Weekly Global Credit Wrap - W/E 22 Jan 2021

Collection of the most notable things I picked up this week in Global Credit

*Contents list*

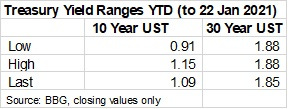

10 Year and 30 Year US Bond Ranges YTD

US Tips at record lows - WSJ

Main Credit Moves MTD

US HY issuance on track for busiest January on record - BBG

Investment Grade Bond Funds are underperforming HY Funds YTD: WSJ

Investment Grade issuers continue to obtain cheap financing

Qatar fund put pandemic bets on distressed debt, high-grade bonds - RTRS

Another European AT1 called

Allianz called some “Fixed for Life” bonds at par, one of which was trading at a reasonable premium

Legacy UK/European Bank Capital continues to get taken out by issuers - BBVA this week

Defaults seen dropping as interest-coverage ratios return to pre-COVID-19 levels: S&P Global

2021 US Loan Default Rate In Line with 2020; HY Trending Lower:

M&A leverage hit five-year high, according to Covenant Review - BBG

AMC Entertainment closes $100M debt financing with Mudrick Capital Management

Lufthansa Cuts Costs Faster than Expected, Says CEO

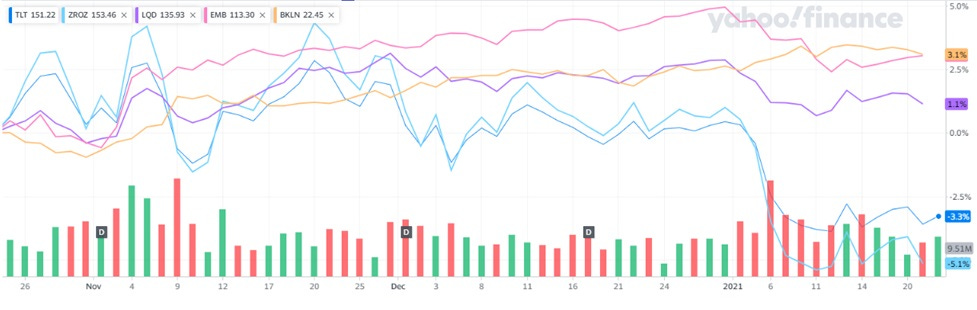

3m Selected Bond ETF Performance

Tesco tendered for some of its old corporate bonds and issued its first sustainable bond

Chile Sells Biggest Latin American Sovereign Sustainability Bond

Animal Spirits - Talk Your Book: Investing in Fixed Income

Giant firms have a hidden borrowing advantage that has helped keep them on top for decades: Research from City University

*Rates*

10 Year and 30 Year US Bond Ranges YTD

US Tips yields are at record lows - WSJ

Investors are hanging on to bonds that protect against inflation even as they sell other U.S. government debt, a sign many trust the Federal Reserve to hold interest rates steady even if the economy picks up steam. WSJ

*Credit*

Main Credit Indices Moves MTD:

EUR 5Yr XOver +11bps to 254

EUR Subfin +5bps to 116

CDX HY 5 Yr: +12bps to 305

CDX EM 5Y: +19bps to 171

Moves in Investment Grade Credit indices not worth the effort highlighting…! Source: BBG

US HY issuance on track for busiest January on record - BBG

The U.S. junk bond market is just $5.5 billion away from the busiest ever January month with borrowers selling debt for anything from refinancing to funding acquisitions and leveraged buyouts at record-low rates as yields dropped to another all-time low of just 4.13%. h/t @gowrinyc / @bloomberg

Investment Grade Bond Funds are underperforming HY Funds YTD: WSJ

Its only a few days into the year, so not really a notable trend so far. However the rise in US Treasury bond yields has hit longer duration Investment grade funds more than HY Funds, which compensate more for the sell-off through wider credit spreads. Read more here: WSJ

Investment Grade issuers continue to obtain cheap financing

Some examples from the week set out below:

Air Lease - $4.8bn market cap aircraft listed lessor

Issued $750mm of 3yr paper @ +72bps over the Treasury.

