Weekly Global Credit Wrap w/e 22 Apr 2022

Global rates continue march higher...

*OVERVIEW*

Rates - Bond yields rose across many markets again this week:

30 year UST went through 3% then retraced lower

UK 10 year Gilt passed 2% then retraced lower

The whole German curve is now positive

Major Australian Bond benchmarks 7 year and onwards now yield more than 3%

These moves have been driven by very hawkish commentary by the Fed Chairman and its members (esp. Bullard and his +75bps chatter) as well as the market re-calibrating to an aggressive rate hike trajectory and aggressive QT.

Front end nominal US Treasuries are now offering yields of 2.7 to 3.0%, levels unheard of for even Investment Grade credit for most of the QE and Pandemic era. Month to date, it is notable that the largest moves in UST have been in the longer maturities, i.e 7 year benchmark and longer are up by around 50bps.

Credit spreads - Credit indices did not experience a huge move this week besides the widening in CDX HY of 27bps such that it closed at +435bps.

Similarly not a great deal to talk about in cash credit spreads besides how robust US HY spreads remain in spite of the volatility. Some commentators have attributed this strength to the high exposure to the energy sector and the high proportion of BB credits that are in the HY index now vs history. However spreads are not as informative as the prices and yields of credit (which have moved a lot YTD).

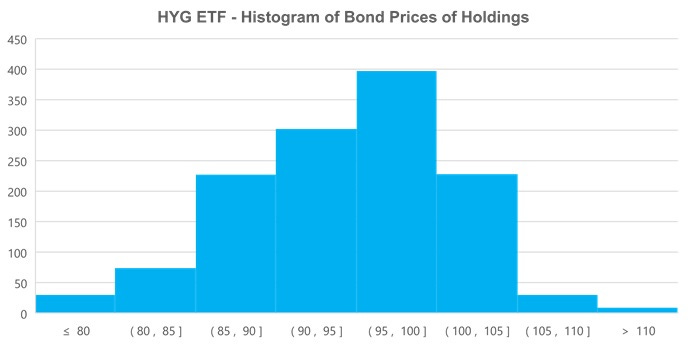

The chart below shows the breakdown of prices of the bond holdings in the HYG ETF (as an example). This shows a large number of bonds that are trading at a discount to par (100). I don’t have the data, but if one was to look back to say September 2021 (nearly the cyclical lows for Treasury yields), HY bond prices would have been more clustered around par or higher. The average yield on HYG is now 6.39%.

Source: iShares, 22 April 2022

Bond ETFs / Mutual Funds - The chart below has being doing the rounds this week regarding bond ETF performance:

Some special candidates need highlighting within that, i.e.:

LQD TR of -13.9%

EMB TR of -14.6%

TLT TR of -18.7%

However, the problem is not isolated to Bond ETFs, with some well known Investment Grade Global Credit Mutual Funds down 9-12% ytd.

*MACRO*

J-Powell key comments from IMF speech:

"50 basis points will be on the table for the May meeting."

"Markets are processing what we're seeing. They're reacting appropriately, generally. But I wouldn't want to bless any particular market pricing."

"It's too hot. It's unsustainably hot. It's our job to get it to a better place where supply and demand are closer together."

h/t Nick Timiraos of the WSJ for these.

Investment-grade Corporate Credit yields more than 4% now - 12 year high

US Mortgage bonds are trading as cheap as at the height of the pandemic in May 2020 - BBG

Extract: “Mortgage bonds are trading as cheap as at the height of the pandemic in May 2020, based on the difference between yields on current coupon mortgages and a blend of five- and 10-year Treasuries. The risk premium was 1.16 percentage point on Tuesday, while last year’s average was 0.7 percentage point. “

*COMMODITIES*

Capacity Constraints Drive the OPEC+ Supply Gap - Dallas Fed

Halliburton - giant oil services co says its oil drilling/fracking kit is almost sold out in North America

Copper - Peru declares state of emergency near a copper mine, halting 20% of national copper output - RTRS

Peru will declare a state of emergency near Southern Copper Corp's Cuajone mine, the country's prime minister said on Wednesday, as protests hit top mines in the Andean nation, halting 20% of national copper output.

