Global Credit Comment - W/E 2 April 2021

A different style to this week's post...talking investor protections, Ghana, Oracle and zero coupon CBs...

A comment from the co-founder of CreditSights and Credit Market veteran; Glenn Reynolds coupled with a few recent observations of global fixed income markets recently inspired this post.

Mr Reynolds was answering a question on the weekly Global Credit Wrap from CreditSights two Fridays ago on the topic of the credit cycle. He was asked what 3 things “newbies” in credit should look at to try to determine where we are in the credit cycle. While caveating that it is difficult to accurately ascertain where we are in the credit cycle, he said watch out for the “deal too far.” By this I believe he meant a bond/loan deal that pushed the limits of pricing and/or investor protections.

This seems to be an increasingly common phenomenon across various parts of global credit markets currently. The first section of this week’s blog touches on the European HY deal for Foncia in order to highlight an example of aggressive deal features related to investor protections/pricing. Then I touch on some subtle developments in the Convertible Bond market, the Ghana zero coupon bond and leveraging up of Tech behemoth Oracle, and whether this is a sign of things to come for other single A rated issuers. All these points considered together appear to form part of the same narrative; a restoration of the balance of power towards issuers again (after a brief favourable tilt towards investors in 2020).

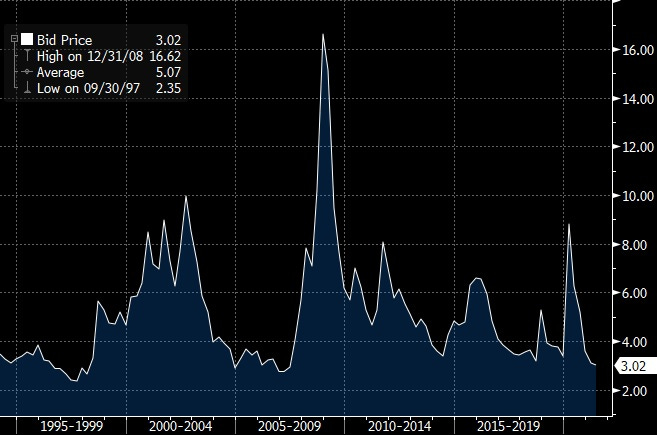

HY spreads are tight by historical standards and goes some way to explaining the record breaking Q1 2021 issuance in USD and European HY and Leveraged Loan markets.

Bloomberg Barclays US Corporate High Yield Average OAS

Foncia’s European HY deal - Assessing investor protections/pricing

Without wanting to re-invent the wheel, I decided to break down TwentyFourAM’s succinct blogpost (A New Low for Investor Protection in Euro High Yield) on new EUR HY issuer; Foncia. Extracts of the blog are in Italics, and my comments beneath them.

“French Real Estate servicer Foncia priced last Friday – €400m of secured bonds, €250m of unsecured bonds and a €1.275bn Term Loan B”

Key takeaway: The company in question – Foncia issued both loans and bonds.

“Foncia is a provider for every aspect surrounding the rental, management or sale of residential units. Since its acquisition by Partners Group back in 2016, Foncia has looked to be an improving story; the company has grown at a steady pace, generated cash and reduced its leverage, while its scale and brand has also enabled the acquisition of smaller rivals. Last week’s issuance facilitated a €475m dividend for Partners Group and refinanced existing debt. While investors are usually wary of dividend recap transactions, Foncia’s growing business in our view supports such a transaction.

Key take-aways:

1) Foncia is a PE owned group, so it is a leveraged situation.

2) There is a good “credit story” (growing at steady pace, generated cash, and reduced leverage)….credit guys love a good story…and so do DCM desks because it serve as a reason to drive down coupons and make covenants more favourable for the issuer/PE sponsor.

3) The new debt is being used to pay the PE firm (divi recap) and also a more legitimate reason of refinancing existing debt

4) “Foncia growing business” – Links to point 2, there is a good credit story.

“However, the troubling aspect of this transaction was the aggression of the covenants, with the initial documents appearing to leave a lot of leeway for the issuer at the expense of investors. For example, there were no caps or time limits for expected synergies and cost savings from acquisitions when computing the covenant debt ratio. The portability clause also looks generous based on a 6.4x consolidated net leverage ratio. There is also plenty of headroom for additional debt, allowing Foncia to add material leverage to the pro-forma leverage of 6.4x for this transaction. Most troubling of all was the inclusion of what many investors have come to call ‘J-Crew covenants’.”

There is a lot here, but the short story is that investor protections appear weak. The simplest ones I would highlight are: a) plenty of headroom for additional debt (meaning that future leverage could be tweaked higher without tripping covenants and b) the inclusion of the “J-Crew covenant.” I recommend you read the BestInterest Blog post to get an understanding of what this is.

