Sustainable bonds are lowering the cost of capital for Large Firms / Sovereigns

Activity centered in Europe...

When I refer to sustainable bonds, I encompass green bonds, social bonds and similar instruments that have some sort of ESG angle to it.

Since the COVID19 pandemic, there has been a big rise in these types of instruments, spanning a diverse set of issuers and instruments across different areas in the credit markets. There have been AT1s, Convertibles, Senior Bonds, Corporate Hybrids and sustainability linked bonds being issued, demonstrating the innovation that is ripe in this sector.

Europe has been the leader in championing sustainable investing which has seen a noticeable pick-up in issuance. The European Union will sell 225 billion euros of green bonds as part of its pandemic recovery fund according to Reuters.

The debt will make up about 30% of the EU’s 750 billion euro rescue package, and will be equivalent to approximately all the green securities sold globally last year. (Src: Bloomberg).

Do Green Bonds always trade cheap to Conventional Bonds?

Taking a handful of examples, it seems that sustainable bonds trade broadly in line with their closest conventional bonds. For example BBVA’s 6% AT1 bond does not trade materially different vs its conventional AT1 bonds and Mexico’s recently issued 2027 EUR bonds sustainability linked bonds trade around 20bps tighter than its conventional 2028 bond (at the time of writing).

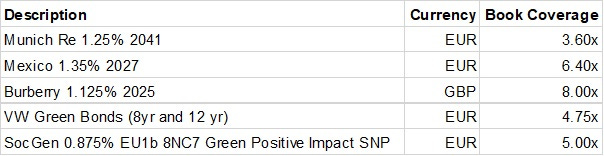

Where the benefit appears to be is at the primary stage, where issuers have managed to squeeze coupons very tight, for example Munich Re 1.25% 2041 (callable May 2031) and Burberry 1.125% 2025. The book sizes have been eye-popping on some of the recent new issuance.

Source: BBG

The coupon of 1.350% on Mexico’s issuance was the second lowest among all euro- denominated bonds issued by the Mexico federal government, which is not bad going especially since the country is in the middle of a pandemic.

So effectively issuers can lock in low coupons for a long time, a variation of a theme that has played out in Investment Grade credit markets since the Global Financial Crisis.

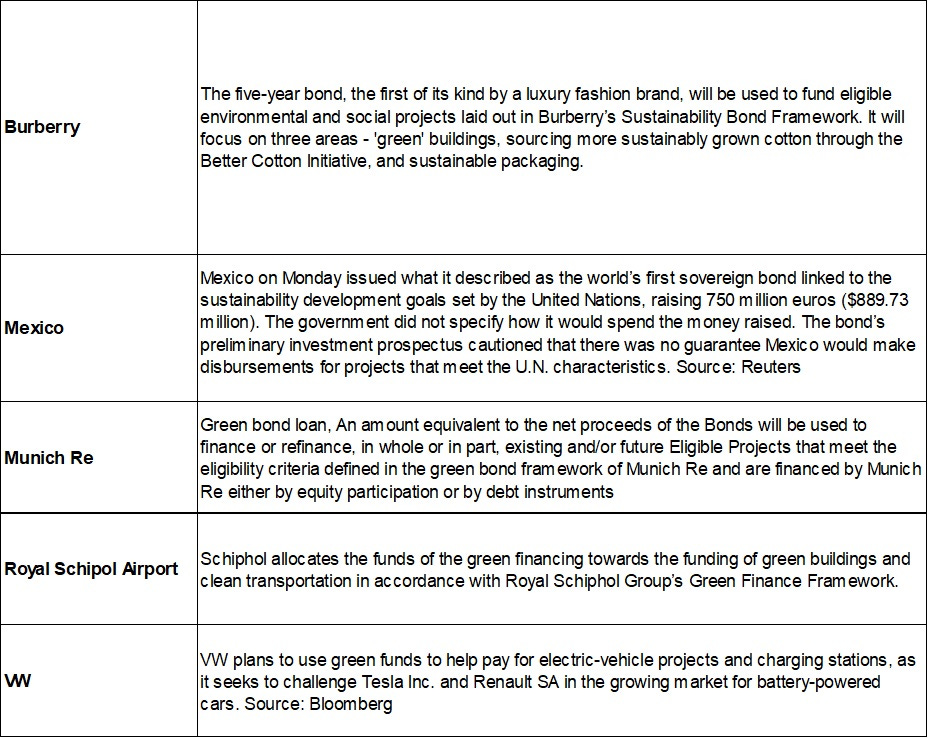

What are issuers saying about use of proceeds for these bonds?

Sources: BBG, Reuters, Companies

The issuance of sustainability bonds is a positive development that should see more funds go towards targeted projects to address Environmental, Sustainability and Governance goals. More crucially (for Corporate Treasurers) it is currently a very cheap form of funding for many large caps and major sovereigns, which should see more organisations issuing in this format.

Just today, the ECB announced that it is to accept sustainability bonds as collateral, there is no surprise here, but just another positive wind in the sails for sustainable/green bonds. Link to statement: https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr200922~482e4a5a90.en.html