Global Credit Wrap 2 September

Record issuance in financials, record lows being retested in long dated credit

A quiet week for markets, but some interesting moves/levels in the credit markets nonetheless. A short read this week.

*TL: DR*

MACRO + INFLATION

Government bonds continue to underperform led lower by Gilts

Eurozone inflation hits record (9.1%)

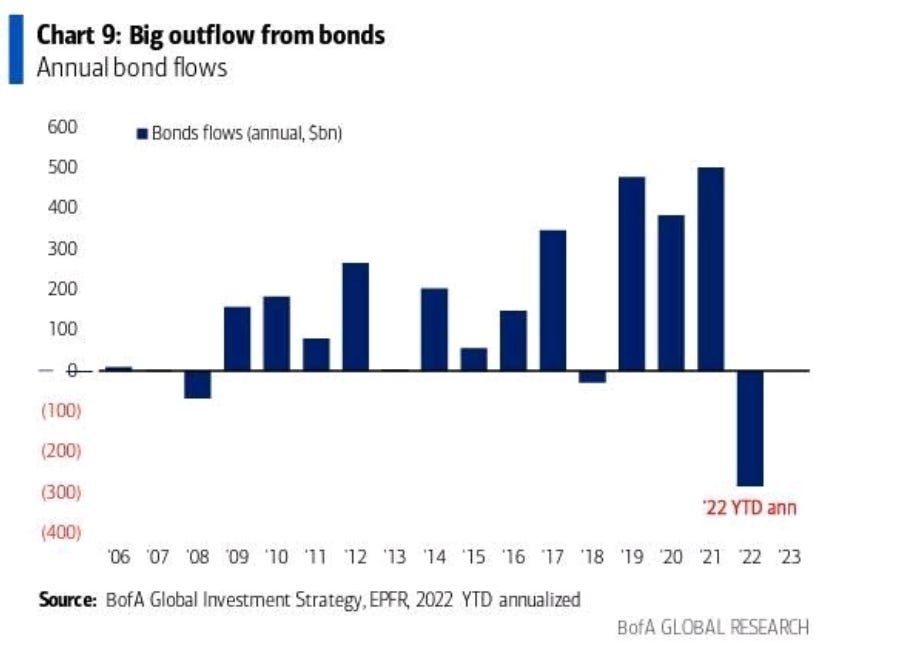

HY and IG funds see outflows again, YTD outflows largest since 2002

Fed speak remains uniformly hawkish

IG

Long duration credit testing record lows again

Certain Utilities in Germany, Sweden and Austria need state support

Merck KGAA looks to tender for its Corporate Hybrids

HY

US CCC rated spreads went through 1000 again

Some bonds in UK/Europe trading at or below pandemic levels now

FINANCIALS

August was a record issuance month for European Financials

Senior / T2 bonds coming with coupons higher than 2021 vintage AT1s!

EM

IMF advancing funding for Pakistan/Sri Lanka

*MOVES OVER 5D*

CDS - Mostly flattish except CDX HY which was 30bps wider to close at +528bps.

Cash spreads - All spread indicators widened with the greatest widening in HY:US HY+41bps to 493 bps, EUR HY +41bps to +585bps. EM resumed its widening trend after some respite in August (EMHY+21bps). UK and European IG corporate aggregate credit spreads are above 200bps (EUR IG +205bps, GBP +207bps). US IG spreads are at +145bps compared to the high of +160bps.

Bond ETFs - Yet another tough week for IGLT (-3.7%) and TLT (-2.0%) joining in the weakness. Duration focused credit ETFs also sold off, e.g. LQD (-1.4%), PGX (-1.7%). On that duration point, I note that on a single bond level, many long dated bonds are reaching the lows seen in July 2022 with many of them priced in the 60s/70s. In terms of yield bogeys, higher rated bond yields appear to have broke through the 4% mark again in USD.

For those looking cross currency and at lower rated bonds, there is now a growing list of IG rated bonds near the 50 price point:

Another feature of this current credit market is how many bonds are trading at or below their lows of 2020. These appear to be concentrated in sectors most affected by the higher rates/inflation/energy costs - e.g. Pubs, REITs and Real Estate. This brings into question how much of the negativity is already priced in.

