Weekly Global Credit Wrap 30 September

Credit risk rising, recessionary corporate earnings signals, innovative ESG financings...

Immense week for Fixed Income markets as historic volatility in the UK Gilt market focuses minds on what else could “break” in Global Markets and how other Central Banks (looking at you J Powell!) could react. In the FX market, both the BoJ and the PBOC intervened in the currency markets this week, adding to BoE’s intervention in Gilt Market. Ad-hoc CB involvement seems to be picking up as market volatility rises. Corporate earnings and guidance from a number of large companies continues to paint a picture of a slowing global economy which could alter the market’s focus from inflation to recession…

MACRO:

Corporate earnings across a range of sectors suggest slowing economy

Big Tech keeps cutting jobs - Meta to cut headcount for first time

Oil set for first quarterly drop since 2020

Anecdata - “Mom and pop” investors in the US loading up on 2yr Treasuries

CORPORATES / CREDIT:

$LQD ETF gone below pandemic era lows

US IG cash spreads broke to new highs of +164bps this week

US IG Bond Funds posted 3rd largest weekly outflow on record

CDS indices at heightened levels:

Europe Itraxx Main @ 135 (highest since euro debt crisis in 2012)

European Xover nearing pandemic wides

Weakness in subordinated perps (e.g. AT1/Corporate Hybrids) as judged by moves in AT1 and EHYB Bond ETFs

Tenders/buybacks - Softbank announces bond tender

Trading - Jefferies announces slowdown in FICC trading, other large US Banks to report Q3s on 14/17 October

INFLATION

European inflation figs still posting double digit increases (EU and Germany data)

Wage inflation - Amazon raises pay in the US

HY

US HY Q3 bond issuance lowest Q3 total since 2008

Bleak update from Carnival sends shares to lowest since 1992

Cineplex proposes merger with Regal Cinemas (owned by Cineworld)

U.S. Lev Loan Default Forecast Raised to 2-3%; 2024 Projected at 3-4% - Fitch

ESG

Barbados issues $146.5m blue finance loan

IMF suggests Bahamas use carbon credits to pay off debt

ESG laggard Pemex looks at $1bn ESG Financing...

*MOVES OVER 5D*

CDS Indices - CDX HY widened to 610bps which was +42bps over the week and the largest move amongst the main indices, although some of this might have been due to the roll (Editor: CDS experts feel free to comment). CDX EM, EUR SUB Fins widened 13bps each. Itraxx main traded at the highest since 2012 and the euro debt crisis and Xover (closed at 641) is nearing the highs (over 700bps) seen during the worst of the pandemic.

Cash Credit spreads - The largest mover I track is the Global CoCo Banking OAS which widened +67bps to 557bps. The main driver was UK AT1s which have weakened with the intense volatility in the Gilt Market. EM HY and EUR HY widened 65 and 63bps respectively. US HY Corp spreads remain above 500 (552bps). US, European and Sterling IG all widened meaningfully with GBP cash moving out the most. US IG cash spreads broke to new highs of +164bps this week, which makes this interesting from an all in yield perspective since Treasury Yields have risen a whole lot more from the last high in 2022 hit at the end of June.

Bond ETFs - Consistent with the move in cash credit, AT1 Bond ETF was the biggest loser amongst the ETFs I track losing 2.8% on the week. This was followed by EHYB (Euro Corporate Hybrids) losing 1.34%. So there was some shared weakness in subordinated perpetual instruments this week presumably largely driven by the volatility in the UK which is the “country of risk” for a fair share of perps.

TLT is closing in on the 100 price mark as it looks to continue its downtrend (30 year UST closed at 3.776%, failing to hold the 4.0% level so far). Other weak performers include BKLN (Senior loans) and TIPS which lost 0.9% on the week. UK Gilts closed the week strongly with IGLT and Vanguard UK long Duration Gilt ETF posting gains of +4.3% and 11.0% over 5 days. HYG, AGG, JNK, IUSB, BSV were all positive over the last 5 days..

*MACRO*

US IG Bond Funds posted 3rd largest outflow on record

$10.3bn was this week’s outflow from IG. US HY saw $3bn out of the door after seeing $1.66bn out the previous week. This was likely a contributing factor to the chronic lack of issuance this week in Credit Markets.

Bellwether corporate earnings/updates were less than stellar this week..

There were weak reports from different corners of consumer focused businesses this week. Apple, Carnival, Nike, Next Plc (UK Clothes retailer), CarMax (Used cars), Micron (chips) updates were all met with disappointment. This is despite some firms like Nike beating expectations for the quarter, however forward guidance on margins and inventory disappointed here. The news weighed on broader credit spreads as market participants project weakness into the upcoming Q3 earnings.

Cost cuts including job cuts keep coming in big Tech..

