7 October Global Credit Wrap

2 year UST at 4.3%, rising instances of forced selling, new issuance ticking along with EM showing some strength

*TLDR*

MACRO

Fed speakers remain resolute in their desire to tighten financial conditions

Latest NFP data showed strength in the labour market, fading pivot talk again

Rates volatility persists and government bond markets ended in the red after NFP

2 Year UST now at 4.3%!

UK PM Truss did not signal any major change to the low-tax / high spending combo…which pressured Gilts again (long dated Gilt ETF -9.2% over 5 days)

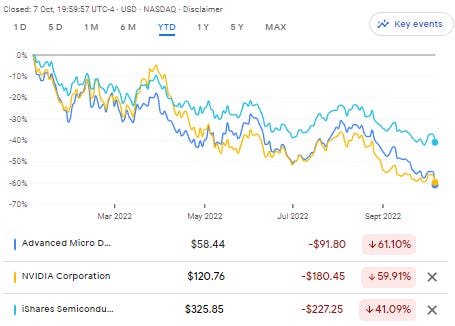

AMD and Samsung earnings show that Semiconductor sector is slowing

IG

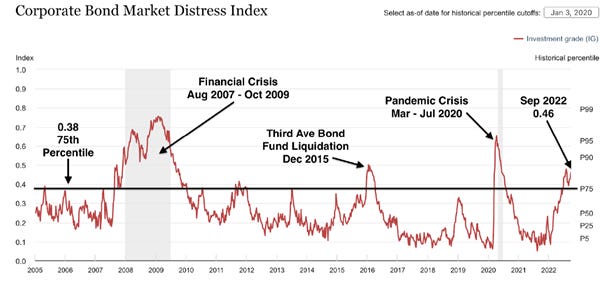

Fed’s Corporate Bond Market Distress Index shows more stress in IG vs HY

IG issuance picked up this week in US and Europe (€30bn priced in week)

Tesla upgraded to IG by S&P

HY

Two EUR HY companies could not pay their coupons/principal:

Metal Corp

Frigoglass

Notable news for Nordic issuers Jervois Mining, Waldorf and Copper Mountain

EM

Issuance picking up (Philippines, Saudi PIF, Czech Rail, Turkey Sukuk)

More ratings downgrades for EM Sovereigns (Pakistan and Bahamas)

FINANCIALS

Immense volatility and risk transfer in Credit Suisse paper

CS vol leaking into pricing of other financials - e.g. TD/AIB wide new issuance

CREDIT TRADING

Instances of forced selling going up in credit market

MarketAxess and Tradeweb report September figures

*MOVES OVER 5D*

CDS - All main indices closing tighter this week, in particular; HY CDX 36bps tighter, CDX EM 17bps tighter.

Cash Credit - Tightening bias this week across all major subsectors led by US HY which tightened in 71bps. HY Fund flows this week showed an inflow which might have helped spreads.

Bond ETFs - Long dated Gilts once again took it on the chin with Vanguard UK long Duration Gilt Fund losing 9.2% and IGLT losing 4.4%. On the positive side, loans (BKLN), HY (HYG/JNK) and BBBs (LQDB), EM Local (EMLC) posted gains of over 1% over 5 days.

*MACRO*

Fed speakers stuck with the hawkish script…(src - BBG weekly fix)

*DALY AIMS TO HIKE RATES AND HOLD, DOESN’T SEE RATE CUT IN 2023 *BOSTIC, ON SPECULATION OF RATE CUTS IN 2023, SAYS ‘NOT SO FAST’ *KASHKARI: WE ARE QUITE A WAYS AWAY FROM A PAUSE IN RATE HIKES *WALLER: HARD TO PAUSE FED RATE HIKES UNTIL INFLATION MODERATES

This is what is keeping risk assets down as the Fed wants to keep tightening financial conditions until inflation goes down meaningfully.

Australia’s RBA hikes less than expected, warns of increased financial stability risks

Australia’s RBA hiked by only 25bps which was less than what economists had predicted. This has got market participants asking if other central banks may follow a similar trajectory, seems unlikely the Fed will slow especially after the latest NFP.

