Weekly Global Credit Wrap for w/e 1 April 2022

Some subtle moves going on beneath the surface...

*OVERVIEW*

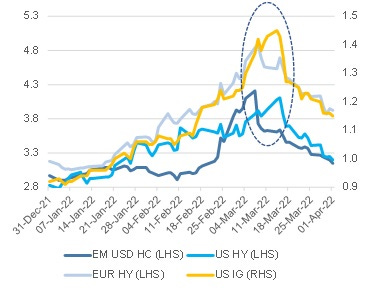

Credit spreads

Credit spreads came off the intra-month highs (chart below) for the major credit subsectors in March. It will be interesting to see how spreads move going forward as the market contends with the impact of the Russia/Ukraine conflict vs the cocktail of slowing growth, high inflation and faster fed hikes/BS tapering.

Bond ETFs - Most Bond ETFs had a good week (closing 1 Apr) with TLT (+2.2%), EMLC (+1.5%), EMB (+1.3%), LQD (+1.2%) and AT1(+1.0%) all posting 5 day returns of more than 1%.

Single names /sectors - Pockets of strength were noticeable in subtle areas likes Sterling Sub Financials and select EM Sovereigns. For example, Egypt bonds have largely recovered their losses incurred in the aftermath of the Ukraine/Russia crisis. There has been strength in other battered MENA nations like Ghana and Pakistan paper but not to the same extent. Reasons for the strength in these pockets are wide ranging (light dealer positioning for a rally/month end, re-appraisal of Russia/Ukraine impact on other nations, lower primary issuance). Within US IG, I note that Kraft’s upgrade to a benchmark IG rating saw it add to nearly $20bn of “rising stars” in March 2022.

Funding Markets - Continue to thaw. This week saw two more AT1s get issued in the financials space (Rabo/DB). Leveraged loans started to show signs of life with a new deal for Barentz. Istanbul Metro announced a possible new issue in EM next week.

Behavioural aspects- The financial press/fintwit is full of headlines about “record losses” in bond markets in Q1 2022, mainly referring to losses in Government bond markets and IG rated bonds, predominantly due to the sell-off in rates. How will market participants react to these headlines - maintain current allocation, reduce or add to fixed income?

*MACRO*

U.S. government bonds just suffered their worst quarter of the past half century - MarketWatch

Extract: “U.S. government bonds lost 5.6% in the first quarter, the worst showing since record-keeping began in 1973, according to the Bloomberg U.S. Treasury Total Return Index. “

*NEW ISSUES/TENDERS*

March US IG credit issuance totaled $230bn - BBG

European primary issuance closed out 1Q with more than €513b of sales - BBG

…passing the half-trillion milestone about a week slower than in 2021

Europe’s Leveraged Loan Market Reopens After Monthlong Pause - BBG

Barentz kick starts junk grade issuance with $110m add-on

Europe’s high-yield bond market has been shut since Feb. 10

Cemex announced a Tender offer for 29s/30s/31s $ bonds

Minerva (Brazilian Beef firm) - Repurchase & Cancellation Bonds 2028 and 2031 - Link

AIG Announces Cash Tender Offers for Certain Outstanding Notes - Yahoo Finance

Glencore refinanced its committed s/t RCFs - Glencore

*Commodities/Inflation*

Siccar Point and Shell handed extension to Cambo licences - Energy Voice

Siccar Point Energy and Shell have been granted a two-year extension to the licences for the Cambo oil field, paving a potential future for the project.

Britons turn to own label food and discounters as inflation bites - Kantar via RTRS

*IG*

Global Corporate Bonds Lost $1 Trillion, and Risks Are Rising - BBG

London School of Economics Raises $230 Million in Private Debt -BBG

The proceeds, earmarked for green and social projects, will help fund a net-zero carbon building development, energy efficiency across its existing premises, as well as scholarships and post-graduate study, according to a university spokesperson.

Aercap intends to vigorously pursue insurance claims with insurers - ITIJ

*HY*

US HY funds had an inflow of $853m at Tuesday’s close, after 11-weeks of outflows

The European Credit Market Is Stirring Back to Life - BBG via WaPo

Extracts:

“It’s been a rocky quarter, but the European credit market is dusting itself off and getting back to work.”

“…investor demand is reemerging at these more attractive spread levels”

“…activity is also resuming in the European leveraged loan market, which was similarly shuttered in recent weeks. Barentz International BV, a single B-rated specialty chemicals distributor, raised 100 million euros on Thursday to finance an acquisition in life sciences.”

European Central Bank urges banks to eye increasing 'risk' in leveraged lending - S&P Global

Avis increased its Tranche C term loan by $250M to $750M - Filing

Note that recently another US HY issuer; American Axle recently upsized a Term Loan A Facility with a lender in order to redeem a portion of its 6.25% 2026 bonds. Even though these are only two transactions, it demonstrates how HY issuers are utilizing different avenues outside of public bond markets to raise financing.

