9 September 2022 Global Credit Wrap

Big issuance week, relief on energy costs, R.I.P negative rates...

*TLDR*

Macro

J Powell re-iterates emphasis of the Fed to act on inflation at Cato Conference

Interesting comments out of Fed’s Brainard and RBA’s Lowe re: future tightening…

Europe & Denmark move out of negative rates. Canada and Poland also hike

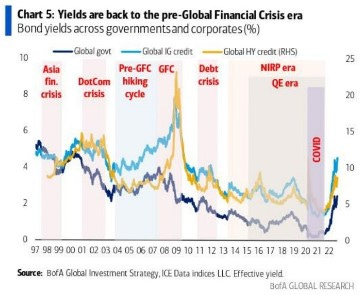

Yields back at pre GFC levels according to BofA chart

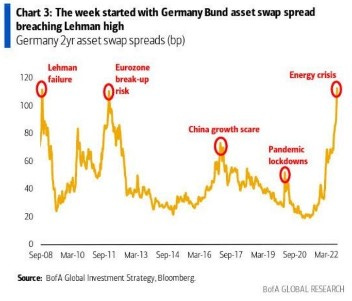

Some wild moves in 30 yr Gilts and German Bund asset swap spreads this week

Inflation

Chinese inflation slowing

Key contributors to inflation falling - shipping rates, used car vehicles and oil price (latter hit January 2022 levels)

Energy crisis

A number of measures were announced by Governments and Corporates to alleviate energy costs for consumers/businesses.

Shares/bonds of Utilities and energy consuming businesses (e.g. Supermarkets, Pubs) and short dated govt bonds rallied but longer dated govt bonds sold off in reaction to the news

New issues/Tenders

Over $50bn issued in US IG debt market with blue chip names in the market

EU IG primary market crossed €1tn issuance YTD

More Corporate Hybrid tenders in Europe

EM issuance making tentative comeback

*IG*

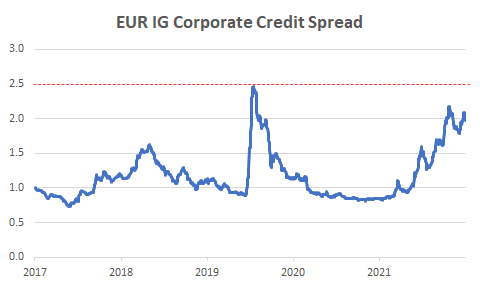

EUR IG credit spreads still hovering near pandemic highs

*HY*

United Airlines raised its 3Q revenue outlook, lifts sector

Cineworld formally filed for Chapter 11

*CREDIT TRADING*

MarketAxess and Tradeweb release August trading stats.

*MACRO CREDIT*

A chart for HM QE II - Source: BofA

Thank you for all that you have done for your country.

J Powell re-iterates Fed’s strong intention to bring inflation down' at Cato Conf.

Extracts from Coindesk article:

"It is very much our view, and my view, that we need to act now, forthrightly, strongly, as we have been doing," Powell said during a question and answer session at the Washington, D.C.-based Cato Institute.

In the U.S. “the clock is ticking” on inflation, forcing the Fed to act quickly, Powell said.

“The longer inflation remains well above target, the greater the risk the public does begin to see higher inflation as the norm,” Powell said.

As with his speech at the Fed’s annual economic symposium in Jackson Hole, Wyoming, last week, Powell took note of the “several failed attempts” by the 1970s Fed to cool inflation. Then-Chairman Paul Volcker finally took action to push for a rise in interest rates to extreme levels, thus pushing the U.S. into a difficult recession. Powell said it’s his hope today’s Fed can calm inflation without causing that kind of social cost.

Similar to remarks on Wednesday by Fed Vice Chair Lael Brainard, Powell stressed that restoring price stability will take time and cause some pain to the labor market and to households. It’s important, he said, not to claim victory over prices too soon.

“History cautions strongly against prematurely loosening policy,” said Powell. “I can assure you that my colleagues and I are strongly committed to this project and we will keep at it until the job is done.”

Fed’s Brainard mentioned risks of over-tightening in speech..

