Global Credit Wrap w/e 22 July 2022

Global Credit Wrap w/e 22 July 2022

Some positivity in Global Credit Markets...

*TLDR*

Macro

ECB hiked more than expected. New TPI tool announced.

US & Germany - Weak eco data this week saw Treasuries rally a lot. Similar story in Germany where there were record moves in the 1 and 2 year Bund.

Credit Market Moves

Big positive moves in Bond ETF land with TLT, LQD, EMB, HYG leading over the week. Some gigantic percentage moves took place in longer dated lower rated EM Sovereigns…

Within CDS 5 year Xover tightened in 74bps but remains elevated at +532bps. Within cash credit EUR HY tightened in the most at 57bps.

Corporates

Increasing amount of corporate actions/debt buybacks/financings. Generally creditor friendly behaviour, e.g. debt buybacks from AMC, Freeport, Delta Airlines and Heimstaden. Equity raises from Carnival, Aston Martin and Heimstaden.

EM & China

Anti government/inflation protests spreading to Investment Grade EM nations (Panama). Fitch revises Pakistan outlook to negative. Ukraine is set to extend its debt maturities.

Foreign outflows from Chinese government bonds hit a record in June, the fifth straight month of selling. China Property bonds plunging to new lows with likes of Country Garden and CIFI down 40% this month only! However, Caixin released a headline on new Infrastructure program supported by top two banks this weekend, will it be enough to sustain the risk on rally?

Loans/Private Credit

New section discussing JPM’s entrance into direct lending, how private credit firms are doling out more modest cheques due to possible recession, and further secondary trading activity at large discounts to originally issued prices.

ESG

Pemex releases first ESG document!

CREDIT TRADING

Deep dive on MarketAxess H1 results to understand credit trading trends better in volatile markets.

*MACRO*

The Return of Yield - Superb chart..

h/t @BlackRock via The Daily Shot Lev Borodovsky

This is a striking chart, showing how starved Fixed Income Investors have been for the 10 years post the GFC. It is telling that a good proportion of yield in fixed income indices has originated from EM, but only what part of the story is told here, i.e. the chart does not account for defaults.

Job cuts / freezes roundup

As the market starts to shift its focus from the fight against inflation to a slowing economy, there is a closer scrutiny on what corporates are doing with respect to hiring/firing. Here are some of the snippets I picked up this week:

Cost Cuts + Job cuts Loom in Investment Banks as Underwriting Keeps Disappointing

Just Eat Moves to Eliminate 350 Delivery Jobs in France

FORD TO ANNOUNCE 8,000 JOB CUTS - BBG

Goldman Sachs is planning to slow its hiring pace in the second half of the year, after staffing up for the pandemic deal making boom

Microsoft Slows Hiring in Security and Cloud in Weaker Economy

Alphabet Inc will be slowing the pace of hiring for the rest of the year and prioritizing engineering and technical talent

Lyft told employees it was reining in hiring in May after its stock dropped precipitously.

Macro snippets from US Bank Earnings this week (BofA)

Mortgage originations fell to $14.5 billion in the second quarter, down from $20.3 billion a year ago. Rising interest rates have sapped refinancing demand and are starting to weigh on purchases, a challenge for large banks' mortgage businesses.

Loans in the bank's commercial division rose 16%. That is positive news for a bank that, like its peers, struggled to profit from lending for much of the pandemic because of rock-bottom interest rates and tepid loan demand.

At Bank of America, executives said, customers have upped their spending while maintaining elevated deposit balances. Credit card spending rose 17%. Loan balances also increased.

Bank of America's U.S. customers are spending more on services and less on goods, Mr. Moynihan said. Customers spent 41% more on travel and entertainment in the second quarter than they did a year ago. They are also paying more for fuel, spending 42% more on gas.

Default rates remain near record lows, and customers are "paying off their debt at a good clip," Mr. Moynihan said.

