear since there are large issuers (including those with state ownership) which would be affected by any new regulations.

Picard pulled its €1.71bn sustainability-linked bond issue, citing market conditions

According to IFR, this Picard deal was the first European high-yield deal to be pulled in almost a year. The three-part issue would have been the largest in that format to be priced in the European junk market. While there appeared to be pushback on the aggressive pricing by the leads and the issuer, the other factor worth considering is the deal indigestion in EUR HY due to the number of deals that have been coming to market lately. IFR have covered the issue re Picard well.

I purposely stuck the story on Picard in the green bond section to make the point that investors are not afraid to pushback on deals in the green space too if the pricing/terms are too aggressive. Issuers should not be able to just get low funding costs by slapping a “green” label on their bond issues.

*F.I LINKS*

Fund Flows - BOFA / EPFR Global

Investors appear to be checking out of US Corporate Bonds…

…And going into US Treasuries, according to this BNY data.

When will spreads change direction?

MarketAxess - The Giant Bond Trading Platform reported Q1 earnings

UK pares bond sale plans after budget deficit undershoots - BBG

Codere is to restructure its debt for the second time since the beginning of the pandemic

Disclaimer: This is not investment advice. These are my own views, and not those of any employer. I may have positions in securities listed in this blogpost.