Ithaca Energy Q4 Highlights (North Sea firm):

Unit operating costs of $18/boe

EBITDAX of $1,036 million including realised gains of $115 million on the commodity hedging instruments that were reset in 2020

$275 million was repaid against the Reserves Based Lending facility during Q4 taking net debt down to $930 million

22 million boe (73% oil) hedged from Q1 2022 into 2023 at an average price floor of $61/bbl oil and 92p/therm gas

Atlas Corp held an investor day (parent of Seaspan Corp) - Link

*CHINA*

China Weighs Raising Billions to Rescue Troubled Financial Firms - BBG

China property developer CIFI to issue $250 mln convertible bonds - RTRS

Extract: “Chinese property developer CIFI Holdings (Group) Co Ltd said on Friday it will issue HK$1.96 billion ($250.22 million) three-year convertible bonds for refinancing a bond maturing this month.”

This follows Country Garden, who also issued a convertible during Jan-2022.

Country Garden Bags Over $6bn Facility from Agricultural Bank of China - Tradingview

Extract: “Property developer Country Garden Holdings secured a 40 billion yuan ($6.28 billion) facility from the Guangdong branch of Agricultural Bank of China as part of the parties' strategic partnership, according to a late Friday filing.

Under the deal, the lender will offer comprehensive financial services to Country Garden for property merger and acquisition, as well as affordable rental housing and personal housing mortgage loan businesses.”

Deleveraging Progress Key to Supporting Sino-Ocean’s Ratings - Fitch

*COMMODITIES/INFLATION*

Venezuela's PDVSA seeks oil tankers in anticipation of U.S. sanctions easing - RTRS

PDVSA is in talks to buy and lease several oil tankers amid a possible expansion in exports, according to three sources and a document seen by Reuters, a sign the country expects U.S. sanctions on its petroleum sector to be eased.

Europe's appetite for U.S. gas fast-tracks two new LNG projects - RTRS

France is looking to build a new floating LNG import terminal in Le Havre

*FINANCIALS*

A couple of AT1s were priced this week:

Rabobank raised € 1bn PerpNC7.25 AT1 bond at 4.875%.

Deutsche Bank priced a new € NC7 AT1 at 6.75%

Both deals tightened in from Initial Pricing Talk and the Deutsche deal saw orders of €5.7bn (7.6x covered).

*EM*

Egypt, Qatar sign $5 billion in investment deals - RTRS

Colombia’s central bank's MPC raised its policy rate by 100bp to 5.00%

Pakistan’s fx reserves hit the lowest level since end of FY 2020-2021 as the country repaid external debt - TheNews

IMF to start talks with Sri Lanka on loan request in coming days - RTRS

Economists in Sri Lanka suggest immediate solutions to FX crisis

*RUSSIA/UKRAINE*

Vontobel EM Strategist sets out Russia/Ukraine conflict scenarios for different debt stakeholders - Vontobel

Russia Offers to Repurchase 2022 Eurobonds Paying in Rubles

Polyus confirms repayment of Eurobond due 28 March 2022 - Polyus

*F.I TRADING*

Jefferies reported quarterly earnings

Comments on bond trading:

“Fixed Income net revenues were lower, primarily due to lower trading volumes in the face of inflation concerns and interest rate uncertainty.”

“Fixed Income results were impacted by lower trading volumes in the face of inflation concerns and interest rate uncertainty.”

Note that JPM, who tends to kick off the bulge bracket bank reporting season reports Q1 2022 on 13 April 2022.

*RATINGS*

Fitch Rates Istanbul's Upcoming USD Bond 'B+(EXP)' - Fitch

The proposed USD305 million fixed-rate bond will have a tenor of five years. The proceeds will be used to finance two of Istanbul's metro projects.

Turkey Downgraded to B+ by S&P

Moody's upgrades five Greek banks and maintains positive outlook - Link

Barrick Gold Upgraded to BBB+ by S&P, Outlook Stable

Fitch Affirms Australia and New Zealand Banking Group at 'A+'; Outlook Stable

Fitch Affirms Commonwealth Bank of Australia at 'A+'; Outlook Stable

Fitch Affirms National Australia Bank at 'A+'; Outlook Stable

Fitch Affirms Westpac Banking Corporation at A+; Outlook Stable

Vinci Affirmed at A- by S&P

GNB Sudameris (Colombian Bank): Moody's affirm the ratings of the company and parent holdco Gilex Holding

Fitch Affirms Investec Bank plc at 'BBB+'; Stable Outlook

S&P UPGRADES EQT TO 'BBB-'; OUTLOOK STABLE; RAISES DEBT RATING

South Africa’s Credit Outlook Raised to Stable by Moody’s

Republic of Congo Affirmed at CCC by Fitch

X-S&PGR Upgrades Oman To 'BB-' From 'B+'; Outlook Stable

Republic of Poland Affirmed at A- by S&P

S&P UPGRADES SAIPEM TO 'BB' FROM 'BB-'; OUTLOOK POSITIVE

Marfrig Global Foods was upgraded to BB+ from BB by S&P

Sony’s Credit Rating Upgraded by S&P as Profits Rise

*LINKS*

JPM’s Guide to the Markets for Q2 2022 - JPM

Rishi Misra on yield curve inversion

Re-Org Research Podcast on EMEA Primary Market; Double-B Bond Trends

One helluva chart…

Strength of the US consumer (?)

Oh…

Less deals mean less LBOs?

New US CLO issuance in 2022

Nice chart from US Housing Guru Logan (orig from GS/Haver):

I’ll be taking a break for a few weeks. See you on the other side of Easter.

Nice content! Thanks for sharing :)