Weekly Global Credit wrap for the w/e 25 March 2022

Only one story really...higher short end rates

*OVERVIEW*

Summary on fixed income markets: Significantly higher issuance this week (€65bn in Europe alone) compared to the early days of the Russian invasion. Note that MTD issuance in US IG is nearing $200bn…no small feat in such volatile conditions. Financials are seeing more activity (tenders/calls/new issuance) and that has spread down the capital structure to LT2 and AT1 issuance. Within EM you are seeing seasoned EM Sovereign borrowers come to market (Philippines, Indonesia). Meanwhile European HY pipeline is still warming up and the US HY market posted the slowest issuance month in two years.

The credit market is merely a sideshow compared to what is happening in the short end of the US rates curve. The 2s10s spread is nearing an inversion, which historically has signaled an upcoming recession in the US. All eyes are on how the Fed navigates the task of bringing down inflation while not crashing the economy. A WSJ article citing J Powell’s comments outside of a Fed Meeting showed a high level of candour, which could give a more useful insight into the trajectory of rates/fed thinking. Meanwhile, a number of other Fed voters are talking up the 50bps hike at the next meeting while a US Bank is calling of 50bps hikes at each of the next four meetings! “50 Sent!” as one clever HY strategist said in their report this week.

Rates - Some massive moves going on especially in the front end. The 2 year UST has gone out nearly 90bps this month to 2.3% and the 3 year has gone out to 2.5% which is +92bps.

This has seen the 2s10s spread collapse to circa 20bps. This has led many market commentators to talk about the increasing possibility of a recession. Principal Global's analysis on this topic showed that the U.S. Treasury yield curve has inverted ahead of every U.S. recession since the 1950s. Note that the 3s10s and the 5s10s have already inverted.

In terms of other notable levels across Global Bond Markets:

French OAT 10 year now through 1.0%

German 3 year is now positive.

Italy 10 year is through 2.0%

Aussie 30 year is through 3.0%

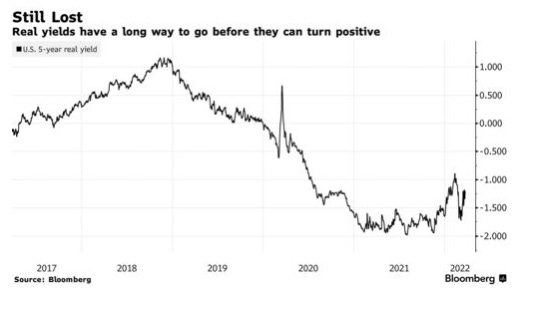

Meanwhile, real rates are still negative

Cash credit moves:

US IG 4bps tighter at +123

EUR HY 25bps tighter at +416bps

US HY 17bps tighter at +352

CoCos 10bps tighter at +381

Bond ETFs:

TLT -3.9% WTD and now down 13% YTD

IGLT down 1.7% WTD and now down 8% YTD

FLOT is flat this week and is down only -0.41% (floating rate bond ETF)

Within IG; LQD and VCIT were down 2.4% and 2.2%, LQD is nearing on a 10% YTD loss. Even some medium dated bond ETFs remain technically oversold, e.g. SLQD which had an RSI of 25 at the end of the week.

Within higher beta bond ETFs, EMB lost 2.1% and is down 11.76% YTD. JNK and HYG both down -1.3% in the week.

*MACRO*

Powell Says Fed Will Consider More-Aggressive Interest-Rate Increases to Reduce Inflation - WSJ

Bringing down inflation and avoiding recession will be ‘challenging task,’ says central bank leader. This article was useful in that J Powell appeared to speak more candidly than he does during regular Fed Meetings.

Creditsights Head sees silver lining in bond rout - BBG Video

Wini Cisar talks about how higher yields should be viewed positively.

Short duration investment-grade funds saw inflows for the first time since January, according to Barclays.

