Global Credit Wrap 14 October

2 year UST @ 4.5%, new post-2009 high in IG corp yields, Corporate Hybrids "special."

*TLDR*

*MACRO*

2 and 3 year UST at 4.5%, reducing the opportunity cost vs risk assets

US IG Yields hit new post-2009 high of 5.81%

Two very big M&A announcements this week (Kroger/Albertsons & Peabody Coal / Coronado Global)

Asian nations keep tightening monetary conditions (Singapore/South Korea)

Airlines defying recessionary call, reporting better than expected figs

UK:

BoE expanded its toolkit to buy Gilt linkers after record 1d widening

BoE expanded accepted collateral list to include Corporate Credit

Money market funds see huge inflows as Pension funds look to park cash ahead of end of BoE bond buybacks

Santander UK sees loan losses creeping up due to rise in missed payments

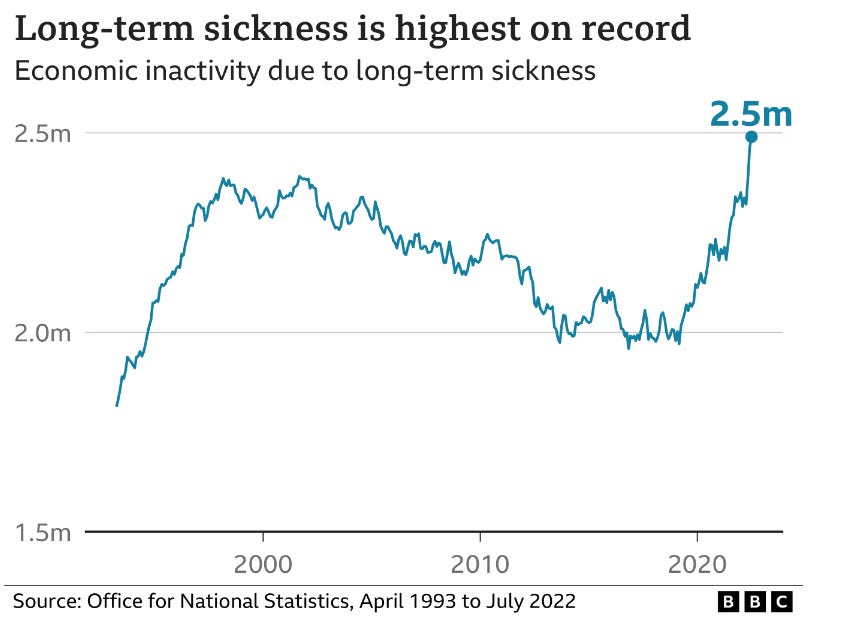

UK labour market - Population with long term sickness hits record high

*INFLATION*

US CPI came in hotter than expected

Sweden inflation hits cycle high

Pepsi increased prices by 17% YoY - A good example of how a firm with a strong brand and low dollar cost per item can raise prices meaningfully without destroying demand materially

*NEW ISSUES / TENDERS

Handful of HY and EM deals came with double digit coupons + decent OIDs

Good take up for recent bond tenders (e.g Lloyds Bank / Softbank) indicative of risk tone and secondary market liquidity (poor)

*IG*

Tender offers / calls for Engie and Naturgy this week

S&P ratings commentary around Corporate Hybrids worth a look

Real Estate/REIT Hybrids trade 20pts lower vs broad Hybrid sector

*HY*

JPM strategist: EUR Distressed Debt now equals 15% of EUR HY Universe

One firm goes public over its size purchases of Citrix/Nielsen debt

*FINANCIALS*

Challenger Bank Shawbrook - looking to exchange AT1 rather than call at upcoming call date

Sabadell non-call of AT1 (largely expected)

Blackrock earnings call highlights - sees generational opportunities in F.I

*EM*

Barbados became 13th country to benefit from IMF support since Russia/Ukraine war

Pakistan bonds hit record low

Sri Lanka falling in line with IMF requirements by raising taxes

Nigeria Fin Min talking about possible debt restructuring

*RATINGS*

Deutsche Bank Upgraded to A1 by Moody’s, Outlook Stable

*CREDIT TRADING*

Margin calls everywhere (Peloton CEO, UK Pension Funds). Likely to keep seeing margin calls in other parts of the market if current environment persists

Blackrock’s Larry Fink explains LDI issue on earnings call

*LINKS*

Some awesome videos / content on Fixed income and credit this week

*NEXT WEEK*

Market reaction to appointment of Jeremy Hunt as new Chancellor, will Truss survive much longer?