"The consumer's in great shape, and the Fed's got a lot of work to do," Alastair Borthwick, Bank of America's chief financial officer, said.

Recap of key US Data this week:

The weakening data saw Treasuries rally towards the end of the week.

U.S. July flash S&P Global PMIs weakened: The manufacturing index dipped to 52.3 in July after falling -4.3 points to 52.7 in June. The index has fallen for three straight months to the lowest since July 2020.

New orders dropped to 48.6 versus 48.7, a second straight month in contraction and weakest since May 2020.

Services PMI also declined -5.7 points to 47.0 after slipping in June to 52.7. Fourth straight monthly drop and also lowest since May 2020.

Prices charged slid to 60.8 from 62.9 in June and is the lowest since March 2021. Employment slumped to the lowest since February.

Composite index tumbled -4.8 points to 47.5 after the 1.3 point drop to 52.3 previously. It is at the lowest since May 2020.

Philadelphia Fed: Prices paid fell to 52.2 from 64.5, new orders 6 months ahead were -24.8

Empire Fed: new orders 6-month outlook to 0 from 14

This coming week we hear from the FOMC…market participants will be keen to hear J Powell and team’s take on the recent data with respect to rate hikes and QT.

Germany PMI miss saw a huge rally in 2 year bund

ECB launches TPI - Project Syndicate

Extract: The European Central Bank has launched a Transmission Protection Instrument (TPI) to prevent monetary policy fragmentation within the eurozone. Announced just after the ECB Governing Council’s July 21 meeting, the TPI has overshadowed the news that the ECB will raise its policy rate by 50 basis points, which is more than expected but less than the macroeconomic situation and the price stability mandate demand.

According to the ECB’s press release, the TPI “will be an addition to the Governing Council’s toolkit and can be activated to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area.” If certain pre-established criteria are met, “the Eurosystem will be able to make secondary market purchases of securities issued in jurisdictions experiencing a deterioration in financing conditions not warranted by country-specific fundamentals, to counter risks to the transmission mechanism. Article continues on Project Syndicate.

*CREDIT MKT MOVES*

Cash credit spreads - All major subsectors in Credit tightened in this week. Closing levels remain elevated as demonstrated by EM HY USD (+877bps), EUR IG (+192bps) and Pan Euro HY (+603bps).

CDS Indices - Similar tightening bias seen here with notable mentions for 5y XOVER (-74bps), Itraxx Main (-18bps), Sub Fins (-37bps), CDX HY (-31bps). Levels on indices remain rather elevated still, e.g. with XOVER closing the week at 532bps.

The moves are especially interesting as the debate roars on regarding recession and the impact on credit spreads. Just this week, Barclays analysts predicted spreads to blow out to recessionary type levels.

Bond ETFs - Some very exciting moves here over 5 days.

Rates ETFs - TLT+3.1%, IGLT +2.2%, IUSB +1.5%

IG Credit ETFs - LQD +2.3%, IEAC+ 1.9%, LQDB +1.9%, VCIT +1.7%.

Drilling down, longer duration positions helped the move in LQD, with the 10+ year bucket providing the largest contribution to returns this week. Big single name movers included Boeing and Oilfield services names like HAL and SLB.

Higher beta bond ETFs - EMB+4.0%, JNK+3.0%, IHYG +3.0%, EHYB+2.9%, HYG+2.8%, AT1+2.0%.

Drilling down into EMB, again similar story to LQD whereby duration trades performed the best. However, the moves (in percentage terms) were absolutely humungous in some cases. The list of best performers read like a “whos who” of bonds that have been out of favour for most of this year and possibly even the end of last year! Basically lowly rated EM duration. Examples with 5d price % changes:

Ecuador 2040 +26%

El Salvador 2052 +24%

Angola 9.125% 2049 +20% [to give context price went from 60 to 72 there]

Nigeria 2047 +17%

Senegal 2048 +15%

Sri Lanka 2029 +12.7%

Within US HY, the lowest rated buckets (CCCs and Single Bs) saw the biggest positive moves in the week with out of favour names like Carvana, Bausch Health and Dish comfortably posting double digit percentage gains.