ECB would reconsider plans to end QE this summer in case of “deep recession”: ECB's Schnabel

German fiscal policy to stave off stagflation, finance minister says - RTRS

The German government will tailor its public spending plans to avoid stagflation in Europe's biggest economy and keep at bay the risk of sliding into a cycle of rising prices and anemic growth, Finance Minister Christian Lindner said on Tuesday.

Norges Bank raised its policy rate to 0.75%, further hikes expected

US Inventory of New Houses Piles Up to Highest since 2008 - Wolf Street

Extract: “The inventory of new single-family houses for sale rose to 407,000 houses in February (seasonally adjusted), the largest unsold inventory since August 2008, up by 40% from a year ago.

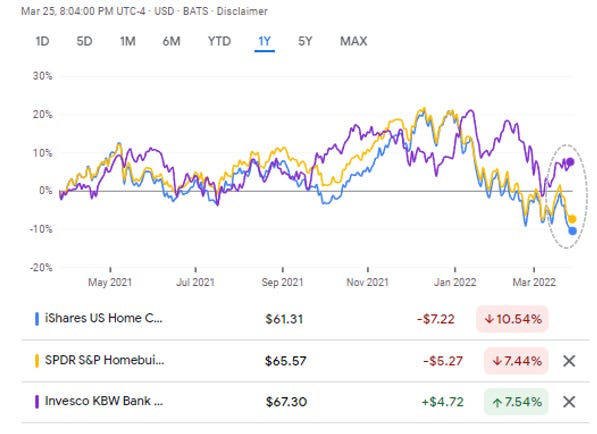

Homebuilders/Construction vs Bank ETFs - Diverging fortunes on higher rates

Banks ETF ($KBWB) starting to decouple from US Homebuilders ($XHB) and US Home Construction ($ITB) ETFs

*NEW ISSUES / FUNDING MKTS*

Bayer Issues $1.4 Billion New Corporate Hybrid Bonds in Two-Tranche Deal

Mercuria secured emergency credit facility - BBG

Swiss trader Mercuria Energy Group Ltd. secured a $2 bn emergency credit facility from banks as commodities prices surge following Russia’s invasion of Ukraine. The facility, secured earlier this month, can be renewed or closed in six months time, people familiar said.

Trafigura Group Pte Ltd closes JPY93.75 billion Japanese term loan facility

Trafigura refinanced its Japanese term loan credit facility totalling JPY93.75 bn (equivalent USD790m at current exchange rate). The Samurai loan was increased by JPY16.95 bn (equivalent USD140m at current exchange rate), from the 2020 Samurai loan. Trafigura Website

El Salvador postponed the debut issuance of its public tokenized dollar bond named “Volcano Bonds”

*COMMODITIES / INFLATION*

U.K. inflation surged to a new 30-year high of 6.2% in February. Consensus was for 6%.

Jamie Dimon pushes Biden for domestic energy "Marshall Plan" - Axios

Top trading houses speak at FT commodities conference - RTRS

Traders warn of looming global diesel shortage - Irish Times

“The heads of three of the largest commodity traders – Vitol, Gunvor and Trafigura – estimated that as much as 3 million barrels of oil and its products a day could be lost from Russia as a result of sanctions, following the country’s invasion of Ukraine. “Europe imports about half of its diesel from Russia and about half of its diesel from the Middle East,” said Russell Hardy, chief of Switzerland-based oil trader Vitol. “That systemic shortfall of diesel is there.””

Qatar Investment Authority sold £790m of Glencore shares in Europe's largest block trade in the year to date

Louis Dreyfus reported 2021 figures

Highlights:

Net Sales of US$49.6 billion, up 47.7% versus 2020

EBITDA of US$1,623 million, up 22.6% compared to 2020

Adjusted Leverage Ratio at 0.9x (1.8x as of December 31,2020)

Adjusted Net Gearing at 0.27 (0.48 as of December 31,2020)

Liquidity Coverage of 2.2x current portion of debt (1.8x as of December 31, 2020)