Rating: BBB

Ticker: AL 0.7% 02/15/24

Tesco - $32bn market cap UK Supermarket

Issued €750mm sustainability linked bonds @ 99.335 to yield 0.455%

Issuer Ratings: Baa3/BBB-/BBB-

Ticker: TSCOLN 0.375% 07/27/29

Vonovia - $37bn German Real Estate Co

Issued €500m of 20yr senior paper @ 98.355 to yield 1.092%

Exp. Ratings: BBB+ (S&P)

Ticker: ANNGR 1% 01/28/41

SRC: BBG

Qatar fund put pandemic bets on distressed debt, high-grade bonds - RTRS

- Qatar Investment Authority is generating strong returns on a multi-billion dollar bet it made on distressed debt and highly rated bonds at the start of the COVID-19 crisis, two sources familiar with its move said. RTRS

*Financials*

Another European AT1 called

Svenska Handeslbanken issued a call notice for its Additional Tier 1 Bonds (BBG DES page). This follows Intesa’s call notice, which marked the first AT1 to be called this year. Source: BBG/Svenska

Allianz called some “Fixed for Life” bonds at par, one of which was trading at a reasonable premium

Legacy UK/European Bank Capital continues to get taken out by issuers - BBVA this week

BBVA Called its legacy Tier 1 CMS Bond (ISIN:XS0225115566)

*HY*

Defaults seen dropping as interest-coverage ratios return to pre-COVID-19 levels: S&P Global

The average interest-coverage ratio — a measure of a company's ability to repay its debts calculated by dividing earnings before interest and tax, or EBIT, by the cost of its debt-interest payments — of investment-grade U.S. companies jumped to 6.6 in the third quarter of 2020, the highest level since at least the third quarter of 2018, up from a low of 4.99 in the second quarter of 2020. The ratio had sunk from 6.1 at the end of 2019 as the outbreak morphed into a global pandemic and drained revenues. Read more here: S&P Global

2021 US Loan Default Rate In Line with 2020; HY Trending Lower:

Default rates for US institutional leveraged loans in 2021 are expected to be consistent with 2020 rates, while the high-yield bond default rate will trend lower, says Fitch Ratings. The economic effects of the pandemic continue to weigh on issuers’ operating profiles, but recent refinancing activity that has pushed out maturities is a key factor supporting a reduction in its default rate forecasts for 2021 and 2022.

Read more here: Fitch

M&A leverage hit five-year high, according to Covenant Review - BBG

Leverage for syndicated loans backing U.S. M&A has surged to at least a five-year high, according to a new report from Covenant Review.

As of the fourth quarter, average first-lien and total leverage for the loans analyzed was 4.83 times and 5.93 times, respectively, according to Covenant Review. That’s the highest level since the firm began tracking the data at the start of 2015, and is up from 4.92 times and 5.62 times in the third quarter, respectively

Src: BBG

Netflix euro bonds rally as company steps back from debt raising: S&P Global

Netflix bonds were up this week after the company announced Jan. 19 that it will no longer use the debt markets to raise financing to fund its operations. On its conference call, management stated it is closing in on turning FCF positive, a target which the market thought would not be achieved for at least a few years still. Netflix’s credit ratings have moved up in recent months and stand 2 notches away from Investment Grade now on S&P’s rating scale. Read more: S&P Global

AMC Entertainment closes $100M debt financing with Mudrick Capital Management

AMC Entertainment Holdings Inc. has issued $100 million in 15% cash/17% PIK toggle first-lien secured notes due 2026 to Mudrick Capital Management.

AMC is the largest movie exhibition company in the world, most recently reporting roughly 953 theaters and 10,700 screens.

Source: S&P Global

AMC stock is up around 60% YTD.

Lufthansa Cuts Costs Faster than Expected, Says CEO

Lufthansa Group has taken €3 billion of a €9 billion Covid relief package commitment from the German government and management believes it will get through the pandemic without drawing on the entire allotment thanks to aggressive cost-cutting, Lufthansa Group CEO Carsten Spohr reported during a Eurocontrol “StraightTalk” interview Thursday. Since the onset of the Covid crisis last spring, Lufthansa has effectively slashed its cash burn in half, from €1 million per hour to €1 million every two hours, he added.

