Weekly Global Credit Wrap w/e 18 March 2022

Relief rally led to thawing of more funding markets...

*OVERVIEW*

Credit spreads

Notable moves over 5d:

CDX IG tightened in 11bps to 64bps

CDX EM tightened in by 68bps to 278bps

CDX HY tightened in 43bps to 358bps

Xover tightened in 47bps to 339bps

Sub Fin CDS tightened in 24bps to 149bps

Month to date, all major credit indices are still wider than where they began.

In terms of cash credit, there were similarly positive moves in US IG, US HY and Bank CoCos. US HY credit spreads have tightened into +370bps whereas Pan European HY still trades above 400bps (+438). EM cash credit spreads look to have tightened 37bps on the month to date.

Bond ETFs

*Note I use Bond ETFs to describe action in Fixed Income Assets here since they are the easiest to track compared to the hundreds of thousands of Mutual Funds out there."

Decent sized moves this week with HYG, JNK and EMLC (EM Local CCY Bond ETF) rallying more than 3% over 5d. EMB and CEMB put in some respectable performances adding around +2.7-2.8% over 5d. Interestingly, TLT posted a positive +1.3% return too over 5d.

Funding Markets

The combination of a specific purported plan towards peace in Ukraine and getting the Fed meeting decision out of the way helped funding markets. I made the comment last week on whether we would see HY/EM/Financials new issue markets start to re-open. Well, EM and Financials markets did re-open with something of a bang. Nigeria and Turkey raised substantial amounts of public bonds and DB and CS issued in the fins market. Across markets, I think its fair to say that better quality issuers can issue, paper, but there is clearly a "cost of doing business" for them at elevated spreads.

Russia / Ukrainian credit

Continued buying of specific Russian credits continues, and there appears to be a slow grind higher of some specific Ukrainian credits too.

*MACRO*

UST - This is the longest (581 days) and largest (-6.6%) correction in US bonds that we’ve seen in recent history - Charlie Bilello

On Wednesday, the 30 year US Treasury went through the 2021 high and hit as high as 2.478%

Gregory Daco provided a solid round up of the Fed decision last week:

Mortgage rates rise above 4% for the first time since 2019 - CNN

US Real Estate specialist on rising rates vs homes supply:

Fed policymakers say dramatic rate hikes may be ahead | RTRS

March 18 (Reuters) - Two of the Federal Reserve's most hawkish policymakers on Friday said the central bank needs to take more aggressive steps to combat inflation, and two others said they would be open to it – one of whom just six months ago envisioned a 2022 with no rate increases at all

2 and 5 year UK Gilts rallied on Friday despite rate hike by BoE on Friday - RTRS

*New issuance*

Post the Fed meeting, the number of new issues/facilities being signed accelerated, demonstrating the authority that it has on Global Markets.

*Note this is not an exhaustive list of deals, just ones which caught my eye/I found interesting.

IG:

Anglo American issued $1.25bn: Anglo American $500 million of 3.875% senior notes due 2029 and $750 million of 4.750% senior notes due 2052

EDP raised EU1.25bn of 7.5year Green senior bonds @ MS +100

EM:

Nigeria 7yr New Issuance priced at 8.375% with closing book size of $3.75Bn

Turkey, which is rated B+ by S&P launched $2 billion in bonds due 2027 for a yield of 8.625%.

SBI, GOVERNMENT OF SRI LANKA SIGN PACT FOR $1B CREDIT FACILITY - Business Standard

IG

Note US IG energy names got issuance done during this volatile period:

Diamondback Energy Inc issued new $750m 30-year bonds at 4.25% (BBB rated credit)

MPLX LP issued $1.5bn of 2052 bonds at 4.95%

ConocoPhillips Co: Issued $1.7bn of bonds with a 4.02% coupon and maturity 2062

EDF announces the conclusion of some bilateral term loans for a total amount of 10.25 billion euros

Financials:

Deutsche Bank raised EU1.5b 10.25NC5.25 T2 bonds at MS+330 – Coupon of 4%, for reference, note how this pricing contrasts to start of 2022 when DB raised a 11NC10 in USD @ +210bps on 4 January 2022.

Credit Suisse raised EU3.5b Debt Offering in 2 Parts with certain market participants highlighting the very wide pricing on the 10NC9 deal.