Meta Platforms announced it is to cut headcount for the first time:

“I had hoped the economy would have more clearly stabilized by now,” Zuckerberg explained. “But from what we’re seeing it doesn’t yet seem like it has, so we want to plan somewhat conservatively.” Zuckerberg added that the hiring freeze is necessary as leaders within Meta want to ensure they don’t hire people to teams where they don’t expect to have positions next year.

Softbank Vision Fund to reduce at least 30% of workforce (150 people) - Techcrunch

Chamath and the besties go through the slowing of tech hiring in their all-in podcast this week, quite a good listen from guys who are stalwarts of Silicon Valley. E98: Big tech starts making cuts, Fed incompetency, global debt, Russia/Ukraine & more - All in Podcast.

ECB’s Lagarde says rates will be lifted at next ‘several’ meetings - BBG

ECB President Christine Lagarde said borrowing costs will be raised at the next “several meetings” to ensure inflation expectations remain anchored and price gains return to the target. “We will do what we have to do, which is to continue hiking interest rates in the next several meetings,” she said. “Our primary goal is not to create a recession. Our primary objective is price stability and we have to deliver on that. If we were not delivering, it would hurt the economy far more.”

While the UK is cutting taxes, Spain introduces a wealth tax

Extract of Al Jazeera: Spain’s Socialist-led coalition government has said that residents whose wealth exceeds 3 million euros ($2.9m) will be subject to a new asset tax in 2023 and 2024. Finance Minister María Jesús Montero on Thursday described the temporary wealth tax, which she said will affect 23,000 people, or 0.1 percent of taxpayers, as one of “solidarity”.

Oil set for first quarterly drop since 2020

*INFLATION*

Euro area flash estimate of Sept inflation @ 10.0% (vs 9.7% consensus)

Euro area annual inflation is expected to be 10.0% in September 2022, up from 9.1% in August according to a flash estimate from Eurostat, the statistical office of the European Union.

See here for more detail.

Germany Sept. CPI in its most populous state jumped above 10%

(Reuters) – German inflation likely grew significantly in September based on initial data from its most populous state, which saw the biggest jump since the early 1950s, according to its statistics office. The state of North Rhine Westphalia saw inflation rise 10.1% year-on-year in September, mainly due to higher costs for goods and services after a cheaper transport ticket and fuel tax cut expired at the end of August.

Japan joins other nations in establishing “inflation reduction programs”

Japanese Prime Minister Fumio Kishida instructed the government Friday to come up with an economic stimulus package by the end of October to help mitigate the impact of inflation, as economists warned against over-sized spending. Yahoo Finance

Wage inflation this week

Amazon.com announced a pay increase for hourly workers in the US that it says will take average starting wage for most front-line employees in warehousing and transportation to more than $19 an hour - WSJ

Carmarkers in Spain to increase wages by as much as 10%: Expansion

Effects of inflation and waning consumer confidence..

*NEW ISSUES/TENDERS*

Softbank announced a tender offer for certain bonds including Hybrids

The move helped lift the Softbank curve in a risk off week for Hybrids. It was also yet another Corporate Hybrid issuer tendering its debt early joining others like Heimstaden Bostad AB, American Movil and KPN.

American Movil sent call notice out on remaining €62.6m of its EUR 6.375% 2073 issue

This was after it had tendered €487.3mm of it at 104.0 earlier on in the month. The expected call date on the bond was September 2023 but it was likely redeemed early through a clean-up call clause that can often be found in Corporate Hybrid docs.

Cemex early tender results - Indicates $468m of bonds to be accepted for tender

2029/2030/2031 USD notes.

DNO completes another bond buyback of 2024 bonds ($19.6m) - Statement

Norwegian Oil firm with major interests in Kurdistan reduces debt further by buying bonds in the market.

*IG*

Cost of refinancing euro high-grade debt at 250 basis points, new record - BBG

The difference corporates need to pay if they sold bonds now compared to the coupons on their existing debt climbed to 250 basis points, the highest since a Bloomberg index of euro-denominated investment-grade bonds began in 1998.

In other words, companies have to pay an additional 2.5 million euros for every 100 million euros that they borrow.

Toyota's global vehicle output rises by record 44.3% in August - JT

Toyota Motor said on Thursday its global vehicle production grew at a record pace for the month of August, as the sector recovered from the COVID-19 pandemic and production capacity increased, mainly overseas. The announcement offers a bit of relief for the Japanese automaker, which has been under scrutiny over whether it can stick to its annual production target of 9.7 million vehicles, even as China dials back pandemic restrictions and chip shortages are showing some signs of easing.