The RBA Financial Stability Review stated that financial stability risks have increased globally and markets are stressed by synchronised policy tightening, geopolitical tension, higher USD and rising energy prices. RBA also stated that stability risks would be magnified by further substantial tightening in global markets and some households are already feeling the strain from higher rates which is likely to persist for some time. RBA

Weak economic data in particular from Spain and US

Spain services PMI dropped materially in September from 50 to 48.5, and was the fourth consecutive fall. The sharp fall shows that the current cost-of-living crisis is starting to hit very hard and spreading more widely. US ISM manufacturing was also weak, since it came in weaker than expectations at 50.9 from the prior month’s 52.8 and expected 52.2. Both employment and new orders both dropped into contractionary territory printing 48.7 (exp. 53.0, prev. 54.2) and 47.1 (prev. 41.3), respectively. The report showed that higher interest rates are starting to weigh on business investment sentiment, at least in the interest rate sensitive sectors. However, the inflationary gauge of prices paid declined to 51.7, which is the sixth consecutive month of falls.

Some forecasters expect NFP job additions to start tapering off too:

Corporate bellwethers slowing down ahead of official data - Chip sector this week

Samsung Electronics posted its first quarterly profit contraction in nearly three years as demand for microchips and electronic devices declined on high inflation and a global economic slowdown. The world’s largest memory chipmaker and smartphone producer estimated its operating profit for the three months to the end of September at Won10.8tn (US$ 7.7bn), down 32% from a year earlier.

AMD issued preliminary 3Q guidance well below its initial guidance. The semiconductor company also said its non-GAAP gross margin is expected to come in around 50%, while it had previously expected gross margin to be closer to 54%. AMD said the shortfall was a combination of a “weaker than expected PC market and significant inventory correction actions across the PC supply chain.” CNBC.

AMD shares are down 30% over 1 month, down 61% YTD but are up more than 300% over 5 years.

US Banks to report this week, as does Blackrock and Delta Airlines

This week sees the US earnings season fire up which will generate discussion and activity around whether earnings estimates have been cut enough and whether share prices have corrected enough.

Earnings week more towards end of the week with some huge US names reporting. Citigroup, JPMorgan Chase, Morgan Stanley, and Wells Fargo all report quarterly results before the market open on Friday. Thursday also looks interesting as a broad range of bellwethers report - Dominos Pizza (US Consumer), TSMC (Chips), Delta Airlines (Airlines), Blackrock (FS-Asset Management). Look out for the Blackrock earnings call to see if analysts ask about the LDI issues in the UK.

Sidenote: Keep a note of how many analysts say “great quarter guys” on the earnings calls.

Earnings calendar

EPS estimates

Analyst forecast cuts…but is it enough?

Key Macro Events this week - Monday closure/CPI/Fed Minutes (Barrons)

Monday 10/10 - Fixed-income markets are closed in observance of Columbus Day and Indigenous Peoples' Day. The New York Stock Exchange and Nasdaq keep regular trading hours.

Wednesday 10/12 - The Federal Open Market Committee releases the minutes from its late-September monetary-policy meeting. The FOMC at that meeting raised the federal-funds rates by three-quarters of a percentage point, for a third consecutive time, to 3%-3.25%.

The Bureau of Labor Statistics releases the producer price index for September. Economists forecast that the PPI will jump 8.4% year over year, after an 8.7% increase in August. The core PPI, which excludes volatile food and energy prices, is seen rising 7.2%, compared with 7.3% previously. The PPI spiked a record 11.7% in March and has since steadily, albeit slowly, declined.

Thursday 10/13 - The BLS releases the consumer price index for September. Consensus estimates are for a year-over-year increase of 8.1% for the CPI and 6.5% for the core CPI. This compares with gains of 8.3% and 6.3%, respectively, in August.

*NEW ISSUES / TENDERS*

New issuance ticking along despite sustained rate vol, Utilities are issuing again..

This week saw just over $13.5bn price in the US IG market with some interesting issuance from Enel which priced a 4 part SLB. Peak books were said to be around $15bn vs final issue size of $4bn. Large concessions were paid to get the deal over the line putting a halt to the trend of tightly priced green bonds. EDP (Portugese Electricity company) also issued in the Dollar market. Sticking with the Utility theme, EDF issued three tranches in the EUR IG senior market after a year’s absence. Seems the market has become a bit more comfortable with European utilities after a torrid couple of months for the sector. European IG clocked up nearly €30bn of issuance this week which is no mean feat considering the dreadful macro backdrop…

T-Mobile tapped the ABS market for the first time ever - BBG

T-Mobile sold $842m of ABS of which $750m was offered to investors at 90+UST interpolated curve. The bond was backed by customers phone loans, a structure which Verizon first came to market with in 2016. Fitch and Moody’s Investors Service are rating the T-Mobile transaction, and expect to award an ‘AAA’ grade to the largest tranche.