“The rapidity of the tightening cycle and its global nature, as well as the uncertainty around the pace at which the effects of tighter financial conditions are working their way through aggregate demand, create risks associated with over-tightening." This is only one sentence from an aptly titled speech this week from Brainard called “Bringing Inflation Down.”

Fed’s Bullard’s weekly update

Europe moves out of negative rates as ECB and Denmark hike

The ECB hiked with its largest ever move, and Denmark hiked rates above 0%.

The ECB seemed to leave possibility of another 75bps hike open.

Meanwhile the Danish Central bank raised its benchmark to 0.65% after the ECB. Denmark has had negative rates longer than any other country.

Australia CB increased the cash rate target by 50 basis points to 2.35%

The comments in the presser following the hike were largely hawkish, but later on in the week RBA Governor Lowe said: “we recognise that, all else equal, the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises.”

Note that Canada also hiked rates (fifth time in this hiking cycle) and Poland’s NBP raised its rate by +25bps to 6.75% (as expected).

Yields are back to pre GFC era - Bofa Chart (Michael Hartnett)

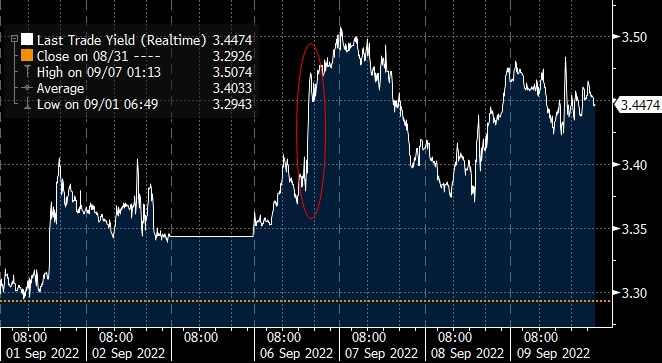

UK 30 year gilts traded +25bps intraday earlier this week

Prior to the announcement of the Liz Truss UK Energy bailout deal, UK 30 year gilt yields spiked +25bps. 30 year gilts topped out this week above 3.5% compared to when it started the year yielding 1.1%! I referred to this point in one of my tweets on the performance of long dated Gilt funds YTD.

Credit to Portfolio Advisor magazine for highlighting the damage done in Gilt Funds.

German Bund asset swap spread spikes

BBG - Demand for German securities has helped drive up the premium at which they trade versus interest-rate swaps. Two-year German bonds extended their premium over equivalent swaps Monday, with the spread set for the widest close since 2008.

“We do not see the demand for short-dated core bonds and bills abating,” said Morgan Stanley strategists including Eric Oynoyan in a note Monday. “The capped remuneration of government cash reserves at 0% will make them more and more attractive with the ECB depo hikes.”

Italy’s right-wing coalition, led by Giorgia Meloni’s Brothers of Italy - BBG

The Italian election is being watched for impact on Italian BTPs and Italian Financials/Corporates which are big issuers in the debt markets.

Extracts of article:

“Italy’s right-wing coalition, led by Giorgia Meloni’s Brothers of Italy, is poised for a landslide win on Sept. 25, according to the last available polls before a blackout period.

The bloc has an advantage of almost 20 percentage points on the center-left coalition led by Enrico Letta’s Democratic Party, according to Bloomberg’s latest polling average. Such an advantage, thanks to Italy’s complex electoral system, might grant it a two-thirds majority of seats in both houses of parliament, enough to change Italy’s constitution on its own.”

This year’s start of the hurricane season has been the quietest for 25 years - John Kemp | Reuters

This is good news especially for Reinsurers and LATAM/Caribbean nations regularly impacted by Hurricanes.

Extract: “The Atlantic hurricane season is nearing its halfway point and so far no hurricanes have made landfall on the coast of the United States, contributing to the recent downward pressure on oil and fuel prices. The Atlantic season lasts from June 1 to Nov. 30, with half of the storms usually occurring before Sept. 12, based on records compiled by the U.S. National Oceanic and Atmospheric Administration (NOAA).”