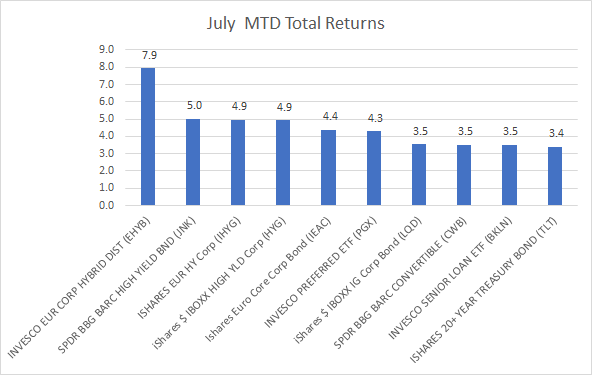

July has been a good month generally with some big moves for many of these ETFs, I have highlighted any moves above 3% below:

On the flip side, Bond ETFs I track that have lagged this move have been EMLC (-2.2% MTD) and CEMB (-0.08% MTD) and SHV (0.0% MTD). For the MTD, it looks like Corporate Hybrids, European and US HY, Investment Grade, Loans and Duration have “caught a bid” in this rally whereas EM is lagging despite a strong rally for EMB over 5 days.

*NEW ISSUES/TENDERS*

Inv. Grade - Imperial Brands raises 5 year bond at 6.0%!

BBB rated Tobacco company Imperial Brands raised $1bn of 5 year bonds at +320bps. I’m not an expert on the credit but that seems an unusually large spread for a BBB rated issuer. The wide spreads are likely a combination of narrower investor base (tobacco/ESG concerns) and a market where investors are generally demanding better concessions to buy credit. The bond was priced at 98.95 and closed the week out at 101.7/102 area.

AMC bought $72.5mm of 2nd lien notes in open market purchases in Q2

Extract: AMC…the largest theatrical exhibition company in the world, announced today that during the second quarter ended June 30, 3022 it strengthened its balance sheet by repurchasing approximately $72.5 million of its 10.0% Second Lien Subordinated Secured Notes due 2026, through the open market, for approximately $50.0 million, representing a 31% discount to the face value of the debt. As a result of this debt reduction, AMC’s annual interest cost will be reduced by $7.25 million…“This action is one more step along our recovery glidepath. We will continue to seek creative and meaningful strategies to further strengthen our balance sheet and create value for our shareholders in the future.”

Large cap Copper Miner Freeport McMoran retired $750mm of debt in last quarter

FCX commented in its earnings call that it retired $750 million of debt in the open market at a discount:

“We took advantage of weakness in credit markets during the quarter and opportunistically repurchased debt in the open market. To date, we have purchased $754 million of FCX's notes in open market transactions at a cost of $718 million including $582 million in principal amount in the second quarter. The current market situation provides a great opportunity for us to reduce absolute debt levels at attractive prices.

Real Estate firm Heimstaden Bostad redeemed EU868 million of corporate hybrids …This was fully financed by SEK6.9 billion equity raised from existing shareholders. The action may have also been a key driver behind a broader rally in other Real Estate Corporate Hybrids and Hybrids more generally as evidenced by the EHYB ETF which is up nearly 8% month to date.

Other firms with debt buyback/tender activity included Delta Airlines and LendInvest

*HY*

Better times in HY? Some seem to think so - check the thread.

Cruiseliners - CDC ends COVID-1 Program for Cruise Ships

Extract from USA Today: The Centers for Disease Control and Prevention ended its COVID-19 Program for Cruise Ships on Monday. "CDC has worked closely with the cruise industry, state, territorial, and local health authorities, and federal and seaport partners to provide a safer and healthier environment for cruise passengers and crew. Cruise ships have access to guidance and tools to manage their own COVID-19 mitigation programs." The CDC added that "while cruising poses some risk of COVID-19 transmission, CDC will continue to publish guidance to help cruise ships continue to provide a safer and healthier environment for crew, passengers, and communities going forward."