Earnings season continues

*MOVES OVER 5D*

Credit spreads - Notable that CDS indices in Europe saw some mild tightening whereas cash credit spreads were wider. E.g Xover was 10bps tighter over 5 days whereas in cash credit; EUR HY was +27bps wider and EUR IG was 9bps wider. CDX EM was 20bps wider and EM HY USD cash credit spreads was 26bps wider.

Bond ETF moves - Seem out of whack with credit spread moves over 5 days. TIPS, IGLT, HYG and JNK posted mild gains this week ranging from 0.3% to 0.7%. Whereas biggest losers (1% or more) included PGX, EMLC, EMB, AT1, CEMB, LQD.

*MACRO*

Ex-Fed Official Clarida Sees Rates Staying in 4.5%-5% Range for ‘Long Time’ - BBG

Extract - “Under Chair Powell’s leadership, they are putting rates on a path where I think they’ll probably need to get, which is somewhere between 4 1/2 and 5%, next year,” Clarida said in an interview with CNN aired Wednesday. “They’re going to keep them there for a long time.”

Singapore tightens policy, keeps door open for more moves on hot inflation - RTRS

Singapore tightened monetary policy as expected for the fourth time this year to combat inflation running near a 14-year high, and left the door open for further policy action as it warned of risks to the growth and price outlook. The central bank made two off-cycle tightening moves in January and July to rein in soaring inflation in the trade-reliant Asian financial hub. Friday's move, seen by some as less aggressive as MAS adjusted only one of the three levers in its policy band, marked the fifth tightening since last October.

South Korea BOK raised its policy rate +50bp to 3.0% (in line with expectations)

A number of Airlines reported strong figures this week

Airlines such as American and IAG pre-announced their quarterly figures due to much better than expected performance over the quarter. IAG noted its booking trends remain strong, suggesting recessionary behaviour is yet to impact the sector meaningfully.

Sources: CNBC, Simple Flying, Company websites

UK Unemployment at lowest rate in nearly 50 years, but looking under the bonnet..

The reason the rate is so low is mainly been due to the rising population of those with a long term illness unable to work.

Extract - The number of people not looking for work because they are suffering from a long-term illness has hit a record high, latest official figures show. The fall in the number looking for work has helped to push the unemployment rate to its lowest for nearly 50 years. ONS head of labour market and household statistics David Freeman said the number of people neither working nor looking for work had continued to rise over the past few months. BBC

Likely reasons for the spike in long term sickness are; long COVID, hugely delayed treatments due to a faltering NHS and some dissatisfaction with work.

Santander UK boss seeing more UK borrowers falling behind on payments - Guardian

Extract - Santander, the UK’s fourth-biggest mortgage lender, will increase its standard variable rate by 0.25 percentage points to 6.24% from the start of November, and its two-year fixed-rate mortgages now command an interest rate of 6.04%. “We’ve seen a very slight increase, but not yet a significant increase, in the number of customers who are falling behind on mortgage payments or … payments on cards, or loans or overdrafts,” Mike Regnier, Boss of Santander UK said.

Investors piled into Sterling money-market funds during rate turbulence - RTRS

Extract - Investors piled cash into sterling money-market funds at more than three times their usual rate during the recent turbulence in British bond markets, and pension funds likely made up the bulk of those inflows, Fitch Ratings said on Friday. Fitch said it believed most of the increase in recent inflows in MMFs was down to pension funds building up cash given an increase in collateral requirements from many LDI funds. The maximum daily inflow at a fund level among Fitch-rated sterling short-term money market funds (MMFs) peaked at 17% of assets under management on Sept. 30 compared with a usual level of around 5%, the ratings agency said in a note.

This sounds similar to what has been happening in the states lately where investors continue to park a record amount in the Fed’s reverse repo facility.