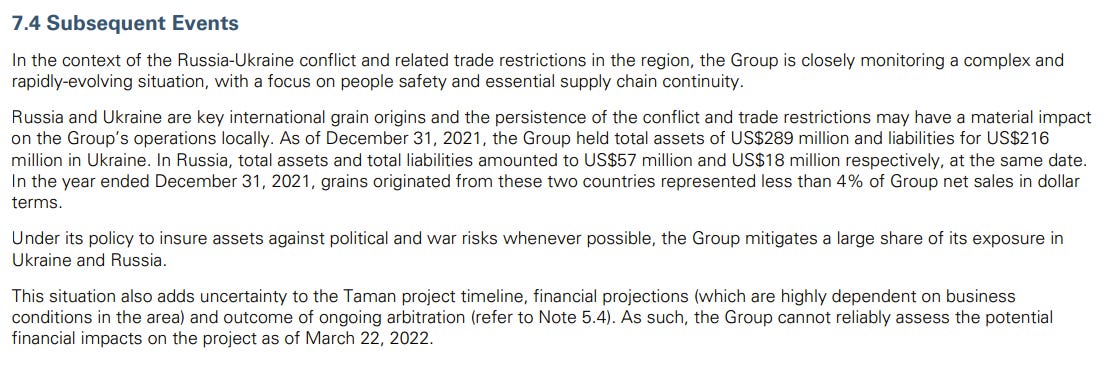

Regarding 2022’s events, there was a note in the subsequent events note of the report and accounts:

Chinese steel output is down as ~ 19 blast furnaces halt production due to Covid restrictions: Mysteel

Steel price in the EU hit a new record high this week

Russian Aluminum Supply Squeeze Tightens After Australia Ban

US plans to supply the EU with up to 15 bn cubic meters of LNG by end of this year: FT

Italy Approves $4.9 Bn Package to Curb Energy Prices

Germany coalition reaches deal on energy relief package.

Ruling German coalition parties have agreed on “extensive and determined measures to relieve the burden on citizens and to strengthen energy policy independence,” DPA reports.

Shell is planning to invest £20-25bn in the UK energy system over the next decade says Company's chairman

Shell reconsiders decision to divest from Cambo North Sea field: Upstream

The field is operated by Siccar Point and faced resistance from environmentalists previously.

Spain pledges $550m of aid to end Truckers protest

*HY / CONVERTS*

US HY - Lipper reported a weekly $2.7bn outflow

…which was the 11th consecutive weekly outflow, which took ytd outflows in US HY to over $20bn.

Yum Brands, owner of a number of well known fast food outlets (KFC/Pizza Hut) issued $1bn of 10 year notes after initially pitching a $500m deal

On the topic of upsizings, Hertz upsized its Rental Car ABS deal to $1.4bn from $1.1bn.

A number of HY issuers redeeming existing bonds (partially or fully):

American Axle

Cleveland Cliffs

Occidental

Peabody

Norwegian Air Shuttle is contemplating a buy-back of the zero-coupon senior unsecured 2026 bonds - Norwegian

Ford Motor Credit raised a $1bn 4NC3 bond at a yield of 4.95%.

Saipem approves € 2bn capital increase, with support from Eni and CDP

Energean (Israeli Gas Firm) reported FY figs - Link

Revenues of $497m ($336m 2020 pro forma) and Adjusted EBITDAX of $212m ($108m 2020 pro forma), representing record full year results and the transition to net operating profit.

First gas from Karish field in Q3 2022

First gas from the first well at NEA/NI (Egypt) expected in H2 2022

Increased weighted average debt maturity to six years, pushed out the first major repayment until 2024 and achieved blended fixed rate of 5.5%, removing exposure to floating rates

Post first gas from Karish, the Company expects a rapid deleveraging on a Group consolidated basis to levels below 1.5x (Net Debt/EBITDAX) and sees this being met no later than 2024.

Year end liquidity position in excess of $1 billion

In December 2021, Energean received a funding package from the Greek State and also from the Black Sea Trade and Development Bank

EnQuest (North Sea oil firm) reported FY Figs and debt reduction

Key Highlights:

Adjusted EBITDA +35% to $723m and PBT of $352.4m.

Co is targeting progress towards a net debt to adjusted EBITDA ratio of 0.5x.