*IG*

Earnings releases have been packed with great insights into the challenges and opportunities Corporates are facing right now - I link to a few here:

Nestle fends off cost inflation, helped by higher prices - RTRS

Nestle confirmed it expects to grow sales around 5% and keep margins broadly stable this year after higher pet food, dairy and coffee prices did not deter consumers in the first quarter, forecasting more price increases ahead.

Tesla seems to be able to pass on higher costs to its customers - Protocol

Tesla are likely to be tapping into the crowd of people willing to stomach higher prices for their vehicles, as an alternative to the high cost of Petrol/Diesel.

Continental - Tyre cost inflation drags down Group margin guidance - RTRS

AB InBev warns of €1bn hit from Russian venture exit - Irish Times

AT&T CEO sums up a strong quarter for the firm:

“Our momentum in growing customer relationships is reaching historical levels,” said John Stankey, AT&T CEO. “We had our best first quarter for postpaid phone net adds in more than a decade and our fiber broadband net adds remain consistently strong. Our results, including free cash flow, are in line with our expectations toward delivering on the full-year guidance provided at our recent Analyst Day.” AT&T Earnings

Reuters discusses higher cost impact on production at large mining firms

Anglo America, BHP, Rio Tinto were just some of the firms who highlighted higher than expected costs and impact of labour shortages on production.

Shares of these companies which had been on a tear pulled back this week after updating the market, along with some added weakness from the broader market. ETF shown below is iShares Global Metals and Mining Producers ETF.

Blackstone’s President Jonathan Gray made an timely comment on picking businesses for investments:

“The biggest challenge is to avoid businesses that are highly exposed to rising rates and/or inflationary pressures that don’t have pricing power,”

“You want to find businesses that can produce revenue growth well in excess of these inflationary pressures.”

*FINANCIALS*

AT1s continue to get redeemed - Unicredit 9.25%

A call notice was issued for this high coupon EUR Unicredit AT1, continuing the theme of AT1 paper being called at first call this YTD.

Senior Bank paper seeing flurry of issuance

With subordinated financials spreads not looking especially attractive for issuers, they are tapping in to demand for medium dated senior paper. Sterling was an area of activity this week with a trio of Banks coming to issue paper: Wells Fargo, GS and BofA, mainly at notable concessions to secondary paper. JP Morgan issued senior paper in Dollars too which appeared to be received very well due to favourable pricing for investors.

*HY*

Airline heavy weekly wrap with a number of airlines reporting and issuers coming to market.

Vistajet - The Private Jet operator raised $500m to fund its acquisition of Air Hamburg.

The company’s five-year note offering was upsized from $440m. This is the second HY deal Vistajet has issued in a matter of months.

American Airlines earnings call highlights - Fool.com

Sees Airfares up 15% Over Pre-Pandemic Levels

Deleveraging our balance sheet remains a top priority, and we are committed to significant debt reduction in the years ahead.

…we remain on track with our target of reducing overall debt levels by $15 billion by the end of 2025. During the quarter, we made $344 million in scheduled debt payments and completed $317 million in open market repurchases of our $750 million unsecured senior notes maturing in June. To date, we have reduced our overall debt levels by $4.1 billion from our peak levels in the second quarter of 2021. We expect to make $1 billion of scheduled debt payments in the second quarter, which includes the remaining outstanding balance of the unsecured senior notes.

CFO: …But our targeted cash level was at $7 billion. And so, right now, we're holding out of the cash. And when we see the recovery, and it's holding up and the cash is holding up, we will use that cash to pay down debt. And I think we'll take it down to somewhere in the $10 billion to $12 billion range as we look forward.

United Airlines earnings highlights

Expects to return to profitability in the second quarter on a robust operating revenue outlook, including total revenue per available seat mile (TRASM) of approximately 17% over 2019, the strongest second quarter revenue guidance in company history.

The company expects to be solidly profitable in the second quarter with an approximate 10% operating margin just 2.9 points less than 2019 operating margin and 3.5 points less than 2019 adjusted operating margin, despite cost headwinds driven by the recent fuel price spike.

Reported first quarter 2022 ending available liquidity of $20 billion.

Reported a decline in total debt of over $700 million.

United has said it is passing along a majority of its fuel cost to customers. The airline’s average fares are more than double what they were a year ago, according to data from Cowen.