*HY*

Fitch: 2023 U.S. Lev Loan Default Forecast Raised to 2.0%-3.0%; 2024 Projected at 3.0%-4.0%

Cruiselines - Carnival profit warning, sends shares and rest of sector lower

The week ended with Carnival’s shares hitting the lowest since 1992 (and closed down 23%) due to an update which showed that its 4q bookings were below the historical range at at lower prices due to the use of travel credits. Earlier on in the week - UK listed Saga Plc which has a cruise division also saw its shares dive (closed down 36% on the week). The weakness there didn’t appear to be specific to the cruiselines but its PBT forecast was guided lower.

US Cruiseliners have been some of the heaviest users of the public debt market since the pandemic, last week I highlighted that RCL had come to market 3 times already this year. If the consumer is going to be continued to be pressured by high inflation and high mortgage rates, the capacity to spend on expensive cruises is likely to diminish. This could have implications for leverage levels as debt levels remain high and EBITDA becomes pressured. Note that there has already been some restructuring activity in the sector with Norwegian operator Hurtigruten appointing advisors in early September to address its 2023 maturities.

Cineplex Seeks to Revive Regal Merger After Cineworld Bankruptcy - WSJ

In an interesting turn of events, Cineplex has started talks with Cineworld’s lenders about taking over the US Cinema Chain Regal Theatres (owned by Cineworld). According to the WSJ article, there has been precedent for this sort of move during bankruptcy as noted in the American Airlines filing in 2011 when it merged with US Airways:

Extracts - Cineplex has started early talks with Cineworld’s lenders about taking over the company’s U.S.-based Regal movie theater chain and handing them debt and stock backed by the merged business in return, these people said.

Cineplex would need to garner broad-based lender backing for the merger and Cineworld hasn’t signaled support for merging its crown-jewel Regal chain with Cineplex in a bankruptcy deal, these people said

Lenders have advocated for mergers out of bankruptcy before. American Airlines, which filed for bankruptcy in 2011, merged with US Airways in 2013 after creditors pushed for a restructuring plan that included combining the two airlines.

Sidenote: Cineworld posted interim figures on 30 September

US HY Q3 bond issuance lowest Q3 total since 2008 - Pitchbook

Pitchbook reports that 3Q US HY volume as at 20 September totalled only $16.9bn which is the lowest Q3 total since 2008 according to LCD. Also, $4bn of that amount is accounted for by the monster deal for Citrix.

Atlas Corp (parent of Seaspan) - Poseidon increases take private bid to $15.50/share

Poseidon, which comprises Atlas' board chairman David Sokol, affiliates of Canadian investment company Fairfax Financial Holdings Ltd , the Washington Family, and Japanese shipping company Ocean Network Express Pte Ltd, has upped its offer to the asset manager to $15.50 cash per common share. Source

UK’s Co-op Group strengthens balance sheet but sees lower profits - Co-Op

Reduced net debt position from year end through improved cashflow; sale of non-core petrol forecourt business (due in H2) set to reduce debt significantly further.

Group profit before tax: £7m Down £37m on H1 2021 (£44m)

Energy and wage inflation increased costs by around £50m versus H1 2021 before mitigating cost savings, and rates holidays in H1 2021 create a further £20m adverse variance.

Copper Mountain sees big increase to reserves - CIM Magazine

A new reserve estimate for Canadian Copper Miner sees Copper Mountain adding over 10 years to its life of mine.

Norwegian E&P Mime Petroleum carrying out strategic review process

Mime…announces that the Company is carrying out a strategic review process and has hired advisors to assist in the process. This process may include a strategic sale and/or entering into potential business combinations with other companies.

This follows another statement in September where Mime stated that the operator of the Balder X project, Vår Energi updated markets on the progress for the Balder X development and a revised cost estimate reflecting an increased scope of work.

Side note: the Norwegian government has recently increased the security around all its oil fields and infrastructure following the attack on the Nord Stream pipelines. Norwegian oil has become an even more important resource for Europe in light of the expected ban on Russian oil and gas.

*CHINA*

CCB to set up 30bn Yuan fund to buy properties from developers - ET

China Construction Bank will set up a 30 bn yuan ($4.2 billion) fund to buy properties from developers. The fund will "invest in existing assets" of real estate companies and renovate the properties into rental housing, the lender said in a statement to the Shanghai stock exchange on Friday. The fund lasts for 10 years, with a possible extension, according to CCB, which is one of China's big four state-owned lenders.

*EM/ASIA*

EM Rate hikes this week

Mexico hiked rates 75 bps to 9.25% (11th hike)

Colombia hikes rates 100 bps to 10.00% (9th hike)

Kenya: the CBK hiked its policy rate by 75bp from +7.50% to +8.25% (surprise)

South African Reserve Bank (SARB) raised the reference rate by 75 bps, to 6.25%

Shamaran exchanges 2023 bond into 2025 bond and appoints new CFO - Shamaran

As expected following the Sarsang acquisition Shamaran’s 2023 bond

Elvis Pellumbi appointed as new Chief Financial Officer of Shamaran Petroleum, Canadian listed E&P firm operating in Kurdistan. Mr. Pellumbi has debt and M&A experience and has invested “well in excess of USD 500 million in oil & gas companies focused in the Kurdistan Region since 2009 and is very familiar with the key players in the sector.”