As at 28 February 2022, net debt was $1,090.0 m, down a further $132.0 m from 31 Dec 2021

Net debt/adjusted EBITDA of 1.6x (2.3x in PY)

Post y/e, group had made further early voluntary repayments of its RBL facility totalling $85.3 million, with the amount drawn down reduced to $329.7 million

EnQ continues to explore options to refinance its Retail and High Yield Bonds ahead of maturity in October 2023. EnQuest 2023 $ bonds moved above par for the first time ever.

Waldorf Production Limited (North Sea) has acquired the UK subsidiary of MOL for $305m plus earn-out

Just Eat Takeaway.com Secures New Agreement With McDonald's to Drive Delivery Growth - PYMNTS.COM

“Just Eat Takeaway, Europe’s largest meal ordering service, has signed a long-term strategic partnership with McDonald’s to expand delivery. “This partnership will elevate existing local partnerships between Just Eat Takeaway.com and McDonalds, which will reduce complexity and provide great opportunity to innovate at scale together on operational efficiency and a seamless customer experience,” the Dutch company said on its website Tuesday (March 22).

McDonald’s has offered delivery through its McDelivery program for the last five years, with the service expanding from 3,000 locations at launch to more than 33,000 restaurants in 300 countries today, Just Eat Takeaway said.”

*FINANCIALS*

ECB to tighten banks' access to loans after pandemic-era largesse - RTRS

The European Central Bank will tighten banks' access to its liquidity from July by phasing out exceptionally easy collateral rules introduced at the onset of the coronavirus pandemic, the ECB said on Thursday.

HSBC issued its first T2 bond since 2016

HSBC 4.762 33 priced at +240bps

Sabadell issued a call notice on its AT1

Sabadell 6.5% AT1 . The redemption date is on the 18th May

Intesa re-opened the European AT1 market

Intesa issued €1bn 6.375% PerpNC6 AT1. Intesa issued in to a market that continues to see a number of AT1s being redeemed.

A number of financials look to tender/repurchase debt, demonstrating confidence in their liquidity/capital positions

Standard Chartered raised $1.5bn two-part offering of Fixed and Floating notes:

$1bn 4NC3 bond at a yield of 3.971%

$500m 4NC3 FRN at a yield of 2.02%

Fitch on Planes Grounded in Russia and impact on Insurers/Reinsurers - In worst case scenario, agency believe most insurers and reinsurers would only suffer a hit to earnings rather than a capital depletion. Fitch

*CHINA*

Mortgage rates are going down in cities in China

Wuhan, the capital city of Hubei province, cuts the mortgage rate for first-home purchase by 43 bps to 5.2% from 5.63%, second-home by 48 bps to 5.4% from 5.88%.

Local real-estate agencies confirmed that Xiangyang, Shiyan, two fourth-tier cities in Hubei province, has cut the mortgage rate by 40 to 45 bp.

Source: @Sino_Market

Evergrande set a target of end-July 2022 to reveal its debt restructuring proposal to creditors - RTRS

Evergrande’s bondholders have threatened to sue the developer on being blindsided …by a US$ 2bn lenders' claim on its subsidiary that was previously not disclosed - Holders are said to include Saba Capital, Redwood Capital Management and Ashmore BBG/Irish Times

CIFI Board Directors to Buy up to 30m Yuan of Co. Local Bonds

China’s Harbin Eases Real Estate Policies After House Prices Fall for Seven Months - Yicai Global

China Property - A number of Auditors resigning and audits delayed according to WSJ

Extract: “Since December, auditors at Hopson Development Holdings Ltd., China Aoyuan Group Ltd., Sinic Holdings Group Co., Yuzhou Group Holdings Co. and Shimao Group Holdings Ltd.’s onshore unit have also resigned.”