HY

Tesla delayed a ~ $1 billion secured bond offering -I think this is more down to Tesla being “stingy” about how much it wanted to pay for its debt, rather than the market being completely shut for the name. RTRS

*ENERGY*

Crude oil returned to the pre-Russia invasion level then bounced again to close around $107/bbl

India doubles down on move to procure crude oil from Russia – Hindustan Times

India is highly dependent on imports for its energy requirements, and almost 85% of the country’s crude oil needs is imported

*IG*

Lennar ($26bn market cap US Homebuilder) had earnings this week – comments re housing market and rates - Source: Earnings call

Exec chairman: “Buyers are seeking shelter and they are seeking shelter from inflationary pressures as scarce rentals see rents escalating and escalating housing costs can be controlled with an owned home with a fixed-rate mortgage”

“[Re demand]…earlier this week, management call, we surveyed almost exactly that question across our geographic footprint. And the answer is where that sales were ranging anywhere from strong to very strong

So there are cross currents out there, we have not seen to date any change in the demand patterns except toward strength, and we're watching it very carefully as you are. “

CFO: “As we've indicated for several quarters, the mortgage market has become increasingly competitive for purchase business, as refinance volumes and resale inventory has declined”

EDF launched a €3.1bn rights-offering - Link

Marubeni-owned aircraft lessor retrieves two Russian aircraft | RTRS

The U.S.-based aircraft leasing firm owned by Japan’s Marubeni Corp and Mizuho Leasing Co Ltd (8425.T) has recovered two of the 12 aircraft it has been leasing to Russian airlines, it said on Wednesday.

Air Lease says Russian law on leased jets could help in claiming insurance | RTRS

*FINANCIALS*

Another AT1 called (this time SEB 5.625%)

Primary market for AT1 remains closed temporarily, but the call notices keep coming.

Natwest sent redemption notice for two bonds of 1.5bn size each - Investegate

NAB to repay Undated Subordinated Floating Rate Notes issued on 9 October 1986 - Investegate

BBVA starts execution of next €1 billion of its share buyback program - BBVA

Phoenix Group (Life Insurance) reported record cash generation, no exposure to Ukraine/Russia in Credit portfolio - Link

*RUSSIA/UKRAINE*

Ukraine war bonds face falling numbers - IFR [15 March]

Extract: “Ukraine's ministry of finance completed its third auction of so-called "war bonds" on Tuesday, although even with the addition of a US dollar leg, the H5.404bn-equivalent (US$184m) raised was the lowest yet.

Reuters article re OFAC exemption for some Russian securities - Reuters

Extract: “In early March, however, the U.S. Office of Foreign Assets Control (OFAC) authorised transactions for U.S. persons for "the receipt of interest, dividend, or maturity payments in connection with debt or equity" issued by Russia's finance ministry, central bank or wealth fund - an exemption that runs out on May 25”

Russian State Leasing Firm Bondholders Receive Coupon in Dollars - BBG

Russia’s State Transport Leasing Company, GTLK, has paid the coupon on the $600 million bonds issued by its Ireland-based subsidiary due on March 10. It’s the second fully state-owned firm to pay in hard currency

*EM*

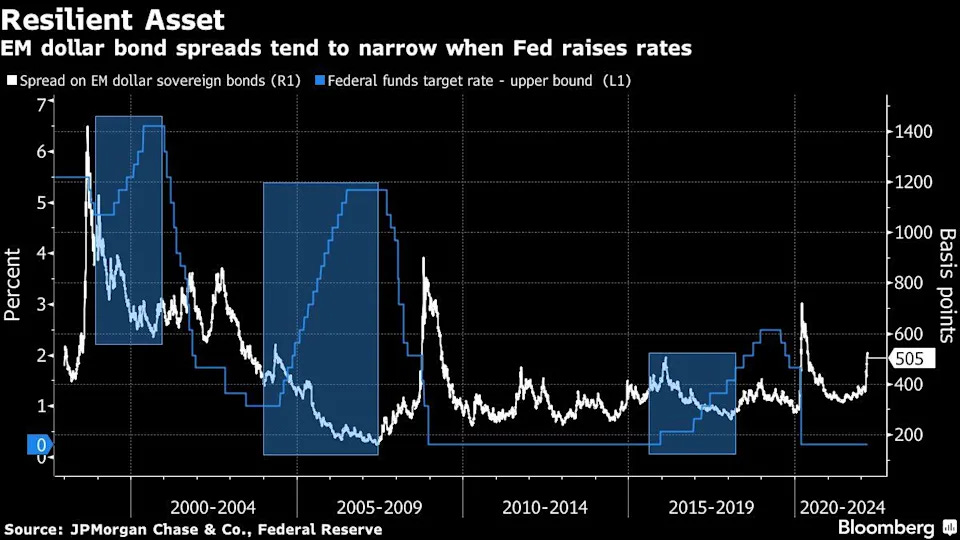

Emerging-market dollar bonds are starting to look like a bargain according to some FMs - BBG