Foncia’s Term Loan B docs were ultimately amended and a cap on EBITDA adjustments introduced, which suggests the issuer did receive some push-back from loan investors. However, the bond docs were not amended. Given the secured bonds were priced at 3.375% (from initial guidance of 3.5% area) and the CCC+ unsecured bonds were priced at 5% (well through initial guidance of 5.25-5.5%), it seems there was enough demand for the issuer to resist any push-back it did receive from bond investors.

With conditions in European HY looking favourable for opportunistic issuance, investors will have to be vigilant for more of these clauses over the coming months.”

Key takeaways:

1) Documentation on the loan was amended to make it bit more investor friendly (on this particular aspect) but bond investors accepted less investor friendly terms (on this aspect).

2) Both deals priced through the initial guidance. No surprise here, as the reach for yield mentality is still very much in play. Also, he “good credit story” point earlier would have enabled the lead managers to tighten the pricing.

3) Conditions look favourable for opportunistic issuers/issuance and investors will have to be “vigilant” to further deal structures like this.

The last point is really important. In any form of investing it takes “two to tango.” I.e. a company issues a security and the long-only investor either chooses to buy it or passes. The question is whether investors will “vote with their wallet” and pass on these deals or apply for smaller allocations? It’s a tough one. As demonstrated by Asda’s multi tranche deal earlier this year, better deal structure does not equal higher book demand. Investors in the Asda deal were more motivated to go in for the issue with higher subordination and therefore higher coupon as demonstrated by the book size of 5.5x on the unsecureds vs 2.0x on the secureds (source: Re-Org). For a bond fund to miss out on a well-performing deal (on the basis of a poor structure) risks the ire of its traders and possibly fund investors. This creates an awkward tension of managing risk by being invested in mainly well priced/structured deals, but not falling behind peers or the benchmark by passing on short-term alpha generating opportunities that may arise from weaker deals…As credit market veteran Glenn Reynolds remarked, watch out for the “deal too far.”

Other snippets in Credit

Is Oracle’s behaviour a blueprint for other Single-A rated issuers?

In March, technology behemoth Oracle was downgraded by two credit ratings agencies from single A to the BBBs. The downgrade was a byproduct of Oracle’s management appearing to prioritise shareholder returns over balance sheet strengths. Below are extracts of what Fitch had to say on the matter in March:

Issuance Deviates from Deleveraging Expectations: Oracle's proposed debt issuance deviates from Fitch's expectation of debt reduction to levels consistent with the 'A-' rating category, despite its intention to use the proceeds to repay debt maturities through FY22. The 'BBB+' rating category appropriately reflects the strong operating profile of the company and the aggressive capital structure given the higher credit risk resulting from high gross leverage and lower (CFO-capex)/Total Debt ratio.

High Financial Leverage: Oracle's financial leverage is high for the rating category. Fitch estimates gross leverage of 4.4x for FY21, declining to 3.2x by FY24 assuming the company continues to repay its debt maturities through FY24. However, Oracle's recent capital market activities suggest that the company could maintain debt at elevated levels that are inconsistent with the 'A' rating category.

Oracle expanded its share buyback plan and raised its dividend by 33%. The downgrade was naturally accompanied by some spread widening, and once that was out of the way, Oracle came with a new jumbo debt issue. This pushed Oracle’s debt load to double vs 2015 levels, according to analysts at Bloomberg Intelligence. The question really then boils down to how many other single-A rated firms would follow Oracle’s lead and prioritise shareholder returns over balance sheet strength?

Rise in zero coupon convertible bond issuance

2021 has seen a number of convertibles issue at zero or thereabouts. Brand names such as AirBnB, Ford, Spotify and Twitter have all issued converts of this nature.

It was particularly interesting that Ford which issued 7 year paper at 2.9% in the US HY market in February 2021 decided to go to the convertible bond market in March instead to issue a 5 year zero coupon CB. Clearly, one still would have some exposure to the upside in the equity, albeit with a lower margin of safety due to the zero coupon. The margin of safety concept is most evident in the “go-go” end of the convertible market. E.g. NIO which issued a 2026 maturity zero coupon CB in the middle of January this year has seen its CB trade into the 80s (vs an issue price of 100) as its stock has fallen more than 40% compared to its highs seen in February 2021.

Ghana Zero Coupon

This bond issue made complete sense for the Ghana sovereign. I.e. Ghana successfully issued $525m zero coupon 4 year bonds in order to redeem interest paying debt at the front end of their curve. According to an article on the Ghana Web website, the sovereign will use the proceeds of the zero coupon deal to redeem high interest local debt. I’m interested in hearing people’s views on this issue and relative value vs the interest paying comparators in the Ghana curve (2025/2026 bonds), feel free to comment below.

Hope you all have a good Easter break.

Disclaimer: This is not investment advice. I currently have no have positions in the securities listed above but this situation may change in the future. The views represent my own views and not that of any employer.