*UKRAINE/RUSSIA*

EU to propose using a € 500m agricultural crisis fund for the first time to aid Ukrainian farmers

Poland will extend a swap line of as much as US$ 1bn to Ukraine

MHP launches consent solicitation with bond investors as its going to miss a coupon payment Link

Rubles for gas: Putin trolls the West over its energy addiction - Axios

“By announcing on Wednesday that so-called unfriendly countries — a list including EU countries and the United States — will have to pay for Russian gas imports in rubles, the Russian president is challenging Western efforts to punish Moscow for invading Ukraine while carving out crucial Russian energy imports from sanctions. "I made the decision to implement within the shortest possible time the package of measures to transfer payments — we will start with that — for our natural gas supplied to the so-called ‘unfriendly’ states to Russian rubles," Putin said.”

*EM/ASIA*

Egypt issues $493mln samurai bonds on Japanese market: finance ministry - Zaywa

Asian IG sovs issued bonds this week - Indonesia and Philippines

Indonesia tendered for some short dated bonds as a part of the process.

Philippines details:

$500m 5y bond at 3.229%;

$750m 10.5y bond at 3.556% and

$1bn 25y sustainability bond at 4.2%.

Bonds are rated Baaa2/BBB+/BBB with orders said to be over US$ 8bn. Due to the flatness of the UST curve, the difference in yields between the 5 year and the 10.5 year was only 32bps.

Vedanta Resources Chairman Anil Agarwal confident of reducing debt by $4 billion in 3 years - MoneyControl

Anil Agarwal…believes that the higher dividend from its Indian unit Vedanta Limited will aid the UK-based mining and metals conglomerate to significantly pay its debt obligations. ''Vedanta Limited is likely to pay out a dividend of approximately $2 billion. We are confident of reducing debt at Vedanta Resources by over $4 billion by three years,''

Rate hikes this week in EM:

Argentina Raises Key Rate to 44.5%

Bank of Ghana hikes prime interest rate to 17%

Banxico (Mexico) - MPC were unanimous in hiking the policy rate by +50bp to 6.50%

GM buys SoftBank Vision Fund's stake in Cruise for $2.1 bln

Softbank- +$1.1bn upsize of private credit loan from Apollo - BBG

Loan is secured on holdings of Softbank Vision Fund according to sources and increases total borrowed under this loan to $5bn, which is said to be the largest of its kind in the private credit market..

*RATINGS*

X-S&PGR Upgrades Stellantis N.V. To 'BBB/A-2'; Outlook Stable

Sunac was downgraded three notches to Caa1 from B1 with a negative outlook

Peru: S&P downgraded the country from BBB+ to BBB citing political issues

Saudi Arabia Outlook to Positive by S&P Amid Higher Oil

*COVID19*

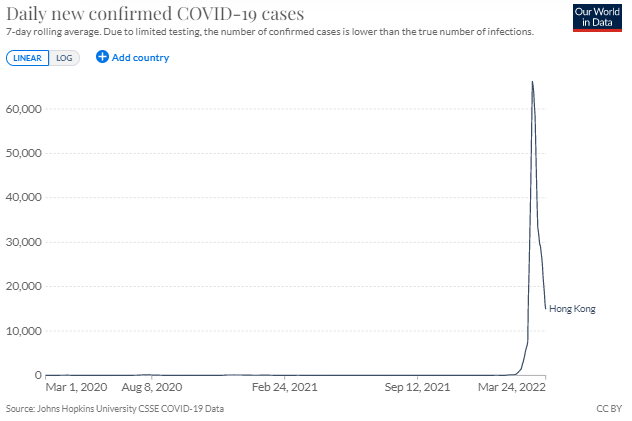

Hong Kong Loosens Restrictions on Inbound Travelers

Some of the changes include; hotel quarantine period for fully vaccinated returning residents to be relaxed from 21 or 14 days to 7. Flight bans on nine countries will also be lifted from 1 April.

COVID - BA.2 wave incoming?

*LINKS*

Howard Marks latest Memo talks Geopolitics

Negative yielding debt update

C Strategist explaining his forecast of 50bp hikes at the next four meetings

Bond market history lesson from Bofa/JF

2 YR UST Focus

Income squeeze in the US…but the squeeze in parts of EM are likely much worse

US Housing - It will be different this time…(?)