EnQuest (North Sea Oil Co) announced results of exchange of its ££ 2023 Retail Bonds

Company issued £131m (net of fees) of the 9% coupon 2027 bonds made up of around £54m new money and around £79m as a part of the exchange offer which leaves around £111m of the old EnQuest 7% £ 2023 notes.

Will Elon carry out one of the biggest LBOs on record to buy Twitter?

Newspapers highlight the $46.5bn financing package to take over twitter. According to the FT, Musk has lined up $25.5bn in debt — including a margin loan of $12.5bn against his shares in the Tesla, from a group of banks led by Morgan Stanley.

Considering the amount of volatility in public markets, pulling this deal off would be one hell of an achievement for Musk. I also wonder what the impacts of pledging $62.5bn of shares in Tesla to secure the loan will have on an already volatile Tesla stock.

*EM*

Ukraine in talks with EU, U.S. on issue of 'peace bonds' - media/Interfax

Ukraine is negotiating a potential issue of "peace bonds" designed for retail investors from the United States and European diaspora, Bloomberg reported citing sources.

EM HC new issuance running 40% below last year

A US Bank put out a research note highlighting that EM HC issuance is lagging by around 40% YoY for the same point. However, macro pressure from upcoming Fed QT and Fed rate hike have dampened this positive technical. EM bonds come with high levels of carry which means a high re-investment requirement from EM Bond Funds. This could be the reason behind why sectors less exposed to the Ukraine/Russia War (e.g African Telcos/Towers) have seen their prices stabilise after some volatility in March.

World Bank Head Seeks New Debt-Resolution Process for Developing Nations - BBG

World Bank chief says current system predates China’s rise, Malpass calls out non-disclosure clauses in debt agreements.

Pemex to Pay Debt Amortizations on Its Own Again This Year - BBG/Worldoil

(Bloomberg) -Petroleos Mexicanos will resume paying its debt amortizations on its own this year instead of relying on the government to meet the obligations, according to a Finance Ministry official.

Turkish Airlines Signs Codeshare Deal With Brazil’s Gol - Simpleflying

The Brazilian carrier GOL signed a codeshare agreement and a frequent flyer partnership with Turkish Airlines. This new agreement allows passengers from the Turkish flag carrier to connect seamlessly with GOL’s entire network in Brazil and several destinations across South America.

Sri Lanka FinMin interview with Bloomberg says talks are centered around “loan recast.”

Over the weekend, Economynext reported that Sri Lanka is set to appoint debt advisors in two weeks, speed up Extended Fund Facility with the IMF.

*RATINGS*

Fitch affirmed ratings of Egypt and Ivory Coast

Egypt Affirmed at B by S&P

Fitch affirmed Scentre Group at A, outlook stable

S&P raised the Greek rating from "BB" to "BB+", with a positive outlook

S&P affirms Italy 'BBB/A-2' Ratings; Outlook Positive

*CREDIT TRADING*

MarketAxess reported Q1 earnings:

EBITDA for the quarter was $106 million and EBITDA margin was 57%.

…we are only three weeks into the new quarter, estimated high-grade, high yield, and emerging market, market share are all tracking well above Q1 levels.

Combined U.S. high grade and high yield estimated market share is currently above 20%, up from 19.1% in Q1.

We believe that higher bond yields and less Central Bank quantitative easing will support higher market volatility in the periods ahead. Higher bond market volatility is already driving increased demand for open trading liquidity in U.S. Treasuries and credit versus prior quarters. This is coming through in market share trends, active client firms and overall trading volumes.

Live markets for credit had record trading volume in the first quarter, with record trade count already surpassing full-year 2021 levels.

Our live markets for treasuries, reached record volume of $1.5 trillion during the quarter, an increase of 40% from last year and a record 2 million trades, up 64%.

We've seen ETF activity in credit accelerating materially this past quarter

Looking at its share price performance, bond trading platforms appear to be underperforming stock trading platforms with MarketAxess the biggest laggard YTD.

*BEST OF FINTWIT/LINKS*

@charliebilello: “US Bond market is now down 11.2% from its high in August 2020, the largest correction we’ve seen in 40 years”

Powell continues to cite Volcker example..

US Homebuilding - Personal finance Influencer with 43k followers said this about higher rates & prices, what will most homebuyers do?

For the first time on record, US inflation is above the emerging market median - Macro Hive