Wide issuance in the $ Financials market - AIB and TD

TD priced $1.75bn 60NC5 limited resource capital notes at 8.125%

BBG commented that just a year ago, Bank of Nova Scotia raised similar paper at 3.625%. LRCNs are deeply subordinated, non-deferrable, interest-bearing debt instruments with a term to maturity of at least 60 years and a non-call period of at least five years akin to AT1s. More here from Fitch.

AIB issued $750m of senior 4NC3 Fxd-to-FRN (Oct. 14, 2026) at +335 IPT which represented a coupon of 7.583%. Note that Irish comp Bank of Ireland issued senior Dollar paper only in September at 100bps tighter! AIB also is carrying out a tender offer on its 2023 $ paper.

EUR HY Name Tendam refinanced bonds two years early.

More tentative signs of life in the EUR HY market with Tendam, Spanish fashion retailer issuing bonds. The note priced with a discount and 7.5% interest plus euribor, taking the yield to the 10.75% region.

*IG*

Fed’s Corporate Bond Market Distress Index shows more stress in IG - Datatrek

Extract - This chart shows the CMBI for investment grade corporate bonds, where the market is clearly in an elevated level of distress. We have highlighted the 75th percentile line, which corresponds to a 0.38 reading. Aside from the 2008 Financial Crisis, the late 2015 liquidation of a credit fund at Third Avenue Capital and the 2020 Pandemic Crisis, the IG CMDI has never been higher than it is right now (0.46 reading, as noted below).

Bluechips US Corporate debt is taking the biggest losses since 2008

Taken from interview between BBG and Vanguard’s Co-Head of IG Credit.

*FINANCIALS*

Credit Suisse - What a week

A lot of CS paper appeared to change hands this week from outsized leveraged holders into more distressed/dedicated financials specialists. FINRA’s TRACE data estimated volume of $5.5bn across 6,200 trades in CS USD paper. The Swiss listed Credit Suisse share price closed the week +11.75% , this is after a Twitter rumour sparked fears that it was going to be a zero last week.

Credit Suisse has a lot of bonds outstanding, many of which were issued as recently as a couple of months ago. Glancing at the AT1 stack, it looks like bonds are closing the week between cash prices of 58 and the low 90s depending on the different resets/call dates. Yields on the 2026 to 2030 call dates range from 13% to 20%. The shorter calls are trading at huge YTCs due to the market belief that these instruments will not be called at the first call, e.g. the CS 23 call AT1 which trades in the high 70s.

Generically bonds look to be closing up 2-3pts following announcement of a series of bond tenders copying the playbook which DB followed in 2016 during its period of strife. The Treasurer at DB at the time (Dixit Joshi) is now the CFO at CS. He was previously at CS and Barclays as an MD. The rally in CS was given a second wind as there was a news late Friday that CS’s SPG unit is being pored over by potential acquirors; Pimco and Centerbridge.

Fitch: No Ratings Impact on UK Life Insurers’ Following UK Outlook Revision

Extracts: The recent revision of the UK’s Outlook to Negative has no immediate impact on UK life insurers’ ratings. Fitch expects the sector’s strong business profile and capital headroom to continue to underpin ratings in the hypothetical scenario of the UK sovereign rating being downgraded by one notch to ‘A+’. We also expect insurers’ investment concentration exposure to UK gilts to remain within rating tolerances.

The recent rapid drop in gilt prices, combined with downward movements in sterling relative to the dollar, triggered substantial collateral calls for some UK insurers on hedge positions. However, insurers hold strong liquidity buffers, which are stress-tested for various scenarios, including recent market events. Fitch expects insurers’ liquidity positions to have comfortably withstood the recent market volatility.

JPMorgan to call perps issued in 2008

JPM is calling its $3bn L+347bps perps that would've reset at the end of October ~7.625%. CUSIP: 46625HHA1. This one data point is further evidence that highly rated issuers would rather call expensive floating rated debt than leave it outstanding.

*HY*

EUR HY - Some issuers postponing repayment / agreeing to standstills on coupons

The tightening environment is having its impact on HY issuers with less access to funding markets. Metalcorp Group seeks to postpone the final repayment of its 7.0% Notes due October 3rd 2022. Reasons included 1) a counterparty reneging on a term facility and 2) an unplanned increase in working capital. Meanwhile, Frigoglass, the Glass and coolers manufacturer has agreed with a majority of bondholders for a standstill on coupon payments due in 2023 as part of a deal to ease its liquidity needs. Source: Co Q2 earnings report.

Diana Shipping gets $200m loan to fund new Vessel Purchases with Nordea

The purpose of the senior secured term loan facility is the partial financing of the nine modern ultramax dry bulk vessels, of which the Company expects to take delivery during the fourth quarter of 2022. Interesting to see some businesses finding it relatively easier to get funding in these tricky markets. Statement.