*ENERGY CRISIS*

A number of measures were introduced by Governments and Corporates to deal with the surge in Energy prices in UK/Europe:

UniCredit sets out $8 billion aid package for Italy clients hit by surging prices - Yahoo Finance

Germany: the country will keep two nuclear plants open this winter, reversing a previous plan to close them - Powermag

Portugal to Lower Value-Added Tax Rate on Electricity Bills - Yahoo

Dutch Eye Windfall Tax in $16 Billion Plan to Ease Energy Costs - BBG

The Dutch plan is different to that of the UK in that it is not excluding the possibility of a windfall tax:

“The Dutch government is said to be working on up to 16 billion euros ($16 billion) in funding to alleviate the burden of high energy prices and runaway inflation on its citizens. The plan will include a 10% increase to the minimum wage, a reduction to energy taxes and targeted subsidies to lower income households, according to people familiar with the matter. The package would be financed through a combination of higher income from the Groningen gas field, a profit tax increase on small and medium-sized enterprises and a windfall tax on companies extracting oil and gas, said the people, who spoke on condition of anonymity to discuss internal deliberations.”

A number of UK/European Utilities got financing from Governments

Extracts from insightful BBG article:

Finnish utility Fortum Oyj got 2.35 billion euros of bridge funding to ensure adequate liquidity.

Switzerland granted Axpo a credit line of up to 4 billion francs

Finland and Sweden announced a $33 billion emergency liquidity facility Sunday to backstop utilities through loans and credit guarantees.

In the UK, Centrica Plc is in talks with banks on the potential extension of credit lines, according to a person familiar with the matter. Centrica declined to comment.

These measures were taken to reduce the risk of a systemic collapse in Utilities. The European Utilities Equity Index (SX6P) seemed to like the news as it advance 2% over the week.

EU chief lays out five measures to tackle energy crisis: EN

An EU-wide plan to introduce "mandatory" electricity savings during peak hours (usually 7 am to 10 pm).

A cap on the excess revenues made by inframarginal generators, namely power plants that use sources cheaper than gas (renewables, nuclear, coal).

A "solidarity mechanism" to partially capture the excess profits made by fossil fuel companies (oil, gas and coal) during extraction, refinery and distribution.

A state aid programme to inject extra liquidity into struggling utility businesses, those who bring electricity to consumers once it has been produced.

A price cap on imports of Russian pipeline gas.

UK - Truss freezes energy retail bills for households and promises protection for businesses

This from Javier Blas of Bloomberg: “Truss on Thursday froze UK energy retail power and gas bills for the next 24 months, so an average household would pay no more than £2,500 ($2,877) per year, instead of the £3,549 that regulators set for the next three months and well below the £4,000-£5,000 expected in 2023. On top of that, she promised the “equivalent” protection to businesses for six months.”

The moves are likely to have big implications for Gilt yields (higher) and Gilt issuance (more issuance).

*INFLATION*

Chinese inflation comes down - Al Jazeera

China joins a handful of nations that are seeing signs of decelerating inflation statistics (US and Brazil).

Extract: China’s consumer prices rose at a slower-than-expected pace in August while producer inflation hit an 18-month low, pointing to weak domestic demand in the world’s second-largest economy.

The consumer price index (CPI) increased 2.5 percent from the same month a year earlier, National Bureau of Statistics (NBS) data showed on Friday, slower than 2.7 percent in July.

The producer price index (PPI) rose 2.3 percent, the slowest pace since February 2021, and slower than 4.2 percent a month prior, due to falling energy and raw materials prices. “Factory gate inflation is set to fall further throughout the rest of the year thanks to a continued drop back in commodity prices and a higher base for comparison,” Capital Economics analysts Sheana Yue and Zichun Huang said in a research note. “We think CPI inflation will remain below the PBOC’s 3 percent ceiling,” they said, referring to the People’s Bank of China.

Interesting to see how next week’s US CPI goes

Ocean freight rates are tumbling

WSJ had this to say: The cost to ship a 40-foot container from China to the U.S. West Coast now stands around $5,400 a box, down 60% from January, according to the Freightos Baltic Index. A container shipped from Asia to Europe costs $9,000, 42% less than at the start of the year. The rate for both routes, while still above prepandemic levels, peaked at more than $20,000 last September. Best Buy Co. Chief Executive Corie Barry said in an earnings call last Tuesday that freight-transportation cost pressures are easing. She said the electronics retailer, whose sales are shrinking, is finding it easier to get freight space on ships and trucks.