*INFLATION*

CPI takes from FinTwit

Forecasts

Food costs

Diesel prices are soaring in Europe and the US…[BBG]

There is a worry that the rise in Diesel prices will result in a fresh bout of inflationary pressures ahead of tricky winter.

“The global diesel market is very strong at the moment,” said Mark Williams, research director for short term oils at WoodMackenzie Ltd. “Higher diesel prices have the potential to create even stronger inflationary pressures, especially if the current price spike is sustained, adding significant downside risk to demand and increasing the chances of a global recession.”

The latest surge in Europe has been helped by curbed supply in France, where a strike over pay at oil refineries has limited fuel supplies and forced the government to tap strategic reserves.

In the US, inventories are perilously low ahead of the winter season. It’s the same story for independent stockpiles held in Amsterdam-Rotterdam-Antwerp, northwest Europe’s oil trading hub. Consumption of heating oil -- a diesel-type fuel -- typically rises in winter.

Sweden’s CPI hits new cycle highs in September - Business Standard

"Higher electricity prices and higher prices for food and non-alcoholic beverages contributed to the high inflation in September," Caroline Neander, a price statistician, said in a statement on Thursday. Electricity prices have increased by 54.2 per cent, and food and non-alcoholic beverages by 16.1 per cent over the past 12 months, Xinhua news agency reported.

Germany planning an urgent €96bn plan to ease pressure on consumers - RTRS

Germany said it plans to urgently implement a €96 billion plan to ease pressure on consumers from surging gas prices.

Redfin real time rent data showing a slowdown in asking rents in the US

Strategists are now debating how long it will take for this to filter into official inflation gauges which the Fed follows.

Pepsi raised prices on its snacks and drinks by 17% on average from last year

Extract of Irish Examiner: “Pepsi lifted its annual forecasts for revenue and profit as the drinks and snack giant raised prices again to battle surging costs while also signalling resilient consumer demand.”

*NEW ISSUES & TENDERS*

HY and EM issuers came with more double digit coupon deals

AMC $400 5NC2 with IPT of 12.75% coupon at a discount of $95-96.

Fedrigoni IPT on EUR 875m 2027s at 11.75%-12%

Latam Air $450m 5NC2 Fixed at 94.423 to Yield 15% | Coupon: 13.375%

Latam Air $700m 7NC3 Fixed (Oct. 15, 2029) at 93.103 to Yield 15%

ENQLN 11 ⅝ 11/01/2027 priced at 98.611 to yield 12%

So much to unpack here...good to see issuers get deals done, but eye-wateringly expensive even for certain improving credits. Viewed another way, these deals enable investors to lock in high coupon multi year return streams should the borrowers stay current on their payments.

EnQuest refinances 2023 $ bond with new bond yielding 12% and new RCF

North Sea Oil independent oil company EnQuest refinanced its USD 792.3m senior 2023 notes with a new USD 305m note maturing in 2027 and an amended USD 500m RBL. EnQuest’s NIBD/EBITDA was 0.9x. Despite the supportive backdrop for oil companies and low leverage, the company had to attract investors with bonds yielding 12%. This is more of a reflection of the pricing in the HY market for Single Bs and a nod towards the risk of buying a cyclical name ahead of a possible recession. The remaining Sterling 2023 EnQuest notes are set to be paid with organic cashflows in the lead up to maturity in 2023.

Decent take up for recent bond tender offers (Lloyds/Softbank)

Lloyds Bank’s 7.625% AT1 had around £1bn tendered in its latest tender offer, leaving only £135m outstanding. Softbank tendered for $2.26bn of its notes in aggregate which included $750m of its $2.75bn Softbank 6% Corporate Hybrids. The reason for the high take up is likely due to asset managers wanting to hold greater liquidity through volatile conditions and an aversion to “hitting bids” in a illiquid secondary market.

*IG*

US IG Yields hit new post-2009 highs - Liza Abramowicz

Corporate Hybrid round up - Tenders/calls/price action

Engie tender offer - Utility is to buy back of upto 10% of its hybrid stack, which according to ratings agency S&P will not affect its remaining hybrid’s equity content as long as tender offers over a 12 month period does not exceed more than 10% of the hybrid stack. Engie is looking to tender for its 2023, 2024 and 2031 corporate hybrids. If recent tender offers are anything to go buy in the subordinated bond space, take up is likely to be high as these corporate actions are likely to give better exits for holders than market prices.