Aston Martin gains Saudi Arabia SWF as 2nd largest shareholder

Extract from Motor Authority website:

Aston Martin has turned to equity funding to help pay down debts as well as fuel investment in future product, and in the process has gained Saudi Arabia's sovereign wealth fund, known as the Public Investment Fund, as a key shareholder—the second largest shareholder, in fact, after Yew Tree, the consortium led by fashion mogul Lawrence Stroll, father of Aston Martin Formula 1 driver Lance Stroll.

Under the deal announced on Friday, Aston Martin plans to raise 653 million British pounds (approximately $773 million) via an initial investment of 78 million British pounds from Saudi Arabia and the rest via a separate rights issue. At the conclusion of the deal, Saudi Arabia will own 16.7% of Aston Martin, behind the 18.3% of Yew Tree and ahead of the 9.7% of Mercedes-Benz. Saudi Arabia will also gain two seats on Aston Martin's board.

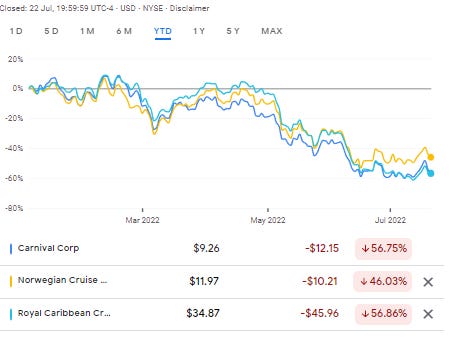

Carnival equity raise to “address 2023 debt maturities”

Carnival, whose share price had risen 25% between the end of June and 20th July then dropped 11% in one day (21st July) following the announcement of a substantial ($1bn) equity raise. In its official press release, CCL stated that it “expects to use the net proceeds from the offering for general corporate purposes, which could include addressing 2023 debt maturities.”

*EM*

Ukraine’s Debt-Relief Plan Gets Backing From Key Creditors - BBG

Ukraine’s request to postpone foreign-debt payments in the wake of Russia’s invasion won support from key government creditors and private bondholders. The government in Kyiv wants to agree with bondholders on a two-year payment freeze and changes to coupons on its so-called GDP warrants by the middle of next month. It filed a formal request to restructure $22.8 billion in sovereign debt on Wednesday.

The full article is worth a read since it goes into more detail about where certain Ukrainian Sovereign debt is currently trading.

Barrick allies with Pakistan on Reko Diq copper-gold project

Pakistan’s Finance Minister, Miftah Ismail, and Barrick Gold’s President and Chief Executive, Mark Bristow, have announced, after their recent meeting in Islamadbad, Pakistan, that they share a clear vision of the national strategic importance of the Reko Diq copper-gold project. Both sides have declared their commitment to developing the project as a world-class mine that will create value for Pakistan and its people through multiple generations. Worldminingreview.

Panama sees heavy rioting, joining certain other EM nations in similar protests

Al-Jazeera summarised Investment Grade EM Nation Panama’s current problems well:

The latest protests come as Panama battles an inflation rate of 4.2 percent in May; unemployment numbers of about 10 percent; and an increase in fuel costs of almost 50 percent since January.

Teachers were the first group to demonstrate at the start of July but they have since been joined by other groups, including construction workers, students and members of Indigenous groups.

Initially, the protesters called for the freezing and reduction of fuel prices, a price cap on food and an increase in the budget for education, but the demands have since widened to include a national negotiation to address political corruption and discuss larger political reforms.

“There are no medical supplies, there are salary cuts, and there is no work. There is no money to pay the doctors,” a Medical Studen (Janireth Dominguez) said. “As a student, the future worries me a lot.”