*NEW ISSUES/TENDERS*

Over $50bn was issued in US IG debt markets in a blockbuster week

A range of borrowers came to market including blue chip names such as Walmart, McDonalds, Stellantis. Concessions being paid averaged doubled digits. Interestingly, the level of issuance on one day could have been one of the contributors to the spike in long dated yields, although some say the huge UK energy plan’s impact on long dated gilts was behind the sell-off.

Another Corporate Hybrid issuer tenders for bonds

Followers bond tenders for Merck KGAA and Heimstaden Bostad, Fastighets AB Balder came out with a tender for two of its corporate hybrids for a total of EUR 85m. The company is a Swedish Homebuilder. Real Estate Corporate Hybrids were some of the largest underperformers in July 2022 and to this day, many of the sector’s bonds trade below the lows seen during the pandemic.

EU IG primary market crossed €1tn issuance YTD

HY primary market - Norton issues upsized bond

In the US HY market, Norton Lifelock (formerly Symantec) broke a 3 week duck in bond sales and managed to sell $1.5bn which was upsized from $1.2bn. Meanwhile in the loan market.

EM HC issuance markets waking up tentatively

Better quality Asian issuers are coming to market, e.g. Indonesia already issued this week and Korean Air is likely to come. Indonesia received more than $9b of Orders for its $2.65b 3-Part Bonds. EM new issue markets have been quieter than even DM HY markets, which is really saying something!

*IG*

EUR IG Corp Credit spreads still elevated, near pandemic highs

Kraft Heinz Affirms Full Year 2022 Guidance, Reduces Leverage Target

Extracts: "The Company has updated its long-term net leverage target ratio from consistently below four times to approximately three times. With interest rates 100% fixed with a weighted average maturity of 14.5 years, and leverage meaningfully improved, the Company believes this level will provide Kraft Heinz with a strong balance sheet through cycles and sufficient financial flexibility.” Kraft expects Adjusted EBITDA growth of 4% to 6% for FY 2022. Source: BBG

EIG Global to Buy Stake in Repsol Upstream Unit for $3.4bn - BBG

Extract: “Spanish oil and gas giant Repsol SA is selling a quarter of its exploration and production division for $3.4 billion to a US private equity firm, in a dramatic downsizing of its exposure to fossil fuels. The deal is Repsol’s second divestment in recent months as the Madrid-based oil producer raises funds to help pay for low-emission projects while also reducing its cost of capital. Repsol was the first large oil company to announce a strategic push into renewable power.”

*HY*

UK HY credit trades well post Liz Truss Energy plan announcement

Energy sensitive HY sectors in Sterling advanced on the week after the announcement of Liz Truss’s UK energy plan. Bonds of Iceland and Asda appeared to be up around 5% over the week and there were smaller gains for Gym Operators (David Lloyd), Pubs (e.g. Stonegate) and Morrisons Supermarket.

United raised its 3Q revenue outlook, sends sector higher - Barrons

Extract: “United Airlines Holdings raised its third-quarter revenue outlook Wednesday citing continued strong demand following a “robust summer.” United now expects total operating revenue in the quarter to be up around 12% on 2019 levels, this is an increase from a previous forecast of 11%. Capacity expectations also improved to between 10% and 11% lower than 2019 levels, compared with an earlier outlook of 11% lower. “Exiting a robust summer, the company continues to see a strong demand environment,” United said in a filing.”

EnQuest Trading Update

North Sea Oil firm EnQuest provided a trading update, key highlights:

As at 31 August Net Debt reduced to $817.6m

The outstanding RBL was reduced to $90.0 million

Executed $33.4 million (4.0%) of buy backs of the October 2023 7% high yield bonds in July and August bringing the total outstanding at the end of August down to $793.8 million.