Naturgy is to redeem €1bn of its 4.125% Corporate Hybrids - on November 18th at par plus accrued and unpaid interest. Naturgy is a multinational natural gas and electrical energy utility company predominantly based in Spain. The hybrids raced up 3.5pts on the day of the call (13th October). In contrast to the statement on Engie, S&P revised the equity content on ALL of Naturgy’s remaining hybrids to “minimal” from “intermediate.” This is on S&P’s working assumption that the company will not replace it, presumably due to market conditions and the company’s ability to absorb the increase in debt and eventually a redemption of all its corporate hybrids. Naturgy has generated a strong performance this year due to its LNG and wholesale gas businesses.

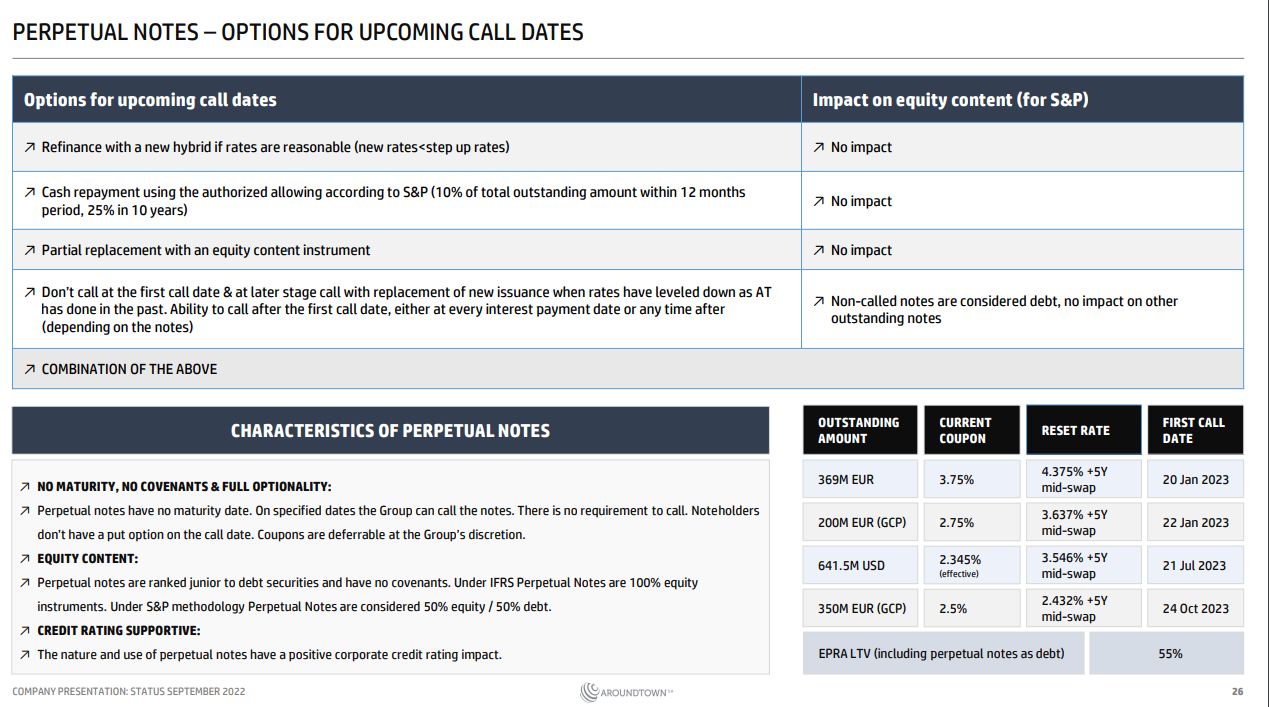

Pain in the REIT Corporate Hybrid Sector - Real Estate and REIT Corporate Hybrids experienced a further leg down this week as rate vol remains high. The chart below demonstrates how badly the subsector is doing vs aggregate Corporate Hybrids. The average Real Estate / REIT Hybrid trades nearly 20 points lower than the average Corporate Hybrid and average YTC is nearly 3 times as high as the average YTC for the Hybrid sector.