*MACRO*

International Treasury Bond ETF…yikes

US Junk-Bond Investors Pull $5.04 Billion in week ended 31 August - BBG

Extract: “The outflows come after withdrawals totaling $4.57 billion a week earlier, following four straight weeks of inflows. It was the second largest weekly outflow of the year. US investment-grade bond funds also registered outflows, as investors plucked $4.64 billion from bond funds. “ Looking YTD, BoFA says $284bn outflow represents the largest since 2002.

*INFLATION*

Eurozone inflation hits record (9.1%)

More on European Inflation

Pace of US Rent Increases Continues to Slow - Calculated risk blog

Rents are still increasing, but slower than last year according to Bill Mcbride. He cites data from ApartmentList.com: Apartment List National Rent Report which shows the size of increase of rents falling.

*US*

The US job market remains hot as judged by the latest JOLTS data

Whole threat below is useful.

Big 4 accounting firms starting to pay $100k base for consulting undergrads- EFC

U.S. Consumer Confidence Rose in August After Three Months of Decline - Yahoo

The Conference Board found that its consumer confidence index was at 103.2 in August, up from 95.3 in July. This was ahead of expectations of 97.7 predicted by economists polled by Reuters.

“Concerns about inflation continued their retreat but remained elevated,” Lynn Franco, senior director of economic indicators at The Conference Board said.

“Meanwhile, purchasing intentions increased after a July pullback, and vacation intentions reached an eight-month high. Looking ahead, August’s improvement in confidence may help support spending, but inflation and additional rate hikes still pose risks to economic growth in the short term.”

*FEDSPEAK*

Fed's Williams’: Very Unlikely Fed Will Cut Rates Next Year - CNBC

Barkin Says Fed Will ‘Do What It Takes’ to Curb Inflation - BBG

From the FOMC Speak page on St Louis Fed:

Fed’s Harker Says Let Rates ‘Stay Up There’ and Play Out

Atlanta Fed's Bostic Wants 'Moderately Restrictive' Policy

Mester Says Fed Might Need to Move Rates Above 4% and Hold

*UK/IRE*

£ Corporate Bond ETF returning nearly the same as the FTSE 250 ETF YTD

SLXX TR -17.8% vs VMID TR -18.2%.

UK sells government bond with highest yield since 2014 - Nasdaq news

Extract: “Sept 1 (Reuters) - Britain sold 2 billion pounds of government debt on Thursday for which it will have to pay the highest interest rate since 2014, reflecting the sharp sell-off in bond prices as inflation has surged. The 0.875% January 2046 gilt sold at auction with an average yield of 3.224%, the highest for any British government bond sold since mid-2014, when a 2060 gilt paid an interest rate of 3.367% and a 2034 bond paid 3.243%.”

UK Gym bond issuers having worst week due to cost of living crisis - BBG

An article on the terminal suggests that HY rated bonds for recreational centers have served up negative returns of 13.4%, worse than the 11.92% negative returns recorded across the broader European high-yield market. Two of the UK Gym issuers including Pure Gym which operates at the budget end and David Lloyds in the higher earnings bracket.

*IG*

Remember negative yielding IG bonds?

MERCK KGAA: Tender offer for Corporate Hybrids

Extract of co statement: The purpose of the Offers is, amongst other things, to proactively manage the Company's layer of hybrid capital: through the transaction, the Company expects to reduce its EUR 3.0 billion hybrid capital portfolio by up to EUR 250 million.”

Could we see other Corporate Hybrid issuers follow by tendering for their paper at large discounts to par?

Uniper Seeks 4 Billion Euros From State Lender as Liquidity Deteriorates - FP

Extract: “German energy giant Uniper SE is seeking to extend a government credit line to 13 billion euros ($13 billion) in the latest sign of how Europe’s energy crisis is getting worse. The utility has requested an additional 4 billion euros from Germany’s state-owned lender KfW after fully using its existing 9 billion-euro credit line, Uniper said in a statement on Monday. The additional funding request is about double the Dusseldorf-based company’s current market value.”

For Uniper the cost of replacing missing supplies from Russia is leading to losses of more than 100 million euros a day, which is why the size of the bailout is so huge.

Meanwhile Austria and Sweden are also looking at emergency measures for its energy companies.

*FINANCIALS*

JPM called $2.5bn of its former JPM 5% perps in full

The bond had a floating coupon of 3m Libor + 332bps.