Norwegian Cruise Line (NCLH) liquidity was $2.2b at Sept. 30. - Seatrade Cruise

Extract: CFO Kempa said the company is talking with lenders to amend and extend facilities coming due 2023. Seventy-five percent of debt is fixed at a weighted average cost of 5%; in 2023, that goes up to 80%. At a time of rising interest rates, this is a positive.

Copper Mountain agreed to sell its Australian development project for up to $230m

Copper Mountain Mining has entered into a definitive agreement with regards to the sale of its fully-owned Eva copper project in Australia. Copper Mountain will receive USD 170m in cash on closing and payments of up to USD 30m dependent on copper prices and up to USD 30m dependent on volume. Closing is expected in Q1’23 and is subject to regulatory approvals and bondholder approval. The disposal is credit positive, and sizeable compared to its equity market cap ($279m) and its borrowings, which is why its bonds advanced 5-6 points following the news.

HY issuer Jervois Global opens only operational Cobalt mine in the US - TMH

Extracts:

Jervois Global will officially open its Idaho Cobalt Operations (ICO) mine site near Salmon, Idaho in the US today (7 October)

The mine is commencing a commissioning phase during October, with full nameplate capacity expected by the end of Q1 23

Once fully commissioned, Jervois’ mine will be the only primary cobalt mine in the US The company says the opening of the ICO represents a “significant milestone” in its strategy to become a major supplier of cobalt to the US

North Sea | Waldorf Production to acquire Dana Petroleum limited

Waldorf Production announced that Waldorf Energy Netherlands had entered into a definitive agreement to acquire Dana Petroleum Limited’s upstream business in the Netherlands. This comes in addition to the acquisition of TAQA Energy also announced earlier on in the week.

North Sea | Ithaca Energy looking at IPO - BBG

While the Energy market is on a tear, the IPO market is most certainly not, so it will be interesting to see if they get this one over the line. Extracts from BBG:

UK oil and gas producer Ithaca Energy Ltd. is preparing an initial public offering in London this year that could raise about $1 billion, according to people familiar with the plan.

A successful share sale in Ithaca would make it the largest in the energy sector since Norwegian company Var Energi AS’s $1 billion deal in February this year. The IPO market received a boost this month with the more than $9 billion offering of Porsche AG, potentially giving other companies waiting in the wings some confidence.

Theatre Group looks to refinance with a £1.2bn direct lending deal - BBG

Ambassador Theatre Group Ltd, which owns venues in the West End and Broadway, is looking to refinance its debt with a direct lending deal worth as much as £1.2 billion.

*EM*

EM issuance sees further momentum

EM issuance picked up, as the market tries to put a long barren spell for issuance behind it. Issuers that came to market included Philippines in USD, Saudi PIF, Turkey 3yr Sukuk and Czech Railways.

Ceske Drahy (Czech railways) priced EU500m 5Y Green at MS+300 to yield around 5.779% for a Baa2 rated credit. I do not follow this credit, but in the past Railways bonds have been an relatively stable area excluding of course the impact on Russian Railways and Ukraine Rail as a result of the war.

Moody’s Cuts Pakistan Rating as Debt Risks Rise After Floods

Could Pakistan follow Sri Lanka into debt restructuring? Pakistan was downgraded to Caa1 from B3 by Moody's on increased risks on liquidity, external vulnerability and debt sustainability ever since the floods hit in June. The floods have exacerbated liquidity and external credit weaknesses, with government revenue being hit severely. Forex reserves are only sufficient to cover less than two months of imports despite the recent US$ 1.1bn IMF disbursement. However Pakistan does have more “friendly nations” in the Middle East who could advance the nation money.

Romania hiked rates above consensus forecasts (75bp to +6.25%)

Sri Lanka holds rates as focus turns to reforms to stabilise crisis-hit economy - RTRS

Interesting tidbit re Kurdish oil, and comment on OPEC

Shamaran Petroleum announced it had changed the reference price for Sarsang crude oil sales payments from dated Brent to KBT (Kurdistan Blend) in order to reflect current market conditions for oil sales at Ceyhan. KBT trades at a discount to dated Brent. Kurdistan blend has had to compete with Russian oil which is being offered at a large discount.

Sidenote: This week’s OPEC meeting resulted in a disappointing outcome so far for the US. OPEC decided to lower production by more than expected, which effectively increased prices for the US. OPEC knows that the US needs to refill its SPR and that there is a midterm election around the corner. I can’t help but think that oil prices are well supported by a motivated OPEC and a well publicised need for the US to fill its SPR. WTI and Brent Crude were up 16.5% and 11.7% respectively over the last 5 days.