Most bonds are trading well below the lows seen during COVID when certain sectors saw their occupancy / footfall plunge to near zero during lockdowns. What could stem the decline; a soothing of rate volatility, corporate actions (calls/tender offers such as the Engie above). There have been corporate actions this year such as that for Heimstaden Bostad but little else. The issuer that has provided some clarity around future actions for its perps is Aroundtown which set out details in its most recent Investor presentation :

Source: Aroundtown September 2022

The next year will be an interesting one for this sector…

US Supermarket behemoth created overnight - Kroger to takeover Albertsons

Extract from BBG - Kroger Co. agreed to buy Albertsons Cos. in a deal with an enterprise value of $24.6 billion that would create a US grocery giant with almost 5,000 stores and annual revenue of about $200 billion.

In terms of the funding: Kroger said it has $17.4 billion in fully committed bridge financing from Citigroup Inc. and Wells Fargo & Co. The deal includes the assumption of $4.7 billion in net debt and is expected to close in early 2024, the companies said. Kroger Chief Executive Officer Rodney McMullen will lead the combined company.

Philips issues Q3 profit warning, takes further €1.3 billion charge - Dutch News

Extract - Inflation and falling orders are also having an impact on the company, which now says sales will decline 5% in the third quarter of the year to €4.3 billion. ‘Looking ahead, Philips still expects a better second half of the year, compared to the first half of 2022,’ the update said. ‘However, the company sees prolonged supply chain disruptions and a worsening macro-environment. Consequently, Philips now expects a mid-single-digit comparable sales decline for the fourth quarter of 2022.’

*HY*

CLOs have been one of the assets being sold by UK Pension Funds - BBG

There is another potential risk around the horizon with many CLOs only allowed to own a maximum of 7.5% in CCCs. The percentage of bonds in the next tier up (B- rated loans) in CLOs is the highest on record which presents a risk if some of those credits get downgraded.

Citigroup reports $110 mln leveraged-loan loss - RTRS

Extract: "We took about $110 million in total between markdowns and losses on loans in the leverage space," Citigroup's chief financial officer Mark Mason told reporters after the company released its third quarter earnings.

Meanwhile JPM and MS appeared to have lesser impacts from lev loan losses:

"There are no real levels of loan write-down this quarter, and that market isn't yet to clear," Jamie Dimon, JPMorgan's chief executive officer, told analysts on a conference call. "Our share of it is very small. So we're very comfortable." Morgan Stanley also scaled back its leveraged exposure in the third quarter. "They actually were quite modest marks, given the environment," Sharon Yeshaya, Morgan Stanley's chief financial officer, told analysts.

Carlyle Credit Arm goes public about buying up Citrix / Nielsen debt - BBG

Extract - Carlyle’s credit arm has invested around $750 million in the Citrix buyout, split about evenly between the secured debt portion that banks syndicated at steep losses last month, and a preferred equity piece that was arranged at the start of the year, according to people with knowledge of the matter. The firm also bought roughly $750 million of the $2.15 billion of second-lien debt backing the buyout of Nielsen that banks privately placed earlier this year with a group of lenders that included Ares Management Corp., the people said.

JPM: EUR Distressed Debt now equals 15% of HY Universe

The proportion of debt trading at distressed levels - at a spread of 1000 basis points or above - within the European high yield universe grew to 15% at the end of September, reaching levels not seen since 2020, according to a JPMorgan report last week. BBG

Peabody and Coronado in merger talks

The article in AFR seemed to have the most interesting take on the rationale for the deal: …As colleague Peter Ker has written, Peabody is mainly a thermal coal miner, so it may be using the sudden lift in profits it has experienced in the past 12 months to increase its exposure to coking coal, which has better prospects over the long term…Peabody may also see buying Coronado as an opportunity to lock in more stable long-term cash flow streams, in a world where its ability to attract funding from banks and a more ESG-focused bond market may be more limited than it has been in the past.