Morgan Stanley Says Buy Salvadoran Bonds Battered by Bitcoin Bet - BBG

Extract: “The government’s $7.7 billion in eurobonds have been “overly punished” by the market despite El Salvador having better metrics than other distressed peers, Simon Waever, the global head of emerging-market sovereign credit strategy at the bank, wrote in a note Tuesday. “

SOUTH AFRICA RAISES BENCHMARK RATE BY 75BPS TO 5.5%; EST. 5.25%

AerCap Cargo Signs Lease Agreements for Six 737-800 Boeing Converted Freighters with GOL

Interesting to see GOL Airlines expand its cargo franchise as it tries to offset the slow recovery its Corporate Travel revenues.

Extract: “Peter Anderson, Chief Commercial Officer of AerCap, said, "We are very pleased to announce our agreement to lease six 737-800 Boeing Converted Freighters to our longstanding customer GOL. These 737-800BCF's will be a versatile addition to GOL's fleet, allowing them to respond to the increased demand from e-commerce retail businesses in South America. We are delighted to expand our relationship with GOL and wish them every success with these aircraft in the years to come.” Announcement.

DNO received $246.6m net from KRG during Q2 2022

Extract: “During the quarter, DNO received USD 264.6 million net from the Kurdistan Regional Government, of which USD 183.8 million represents the entitlement share of January through March 2022 Tawke license crude oil deliveries. “ Announcement

*CHINA*

China Property Bonds round up

Well worth reading the full tweet thread above which contains info on more than just the China Property sector. The latest issue to plague this sector is the mortgage and supplier loan boycotts to Chinese Real Estate firms. Extracts from the Tweet above and associated articles:

Foreign outflows from Chinese government bonds hit a record in June, the fifth straight month of selling. Prices on junk dollar debt are on the brink of an all-time low.

Dollar bonds from Country Garden Holdings Co., China’s largest builder by contracted sales, and CIFI Holdings Group Inc. have lost nearly 40% this month through Tuesday.

“We maintain our view that the situation is not triggering systematic crisis or social stability issues yet,” said Zerlina Zeng, a senior analyst at CreditSights. “The scale of the reported mortgage and supplier loan boycott is still small compared to outstanding loan balances.” She expects China to coordinate with banks, developers and state-run entities to restart stalled projects soon, with non-viable ones likely converted into social housing or urban renewal projects.

Top China Banks Start Lending Funds in $45 Billion Infrastructure Plan: Caixin

Extract: Two of China’s policy lenders set up new units to handle financing in Beijing’s latest 300 billion yuan ($45 billion) round of infrastructure spending to bolster the staggering economy. China Development Bank (CDB), the country’s largest policy bank, issued 1.3 billion yuan of loans through a newly established infrastructure fund management company to finance a highway construction project in Shanxi and an airport project in Henan, the bank said Friday.

*FINANCIALS*

Nordea Profit Beats Estimates as Lending Growth Continues - BBG

Nordea Bank Abp’s profit beat estimates in a turbulent second quarter for financial markets, as demand for loans and rising interest rates herald higher income from lending for the biggest Nordic bank.

*LOANS / PRIVATE CREDIT*

JPMorgan deploys big 'chunk of capital' in leveraged loans to take on direct lenders: FT

Extract from Seeking Alpha:

In an effort to compete with direct lenders, JPMorgan has thrown a "significant chunk of capital" to keep self-funded leveraged loans on its balance sheet, the Financial Times reported Wednesday, citing Kevin Foley, the megabank's head of global debt capital markets.

JPM started making that debt in 2021 and has locked in around 20 deals. Now "we want to hold on to it" instead of underwriting leveraged loans and high-yield bonds for syndication, Foley told the FT.

“This is modern-day relationship lending. We have to adjust,” Foley said, as quoted by the FT. “We have a team of six dedicated to direct lending across banking, markets and commercial banking.”

To me, this move makes sense since syndicated markets are largely frozen at the moment and JPM wants to hold on to more of the business. Although JPM’s move is a reversal of the bigger trend we saw post GFC when most banks were forced to reduce their on-balance sheet lending.