Extract: “The extra yield offered by developing-nation sovereign debt over U.S. Treasuries has risen above 500 basis points, crossing a threshold breached only two other times in more than a decade. That’s drawing money managers including FIM Partners and Vontobel Asset Management to bet spreads will quickly tumble, just like they did following the previous spikes”

Egypt said to be in talks with IMF re funding - BBG

Brazil Central Bank raised the Selic rate by 100bps to 11.75% (expected)

Brazil President Jair Bolsonaro unveiled a social spending package that will inject 165 billion reais US$ 32.4bn) into the economy - BBG

Puma Energy Announces Agreement for Sale of Infrastructure Assets - Link

Puma Energy has agreed to sell a significant part of Puma Energy’s infrastructure and storage business to ITG Sàrl, the parent company of Impala Terminals… As a result of the transaction, if successfully consummated, it is expected that Puma Energy’s net debt (net of cash and cash equivalents and inventories) will become negative.

*CHINA*

On Wednesday, Chinese Vice Premier Liu He urged the roll-out of market-friendly policies to support the economy…RTRS

and caution in introducing measures that risked hurting markets.

Shenzhen eases lockdown as pandemic gnaws at China economy -

Extract: “Beijing (AFP) – China's southern tech powerhouse Shenzhen has partially eased lockdown measures, after President Xi Jinping stressed the need to "minimise the impact" of the coronavirus pandemic on the nation's economy.”

China Property sector saw a number of developments - BBG

China Developers Should Be Self-Reliant, Not Hope On Policy: AB

Defaulter Kaisa Dollar Bonds Surge On Reported Talks With SOE

Kaisa Talking to State Cos. on Investment, Cooperation: Cailian

China Will Not Expand Its Property Tax Trial This Year

Country Garden Exec., Supervisor to Buy up to 20m Yuan Co. Bonds

China CBIRC to Unveil Policies to Bolster Capital Markets

The China Property bond sector saw some extreme moves up after around 2-3 weeks of losses. Kaisa for example saw its bond prices double (from ten cents in the dollar to around 20 cents). The article in the BBG link has more details.

Zhengzhou is first city to relax curbs on second homes - Business Times

Government in Zhengzhou published 19 policies and the government in Hunan released 10 policies to boost the local real estate market. Story from 3 March.

Bloomberg index of Chinese HY posted its first daily gain Thursday in more than three weeks, and largest since January

Cifi (China Property developer) issued 1bn yuan bond with a 4.75% coupon

Equates to around $157mm USD.

*HY*

U.S. Airlines See Revenue Strength Even as Fuel Cost Rises - Business Travel News

Extract: “…several airline senior executives during Tuesday's J.P. Morgan Industrials Conference expressed confidence in business travel's recovery through 2022 and beyond. Carriers that updated capacity and revenue guidance Tuesday in filings with the U.S. Securities and Exchange Commission include American Airlines, Delta Air Lines, United Airlines and Southwest Airlines. “

Cineworld Boss Mooky Greidinger Optimistic For A “New Normal”, Talks Ticket Prices, Reducing Debt & More - Deadline

“…once business goes back to normal, of course the first priority is to deal with the debt.”

Comment from Cineworld CEO echoes that of Adam Aron of AMC from earlier this year, which is much further ahead in its journey of debt reduction.

Seaspan forward fixes contracts for 18 containerships - PRnewswire

Seaspan, a wholly-owned subsidiary of Atlas Corp. ("Atlas") (NYSE: ATCO), today announced that it has entered into an agreement with a major European liner customer to forward fix contracts, extending current charter terms for 18 containerships

*CREDIT TRADING*

Bloomberg launches all-to-all bond trading service with help of GS - FI-Desk

Extract: “Bloomberg has launched Bloomberg Bridge, a new global all-to-all service that supports intermediated trading for corporate and emerging market bonds. Clients will be able to launch request for quote (RFQ) tickets for applicable securities or respond to an RFQ to execute a trade, supported by dedicated Goldman Sachs intermediation desks.”

Russia’s Corporate Debt Trading Soars as Sanctions Fail to Deter - BBG

Extract: “The average daily trading volume for dollar-denominated Russian corporate bonds rose to a level last seen in March 2020. The average trading volume for this month, as of March 14, was $258 million, compared with $96 million in the same month last year, according to data from MarketAxess.”

*RATINGS*

Kraft Heinz was upgraded to BBB- from BB+ with a positive outlook by S&P Global

Unifin Financiera downgraded to B+ from BB- by S&P

*LINKS*

The man, Charlie Bilello on Inflation and the Fed balance sheet

Ferro / Citi on Fed BS reduction

Negative yielding bonds update:

US slow down → recession ahead?

The “R” word again