August was a record month for financials issuance

One US Bank pointed out this week that August was a record month for financials with issuance totaling nearly €64bn. Within that there were 5 AT1s totaling €7bn. The blowout issuance is in stark contrast to the Corporate market, in particular HY Corporates where issuance is down significantly YoY.

Summary of issuance this week - AT1-esque coupons on senior and T2…!

Sterling was an active currency for financials issuance this week. Credit Suisse nowadays seems to trade in its own relative value spectrum as its bonds are priced so wide to other banks. This week it issued two senior bonds in Sterling 5NC4 and 11NC10 with coupons of 7% and 7.375%. Away from CS, Bank of Ireland issued a T2 bond with a coupon of 7.594% again in GBP. Compare this to AT1 coupons for bonds issued only as recently as last year: OneSavings Bank 6% AT1, Natwest 5.125% AT1, Nationwide 5.75%. Lloyds Bank did issue an AT1 this week with a coupon of 8.5%, the bond is rated IG from two agencies.

In Euros, there was issuance from Commerzbank (T2 with 6.5% coupon) and BNP (AT1 with coupon of 6.875%).

*HY*

CCCs went through 1000bps

United and Emirates set to enter into a codeshare agreement - Simply Flying

Extracts: “According to Reuters, sources have confirmed that United and Emirates will be announcing a codeshare agreement….A codeshare with United would be Emirates' second in the United States. Emirates currently has a codeshare agreement with JetBlue and previously had one with Alaska Airlines. American recently announced an expansion of its strategic alliance with Qatar Airways, originally announced two years ago. The expansion of the partnership was a new codeshare agreement that expanded to an additional 16 countries. In June, American also launched a new nonstop service from John F. Kennedy International Airport in New York City and Hamad International Airport in Doha. This new route established American Airlines as the only United States airline to serve the Gulf region.”

*EM*

Good thread covering off major events in MENA this week

IMF Staff Reaches Staff-Level Agreement on an EFF Arrangement with Sri Lanka

Extract: IMF staff and the Sri Lankan authorities have reached a staff-level agreement to support Sri Lanka's economic policies with a 48-month arrangement under the Extended Fund Facility (EFF) of about US$2.9 billion.

The objectives of Sri Lanka’s new Fund-supported program are to restore macroeconomic stability and debt sustainability, while safeguarding financial stability, protecting the vulnerable, and stepping up structural reforms to address corruption vulnerabilities and unlock Sri Lanka’s growth potential.

Debt relief from Sri Lanka’s creditors and additional financing from multilateral partners will be required to help ensure debt sustainability and close financing gaps. Financing assurances to restore debt sustainability from Sri Lanka’s official creditors and making a good faith effort to reach a collaborative agreement with private creditors are crucial before the IMF can provide financial support to Sri Lanka.

The last paragraph is crucial as Sri Lanka now needs its to come to an agreement with its creditors as to what sort of debt relief it can gain. Sri Lanka bond prices had been rallying ahead of the announcement and popped around 10% on the actual announcement.

Pakistan: IMF approved revival of loan programme, releasing $1.17bn - Al Jazeera

Extract: “The IMF board has approved the seventh and eighth reviews of Pakistan’s bailout programme, Finance Minister Miftah Ismail said, which will release $1.17bn in funds to the cash-strapped country. Ismail also said the IMF agreed to extend the programme by a year and augment the funds by $1bn.”

Ukrainian Railway to Open Two Additional Rail Links to Romania - BBG

Romania is currently Ukrainian Railways’ most active direction for shipments Ukrainian Railways is in talks to restore rails on Romania’s territory New links may allow transportation of 3.5m tons of additional cargo per year.

Cemex sells Costa Rica and El Salvador assets for US$329m

“Cemex has successfully closed its sale of its Costa Rica and El Salvador subsidiaries to Cementos Progreso for US$329m. Cemex plans to use the proceeds from the divestments to fund its bolt-on investment growth strategy, reduce its debt and for other general corporate purposes.” Global Cement

*LINKS*

Savers rejoice: Yield is back - Ben Carlson

Extract: “The bad news is the Fed raising interest rates is likely one of the reasons the stock market is falling and could push the economy into a recession. The good news is savers like you can finally find some yield on their cash.”

Bigger Than the GFC: The Once in a Lifetime Cycle in Distressed Debt - Man Group

Extract: “Global levels of distressed debt already rival those seen during the GFC. Could we be on the cusp of a career-defining cycle for distressed debt investors?”