Private Credit Giants Curb Buyout Lending Spree in Big Shift - BBG

Extracts:

Blackstone, Apollo., Ares Management, KKR, Antares Capital, and the asset management arm of Goldman Sachs are cutting the amount of debt they’re providing per deal as recession risk rises.

They’re also asking for, and getting, higher yields on financing packages with less leverage, while commanding stronger investor protections in case corporate borrowers go under [Editor: This is generally positive for credit investors and public credit investors should take note]

“With rates going up along with other macroeconomic economic factors, including Ukraine, we expect market activity to be slower than last year, which was a record year,” said Kipp deVeer, head of credit at Ares Management, adding: “We are seeing smaller hold sizes in new deals, which probably decreases an issuer’s ability to execute really large transactions in the current volatile environment.”

In the first half of the year these private credit firms were willing to band together to provide as much as $5 billion, or even $7 billion, of debt for an acquisition. That has dwindled to around $2 billion for the unitranche loan portion, said one of the people, though such a figure remains large by historic standards.

Stepping back, making smaller loans makes sense as private credit firms also dial down risk appetite ahead of a recessionary period.

Pimco Buys $1 Billion in Loans for Apollo M&A at Deep Discount - BBG

Pimco picked up leveraged loans of Worldline (payments company) from banks including Bank of America and Barclays in the range of 85 cents on the euro according to sources. Apollo’s buyout of Worldline SA’s payment terminals unit was financed in early March, when debt markets were in much better shape.

According to the article, Pimco has also scooped up 545 million euros of senior secured debt backing the buyout of Wm Morrison Supermarkets Plc at 85% of face value. These notes appear to be trading now around 83/85.

Orange, Masmovil Get EU6.6B Loan for Spain Merger

Orange and MasMovil have signed a binding agreement to combine operations in Spain in a deal valuing the merged entity at close to $19 billion, the two telecoms firms said in a statement on Saturday. The merged entity creates challenger to Telefonica.

Consolidation seems to be the theme in UK/European Telcos with Virgin media supposedly eyeing up a bid for Talk Talk.

Financing was provided by a series of European/US Banks in the form of EU4b TLA loan, EU2b bridge loan to be placed in debt markets from 2023.

This deal demonstrates that funding markets remain open for large well known brands in sectors that are expected to fare better than most going into a possible recessionary period.

Sources: Bloomberg, Reuters

*RATINGS*

T-Mobile was upgraded by Moody's to Baa3 from Ba2

Moody's downgrades Lloyds Banking Group's senior unsecured debt ratings to A3 from A2, stable outlook maintained

Moody’s downgraded Lloyds as a consequence of reviewing its Loss Given Failure (‘LGF’) assumptions. Not a major game changer. Source: Moody’s

Moody's upgrades Saipem's CFR to Ba3, outlook stable

S&P changed the outlook on Greek Banks to Positive from Stable

S&P changed the outlook on the Greek banks to Positive from Stable including all of the main four Greek banks (Alpha Bank, Eurobank, National Bank, Piraeus).

X-S&PGR Puts Aston Martin On CreditWatch Pos On Equity Financing

Fitch Revises Pakistan's Outlook to Negative; Affirms at 'B-'

Moody's downgrades Sharjah's ratings to Ba1, changes outlook to stable - Zaywa

Brazil: Fitch affirmed the BB- sovereign rating on the country and changed the outlook from negative to stable

Fitch downgraded Turkey’s foreign debt rating to B from B+, with a negative outlook

*ESG*

Once-Unthinkable Nuclear Green Bonds Are Coming to Europe - BBG

Extract: “Europe’s green bond market is preparing to finance nuclear energy projects for the first time. Electricite de France SA has updated its green financing framework to include nuclear after European Union lawmakers voted to give certain nuclear energy projects a sustainable label. A number of other companies are talking to investors about it, according to NatWest Markets Plc, one of the top 10 arrangers of environmental bond deals.“

Pemex releases first ever note on ESG

Readers, please correct me if I am wrong but I have never seen a specific ESG document from Pemex before…Pemex ESG Document 2022.