“It shows that our cost-cutting has gone a lot faster than we would have thought,” said Spohr. “But there a few things we need to do that go beyond the pandemic, so we have decided to shut down two airlines within the Lufthansa Group. We started with 14 airlines; we’ll come out of the pandemic with 12 airlines only.” AIONLINE

*Bond ETFs*

Rates sensitive bond ETFs (TLT) and (ZROZ) have underperformed as US Treasury yields have risen.

3m Selected Bond ETF Performance

To a lesser extent, long duration investment grade bond corporate bond ETF (LQD) has also weakened YTD.

BLKN - Leveraged loans index has helped up well and is up 0.4% YTD whereas traditional HY ETF (HYG) is flat on the year. Presumably this is due to the floating rate element of lev-loans. An ETF many people forget about is the Convertible bond ETF which has had a strong start to the year (below).

*Sustainable Corporate Bond Investing*

Tesco tendered for some of its old corporate bonds and issued its first sustainable bond

€750m bond with a 0.375% coupon offers an 8.5-year maturity and is the first bond of its kind to be issued by a retailer

Chile Sells Biggest Latin American Sovereign Sustainability Bond

(Bloomberg) -- Chile raised a total of about $4.25 billion in euro and U.S. dollar markets Tuesday amid strong investor demand, including the biggest sustainability bond issued by a Latin American sovereign in foreign debt markets.

The nation borrowed $2.25 billion in a two-part dollar-denominated sale that included $1.5 billion of sustainability bonds, the biggest from the region, according to data compiled by Bloomberg. Chile also raised $1.65 billion euros ($2 billion) in European markets to fund green and social projects.

The longest-term portion of the European deal -- a 1.25 billion euro security maturing in 30 years -- represents Latin America’s biggest foreign currency social bond from a sovereign. That debt was sold at 98.814 cents on the euro to yield 1.298%.

Both the dollar and euro offerings were oversubscribed by investors with dedicated environmental, social and governance mandates, Chile’s finance ministry said in a statement Tuesday. ESG-conscious buyers gobbled 48.5% of the total euro sale and the interest rates obtained on the green tranches maturing in 10 years and above were the lowest obtained by the country, according to the ministry.

*Long Reads / Listens on Fixed Income*

Animal Spirits - Talk Your Book: Investing in Fixed Income

On today's show, Michael and Ben talk with Gibson Smith of Smith Capital Investors about how the structure of the fixed income market has evolved over time, what happened to bond funds and ETFs in March? The potential problems with plain-vanilla bond indexes, and much more Find complete shownotes on our blogs... Ben Carlson’s A Wealth of Common Sense Michael Batnick’s The Irrelevant Investor Like us on Facebook And feel free to shoot us an email at animalspiritspod@gmail.com with any feedback, questions, recommendations, or ideas for future topics of conversation.

Giant firms have a hidden borrowing advantage that has helped keep them on top for decades: Research from City University

When the COVID-19 pandemic first hit, it seemed like the day of reckoning for over-stretched corporate borrowers was finally at hand. For years, pundits and policymakers had been warning about a dangerous build-up of the debt of “non-financial firms”, meaning all those that aren’t in finance, insurance or property.

According to an OECD report from 2019, their debt doubled globally in the decade following the crash of 2008-09. Surely the devastation wrought by a global pandemic would be enough to pop this giant bubble, setting off a wave of corporate defaults and putting the global financial system at risk of another major crisis?

Though corporate default rates climbed across the world in 2020, the long-anticipated collapse of the corporate debt market has not come to pass – at least not yet. This is thanks to government intervention, especially the unprecedented moves by central banks, including the Bank of England, to keep the interest rates on corporate bonds low by directly purchasing them.

These aggressive measures may have helped to avert a corporate debt catastrophe, but they’ve come at a hefty price. In 2020, global corporate debt issuance reached record highs, stoking fears that central banks have merely delayed the inevitable.

Disclaimer: Not investment advice. I may have holdings in the securities mentioned above.