Apollo Cleared to Lend $700m to Bankrupt Airline SAS in ‘Unusual’ Deal - BBG

Extract: US Bankruptcy Judge Michael Wiles on Friday approved a $700 million financing package for SAS AB from Apollo Global Management, though he said features of the deal concern him. The financing, divided into two $350 million draws, will allow Apollo to convert the debt into stock in the bankrupt airline or participate in an equity raise tied to SAS’s eventual exit from Chapter 11 protection under certain circumstances. Wiles called the financing “unusual” and questioned whether it was legally viable.

Cineworld formally filed for Chapter 11

Extract of company statement:

Cineworld Commences Chapter 11 Cases with Approximately $1.94 billion in Debtor-in-Possession Financing Commitments to Facilitate a Significant De-Leveraging Transaction and Position Company for Long-Term Growth

Chapter 11 restructuring process expected to significantly reduce debt and strengthen Cineworld’s balance sheet and liquidity position

De-leveraging transaction will allow Cineworld to accelerate, and capitalise on, its strategy in the cinema industry

Chapter 11 restructuring process involves entities that are engaged in Cineworld’s US, UK and Jersey businesses; businesses in all other territories remain unaffected

Group cinemas remain open globally to guests and members; operations to continue without interruption

UK Housebuilders - Vistry to Buy Countryside in $1.4 Billion Cash, Stock Deal

Extracts of BBG article:

Countryside put itself up for sale in June after coming under pressure from activist investor Browning West, which began building a stake in the company in 2020 and has been calling for a breakup. Countryside rejected two previous bids from Inclusive Capital that valued it at about £1.47 billion, saying they undervalued the company.

“This proposed combination has a highly compelling strategic rationale,” Vistry Chief Executive Officer Greg Fitzgerald said in the statement. “It will create a leader in the partnerships housing sector, with the scale and expertise to accelerate profitable growth across both partnerships and housebuilding, and expand the delivery of much needed affordable housing across England.”

The Vistry CEO seemed to show his enthusiasm for the deal by buying 24,699 shares at around £8 this week.

*FINANCIALS*

DB’s Jim Red - "Financials completely skipped the rate hiking cycle and have directly priced in a recession"

h/t Octavian Adrian Tanase on Linkedin.

While this chart relates to financial equities, it helps to show the sentiment towards financials sector as a whole.

Note however that European Banks rallied on Friday after the ECB decision as they were given some benefit for the ECB’s rate hikes.

Sainsburys Bank issues double digit coupon T2 bond, trades up in secondary

Supermarket chain’s Bank subsidiary issued £120m 10.5Y Tier 2 bond with a 10.5% coupon which traded up 1-2 points in the secondary market. Transaction is expected to be rated Baa2. Sidenote: Sainsbury and Tesco shares prices hit a 52 week low before bouncing towards the end of the week.

Shawbrook owners put plans to sell the challenger bank on ice - CityAM

Extract: The owners of Shawbrook Bank have reportedly shelved their plans to sell the lender. PE firms BC Partners and Pollen Street Capital were seeking bids of around £2bn for the challenger bank, which specialises in lending to small and medium-sized companies. The Financial Times reported, however, that the firms had failed to attract offers near the desired amount, and have since decided to put the plans on ice.

Banco BPM called its €500m 4.375% T2 bond (largely expected)

*CHINA*

China Property Firms held onto gains on hopes of easing restrictions / more stimulus

Several China Property firms’ bonds held onto gains from the prior week and stocks reacted even better this week. The basis for the optimism seems to stem form the possibility of the removal of curbs on purchasing in several cities and tax concessions for property transactions. However, enthusiasm is limited due to the level of COVID lockdowns currently in place. There was a new Dollar bond priced for Zhengzhou Real Estate (a Government related entity) which raised $350m of 3yr bonds at 5.1%.

*EM*

Zambia seeks US $ 8.4bn debt relief through 2025: IMF - BBG

Extract: “Zambia wants US $ 8.4 billion in cash debt relief from this year through 2025, the International Monetary Fund (IMF) said in a report published on Tuesday that will set the tone for complex restructuring negotiations with creditors ranging from Chinese state-owned banks to eurobond holders.