*CREDIT TRADING*

Credit Suisse looks to shrink credit trading by 25% - IFR

Extract: “Credit trading co-head Jonathan Moore's decision to leave the bank in May was partly motivated by the scale of the planned cuts, sources said, which have already seen a staff reduction of over 15% this year in that business. Many of the departures are in Europe, which is smaller and less profitable than the bank’s US credit trading franchise, the sources said, but a number of senior New-York traders have also headed for the exit.”

MarketAxess H1 2022 - Highlights

We have increased our leadership position in the global credit institutional e-trading space versus our primary competitors with strong market share momentum in corporate bonds and emerging markets

We achieved record levels of estimated market share across both credit and rates, driving a new quarterly record for global credit trading volume.

Achieved another record quarter with $23 billion in total portfolio trading volume.

MarketAxess launched an ETF on its MarketAxess investment grade 400 index

Just eight months ago, we predicted that an end to accommodative central bank policy and quantitative easing would drive a return to wider credit spreads and higher credit spread volatility. That is exactly what is happening today. And we are now in a much more favorable operating environment.

Median bid/ask spread in high-grade has moved from two basis points to four basis points in a very short period of time

Central bank tightening has led to a substantial increase in short maturity yields and a reduction in average maturity is traded, which has created a short term headwind for high-grade institutional fee capture.

According to the major global banks we recently surveyed, the MarketAxess lead in institutional client electronic credit trading has widened in all three geographic regions

one percentage point increase in market share across all our products generates approximately $50 million in incremental revenue annually

Estimated high-grade and high yield portfolio trading market volume represented approximately 6% of the total high-grade and high yield TRACE market in Q2 up slightly from the first quarter.

Strong growth in trading volume and market share gains across credit and rates was partially offset by a 10% decrease in total credit fee capture and lower information services and post trade revenue.

The lower high grade fee capture was driven by a combination of higher bond yields and lower years to maturity, which accounted for approximately 85% of the $31 year-over-year decline. The decrease in other credit fee capture was driven principally by product mix shift as a result of the increase in EM local markets trading volume, which has a lower average fee capture as these are rates focus markets.

within high-grade corporate bond, institutional client trading, clients trade on a yield spread to treasuries and our transaction fee is also based on a yield spread which is why duration matters in determining that outcome for high-grade fee capture

ETF shares had a very active quarter volume this quarter. Part of that was outflows in the sector. But a part of it is because the institutional market, both dealers and investors are using ETFs as another risk transfer tool.

Rick, I would just add, as we see rates rise, and fixed income assets become more attractive, particularly for retail investors we would expect fund flows to be quite positive towards fixed income ETFs and rather than managed funds over time.

…two high yield dealers migrating to a fixed fee plan and those fixed fee plans are $150,000 a month. So it's 450 per quarter that you're seeing a pickup. And it's a good sign for us because it means that those dealers anticipate that they're going to do more on the platform. We're still charging a transaction fee for those fixed fee plans.

But they're not, they are paying a lower transaction fee as compared to the monthly minimum commitment fee planning around previously

…we've seen hybrid electronic trading moved from 20% to near 35% to 40% over the past several years…

Q: Just wondering if you can provide the average years to maturity for high grade in the quarter. And remind us the historical range that you've seen for that high grade bucket? A: Yes, for the second quarter was just over nine for the years to maturity and it's been hovering around high eight, low nines for the last couple of quarters, it peaked out at 10 Kyle back in Q1 of '21. But going back longer term in 2019, it did hit the mid 7s

*TWEETS/LINKS*

Bit more detail on that Barclays Research Note re wider credit spreads

Prices..

Food prices should come down…

Made.com profit warning reflective of cautious spending on certain goods