*FINANCIALS*

UK Challenger Bank Shawbrook looks to exchange AT1 bonds…

…instead of issuing in the new issue bond market. There are some incredible stats in this article on the topic. There has not been a single Sterling Corporate bond issue issued in the £ market since September 20th, just before the mini budget. Further details: “With no sign of volatility easing yet, Shawbrook Group Plc wants to keep investors happy by moving them to new notes that offer an 8.099 percentage-point premium over UK gilts, an extra 100 basis points versus its existing perpetual bonds. Under normal conditions, it would exercise an option to redeem them in December and issue new debt in the open market.”

The issuance of AT1s by Barclays, Lloyds, BNP and Credit Suisse a few months ago is looking pretty smart vs where the sector trades currently…

Sabadell skips AT1 call citing replacement costs under current mkt conditions

Blackrock - Q3 F.I focused earnings call highlights

Extracts:

Third quarter ETF net inflows of $22 billion were led by surging demand for our bond ETFs

Bond ETFs generated $37 billion in net inflows, the second best quarter in our history

Retail net outflows of $5 billion reflected ongoing industry pressures in active fixed income and world allocation strategies…

If we go back in 1995, to get a 7.5% yield, which is what many institutions were looking for. Our portfolio could be in 100% bonds. If you fast-forward 10 years, in 2005, it had to be 50% bonds, 40% equities and 10% alternatives. Then move another 10 years, and in 2016, you needed only 15% bonds, 60% equities, and 25% alternatives. This describes the growth of several markets. Now today to get that same 7.5% yield, a portfolio could be in 85% bonds and then 15% equities and alternatives

Blackrock is helping clients “pursue what I would call generational opportunities in the bond market, both institutional and individual”

*EM*

Barbados became 13th country to benefit from IMF support since Russia/Ukraine

Extract from Tellimer: Barbados last week became the 13th country that is set to benefit from (or has benefitted from) IMF support since Russia's invasion of Ukraine in February and the mostly indirect impact of subsequent higher food and fuel prices and the concomitant higher global rate outlook arising from the inflation shock.

Ghana hiked rates +250bps to 24.5% (100bp higher than expected)

Chile hikes 50bps to 11.25%, fwd guidance signals end of hiking cycle

Sri Lanka Moves to Raise Income Tax Levels as Part of IMF Pact - BBG

Extract: Sri Lanka has published a bill to legislate a planned increase in income taxes as part of the island nation’s measures to increase revenue under an agreement to get funding from the IMF:

The plan to increase taxes was unveiled in May

Personal income tax exemption threshold to be lowered, rates in each slab raised Standard corporate income tax proposed raised to 30% from current 24%

Tax rates for mutual funds, trusts to be raised

If Sri Lanka follows guidelines from the IMF, there is a better chance the country gets out of its current economic problems sooner.

Pakistan Dollar bonds traded at record lows this week

For example Pakistan 7.375% 2031 bonds issued in 2021 at par (100) are now trading in the low 30s. Bonds have not defaulted, but markets are implying a high level of default risk.

Nigeria Exploring Debt Restructuring, Finance Minister Says - BBG

Extract: Nigeria is considering restructuring its debt and extending the repayment period of its credit obligations, and appointed consultants to advise the government as it faces a rising debt-service burden, Finance Minister Zainab Ahmed said. Nigeria is one of the largest issuers in the EM hard currency bond market.

*CHINA*

The week started with very poor China data…

A much sharper than-expected decline of Caixin services PMI was reported from 55 to 49.3 in September (consensus: 54.4), the index slipping into contraction territory. The composite PMI deteriorated from 53 to 48.5.

China Property Developer Cifi defaults - SCMP

In the ongoing saga that is the China Property Bond Market, developer Cifi announced it has defaulted. The news weighed on the whole sector.

Extract - Chinese property developer Cifi Holdings has failed to make a bond payment, marking its first offshore default as the debt crisis gripping the property sector spread to companies previously deemed financially sound. Bondholders of Cifi’s HK$2.5 billion (US$318 million) convertible bond with an interest rate of 6.95 per cent due in 2025 did not receive the payment they were due on October 8 – payable on Monday as October 8 fell on a weekend – according to a notice from China Construction Bank (CCB), a trustee of the creditors. The Shanghai-based home builder blamed the National Day “golden week” holiday for the delayed payment and said it was working with creditors to find a solution.