The nation, which in 2020 became Africa’s first pandemic-era sovereign defaulter, finalised a deal with the Washington-based lender last week for a US $ 1.3 billion bailout and economic programme. The government is seeking to restructure its external liabilities that reached US $ 17.3 billion last year and the IMF report reveals for the first time the forecast economic parameters that will frame talks starting this month.”

Sri Lanka Sovereign Bonds sold off slightly in sympathy with this headline from Zambia this week.

China ready to play positive role on SL debt restructuring - FT.LK

China on Friday said it is ready to play a positive role on the restructuring of Sri Lanka’s foreign debt. “We are ready to work with relevant countries and international financial institutions to continue to play a positive role in supporting Sri Lanka’s response to current difficulties and efforts to ease debt burden and realise sustainable development,” Chinese Foreign Ministry Spokesperson Zhao Lijian said. He was responding to a question at his weekly briefing in Beijing whether China as a creditor nation has any comment to Japanese Finance Minister Shunichi Suzuki on Friday urging all countries that lent money to Sri Lanka, including China, to discuss the country’s debt restructuring. “China has paid close attention to the difficulties and challenges faced by Sri Lanka and we have provided help to Sri Lanka’s socioeconomic development to the best of its capacity. China supports relevant financial institutions in consulting with Sri Lanka for proper solutions,” Zhao added. China accounts for the largest share (44%) of Sri Lanka's outstanding bilateral debt which as at end 2021 was $ 10 billion.

Apollo Funds Complete Sale-Leaseback Transaction with GOL Airlines - Statement

Extracts: Apollo and GOL Linhas Aéreas Inteligentes announced the completion of a sale and leaseback transaction, involving one new Boeing 737 MAX 8 aircraft, between GOL and certain funds managed by Apollo affiliates and serviced by Merx Aviation. The aircraft was acquired by the Apollo Funds upon its delivery from Boeing in July 2022 and immediately placed on long-term lease to GOL.

*CREDIT TRADING*

Tradeweb August Volume stats

Total trading volume for August 2022 of $23.4tn

Average daily volume (ADV) for the month was $1.02tn, an increase of 13.0% YoY

Fully electronic U.S. Credit ADV was up 14.8% YoY to $3.5bn and European credit ADV was down 9.6% YoY (up 4.8% YoY in EUR terms) to $1.0bn

Credit derivatives ADV was up 95.0% YoY to $11.4bn.

Tradeweb captured fully electronic share of U.S. High Grade and U.S. High Yield TRACE of 13.2% and 5.2%, respectively.

MarketAxess August Volumes update

Highlights:

Strongest ever month of August, with $30.6 billion in total trading average daily volume (“ADV”), up 44%, driven by a 55% increase in U.S. Treasury ADV to $20.2 billion and a 27% increase in total credit ADV to $10.2 billion

The preliminary average fee per million for total credit was $168 per million in August, up from $166 in July

Open Trading® represented 37% of total credit trading volume, up from 35% in the prior yea

Record Eurobonds estimated market share of 17.8% on ADV of $1.0 billion

*RATINGS*

Fitch Revises EDF's Outlook to Stable; Affirms at 'BBB+'

Moody's has upgraded Vietnam's rating from Ba3 to Ba2

Credit rating agency Moody's has upgraded Vietnam's rating from Ba3 to Ba2 thanks to its growing exports and manufacturing sector, and changed its outlook from positive to stable. "The upgrade to Ba2 reflects Vietnam's growing economic strengths relative to peers and greater resilience to external macroeconomic shocks that are indicative of improved policy effectiveness," it said in a statement. Read more here.

*LINKS*

Oaktree’s Howard Marks’ latest - “The Illusion of knowledge”

Summary: “I’ve been expressing my disregard for forecasts for almost as long as I’ve been writing my memos, starting with The Value of Predictions, or Where’d All This Rain Come From in February 1993. Over the years since then, I’ve explained at length why I’m not interested in forecasts – a few of my favorite quotes echoing my disdain head the sections below – but I’ve never devoted a memo to explaining why making helpful macro forecasts is so difficult. So here it is…”