On Monday, Macau Casinos Jump Most in Six Months on Tourism Revival Bet

Extract - (Bloomberg) -- Macau casino stocks surged the most in six months after the city announced plans to welcome back tour groups from mainland China as soon as November, a breakthrough for the gaming hub’s Covid-hammered, tourism-dependent economy. Wynn Resorts Ltd. soared as much 15% Monday to $68.89 in New York, the biggest intraday gain since November. Las Vegas Sands Corp. jumped 14% to $40.50, the biggest advance since May. Both stocks led the S&P 500 index. Shares of MGM Resorts International were up as much as 5%.

*RATINGS*

JPMorgan: Upgraded to A1 by Moody's

Fitch Revises Heimstaden Bostad AB's Outlook to Negative; Affirms IDR at 'BBB'

S&P puts UK Credit Rating on negative outlook

FITCH AFFIRMS HARBOUR ENERGY AT 'BB'; OUTLOOK STABLE

*CREDIT TRADING*

Jefferies reported slower Fixed Income net revenues..

Extracts:

3m perf: Fixed Income net revenues reflect mark to market losses on certain mortgage inventory positions and a slowdown in securitization activity as a result of continued uncertainty in respect of inflation and interest rates.

9m perf: Fixed Income results were impacted by lower trading volumes, mark to market losses on certain mortgage inventory positions and a slowdown in securitization activity in the face of inflation concerns and interest rate uncertainty.

F.I net revenues were up 8% QoQ but down 15% YoY for the quarter. The Major US Banks will be reporting Q3 earnings on 14th and 17th October as per Earnings Whisper’s calendar below.

*ESG*

IMF managing director suggests carbon credits to pay off debt - Nassau Guardian

Extract: IMF MD Kristalina Georgieva advocated yesterday for small island developing nations to be able to repay their debts in the form of carbon credits. Georgieva was a part of a panel conversation with Prime Minister Philip Davis and World Bank President David Malpass for the New York Times Climate Forward event discussing “Money in Action: Closing the Climate Finance Gap”. Pointing to the prime minister’s reference to The Bahamas as one of the world’s largest carbon sinks, Georgieva said low carbon emitting nations like The Bahamas should be able to exchange carbon assets for debt forgiveness.

Barbados blue bond to help Caribbean with liability management - Euromoney

…In the overwhelmingly green world of sustainable finance, blue debt-for-nature swap deals are still scarce. Credit Suisse’s announcement of a $146.5 million dual currency blended finance blue loan for Barbados on September 21, is therefore significant. The deal was done alongside CIBC FirstCaribbean and build on the Swiss firm’s blue bond for ocean conservation transaction with the government of Belize last year.

Goldman, HSBC in Talks With Pemex on $1 Billion ESG Financing

Petroleos Mexicanos is seeking financing from HSBC and Goldman Sachs Group Inc. in a deal that will tie funds to reducing greenhouse gas emissions. The banks have reached a preliminary agreement to provide financing to Pemex linked to carbon emissions reduction goals as the Mexican state producer struggles under a liquidity crunch and faces increasing pressure from investors to improve its environmental track record, according to people with knowledge of the situation. The banks will provide about $1 billion, one of the people said.

*LINKS*

Top Takeaways From Oaktree's Quarterly Letters - 3Q2022

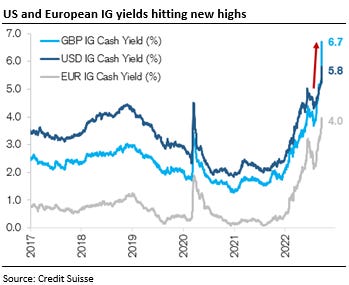

US/EUR/GBP IG yields hit new highs - CS

Expected returns for bonds are finally attractive - Ben Carlson

Bond Yields Are Finally Looking Attractive. What to Buy Now - Barrons.com

High-Grade Bonds Attract Junk Buyers as Yields Hit 13-Year Peak - Yahoo Finance

KKR update on Global Perspectives by CIO

9Fin Podcast - “The new playbook for LBOs”

BBG interview with CDS guru Boaz Weinstein

Sidenote: Weinstein seemed to be more sanguine about rumours of Credit Suisse’s problems this weekend…

Until rates vol subsides…other markets are likely to remain volatile

Global bond losses

Yet another “worst Global bond market…” chart

4% the magic number?

US Retail Investors loading up on 2yr bonds?