*RATINGS*

Fitch Affirms Hawaiian Airlines at 'B-'; Outlook Stable

S&PGR Puts EnQuest On Watch Pos; Rates New Notes Prelim 'B+'

S&PGR Affirms Volkswagen AG At 'BBB+/A-2'; Outlook Stable

Deutsche Bank Upgraded to A1 by Moody’s, Outlook Stable

Transocean Upgraded to CCC by S&P

*ESG*

Enel in $800m Sustainability-Linked Financing with Denmark’s EKF - Enel IR

Anecdotally, Enel seems like a business that seems to get a LOT of financing from a diverse range of sources, just last week it was in the market raising a multi tranche deal from the US IG market in the form of an SLB…

Extract - The Enel Group (“Enel” or “the Group”) has received a facility from Denmark’s export credit agency, EKF, for up to 800 million US dollars. The facility, arranged by Citi, is based on the Group’s worldwide business relationship with Danish suppliers and is aimed at supporting the development of wind energy as well as mitigating the effects caused by climate change, as part of Enel’s 2040 Net-Zero ambition, through a flexible instrument.

*CREDIT TRADING*

Margin calls are becoming more and more common…

Whether its the former CEO of Peloton getting margin called or UK Pension Funds needing to post additional margin for their total return swaps, the instances of margin calls are increasing. Effects of QT, political volatility (as per the UK) and the War keep the risk of margin calls high in global markets. The long extract below from Larry Fink (CEO of Blackrock) on the UK LDI situation is quite insightful (taken from earnings call):

Larry Fink -- Chairman and Chief Executive Officer of Blackrock on LDI

Let me start with the context of LDI first. LDI has been a 20-year market. It's been transparent. Regulators have proved strategies.

Consultants were the ones who really approve the strategies on behalf of the individual funds. It is our estimate the LDI market in the U.K. is about $1.7 trillion. We have about 20% of that, $250 billion.

So let's describe what happened. These products were built with the idea that we'll -- create these strategies. You had risk corridors of 100 to 125 basis points. That corridor worked for over 20 years.

Because of a fiscal policy announcement by the U.K. government, markets fell over 100 basis points in one day. And many of the corridors were penetrated. Now what does that mean? It means the clients have to post margin in their total return swaps.

Many clients did not have the ability to rapidly post margin in a single day. And that created the market setback. The Bank of England comes in and steps in and stabilizes it. And during the stabilization period, for those who needed to be stabilized, for many of the funds, they posted the margins.

For many of the other funds that could not do it, we had to create, and other firms had to create different types of corridors, broadening the corridors, should the corridors be not 100 basis points, but a 200 basis point corridor. And that announcement by the Governor of Bank of England yesterday, it indicated to me that much of the reconstruction of these products have been done. They have the intelligence of every player in this. And as I said, some of the pension funds did not have a collateral.

And in doing so, they may have to sell other assets to meet margin calls. Some clients were easy to provide the margin call and some clients needed to have some form of restructuring. By the actions this morning, the Gilt markets have been -- I don't know the Gilt markets since we've been on this call, but as of this morning, Gilt markets were stable. And so it appears much of the reconstruction of these products may have been done, and the market maybe should be a little more normalized.

I'm not here to tell you I know the intelligence of has everybody done it, will there be more volatility starting in Monday on this, I don't know that. What I do believe that we should do like BlackRock was a leader in terms of money market reform, we want to work with the regulators, be a part of this to try to say, if volatility is going to continue to be this large, maybe there has to be whole redesigning of some of the products, whether that is in a commingled fund or in separate accounts. But we are going to be part of the solution to move this forward, as we always are. But I think this is a specific event to the U.K. pension market. And it was a major component of the U.K. pension market. And so it had very deliberate issues that impacted that market.

But as of now, there has been adequate time, in most cases, not all, I'm not here to suggest it's over, of changing the corridors, widening that, obviously at a cost, and then importantly, putting up the necessary margins that were necessary in the severe market moves in the U.K. Gilt market.

*LINKS*

Good video on broad F.I developments this week - Creditsights’ Winnie Cisar - BBG

Paul Tudor Jones believes the US economy is either near or already in the middle of a recession - CNBC

Nice tweet with a bunch of recent videos from credit market stalwarts

60:40 Portfolio Update - Wow!

Great wrap up