EM Inflation undershooting?

*RATINGS*

Fitch affirmed the UK at AA-; Outlook revised to Negative from Stable

Greece Affirmed at BB by Fitch

Fitch Affirms Romania at 'BBB-'; Outlook Negative

Moody's downgrades The Bahamas' ratings to B1, changes outlook to stable

Fitch Affirms International Personal Finance at 'BB-'; Outlook Stable

Moody's affirms AerCap's Baa3 ratings and revises outlook to positive from stable

Casino Downgraded to CCC+ by S&P

Fitch Affirms Harbour Energy at 'BB'; Outlook Stable

Fitch Affirms British Airways' IDR at 'BB'/Negative

S&PGR Upgrades Tesla Inc. To 'BBB-' From 'BB+'; Outlook Positive

Extract from BBG - Tesla scored an upgrade from S&P Global Ratings to BBB on Thursday, with analysts citing the electric-vehicle maker’s market leadership and “solid” manufacturing efficiency. That means that Tesla needs just one more upgrade from a major ratings provider to cinch overall investment-grade status — a milestone which Bloomberg Intelligence sees as just a matter of time. “S&P’s upgrade is the latest, but not the last for Tesla,” said Joel Levington, a Bloomberg Intelligence credit analyst. “We see its ratings eventually moving toward high BBB this year.

*CREDIT TRADING*

Credit volumes driven up by more instances of forced selling

Some of the best deals in credit come about due to the inefficiencies of the market and when there are forced sellers, e.g. credit downgrades or firms falling out of favour with a name (e.g CS) or something more technical (e.g LDI). This week there appeared to be selling down of Credit Suisse paper by accounts which simply owned too much of the name and then BBG reported that LDI Funds had been selling government and corporate bonds to shore up liquidity ahead of the end of the BoE’s intervention.

UK Pension Funds said to be dumping assets before end of BoE intervention - BBG

Extract - Pension funds were actively offloading their most liquid assets until Tuesday this week when selling abated, according to a senior banker, who manages bond sales for the UK government and for British and European companies. Much of the selling centered around European corporate bonds, US credit and US Treasuries, he said, asking not to be identified because the transactions are private. There has also been selling of collateralized-loan obligations, or CLOs, an investment that has been historically popular with pension funds, according to Aza Teeuwen, partner at TwentyFour Asset Management. Last week, more than 1.5 billion euros of CLOs were listed for sale, with more sold this week, he said in a note on Wednesday. Sales of CLOs in the last week-and-a-half could total more than the previous three months combined.

MarketAxess US HY market share increased in September - MKTX

If only MarketAxess’s share price had the same uptrend!

Other highlights include record week of trading at the end of September which drove 20% growth in total credit. Estimated market share of 20% across three major product areas (IG, EM and HY) in the month for the first time in history.

Tradeweb reports +17.2% YoY incease in ADV in September - Tradeweb

Extracts:

Fully electronic U.S. Credit ADV was up 25.6% YoY to $4.2bn and European credit ADV was down 15.3% YoY (down 1.6% YoY in EUR terms) to $1.7bn.

Record electronic U.S. High Grade activity was buoyed by record volume in both portfolio trading and Tradeweb AllTrade’s all-to-all offering. U.S. High Yield and European credit reported strong volumes into the end of the month following a lighter start of the month.

Tradeweb captured a record 14.5% share of fully electronic U.S. High Grade TRACE and 5.7% share of fully electronic U.S. High Yield TRACE.

*ESG*

Green bond sales hit 4 month high - BBG

Extract - Companies and governments around the world raised more than $54 billion in green bonds last month, compared with more than $35 billion raised in August, data compiled by Bloomberg show. That’s despite overall bond issuance in the US and Europe dropping significantly in September as central banks across the globe stepped up their battle against inflation.

This is quite interesting in light of how weak the flows for mainstream credit assets were. Suggests to me that there is still a decent amount of AUM dedicated to ESG in Fixed Income.

Cemex closed a €500m Sustainability Linked Loan

Extract - (Bloomberg) -- Cemex said in a statement it closed a new 500m euro three year sustainability-linked term loan.

Proceeds will be used to repay other debt, the company said

The loan increases “the amount of debt that is linked to the company’s Future in Action strategy and its ultimate vision of a carbon-neutral economy”

*LINKS*

The 10-Year treasury bond is on pace for its worst year ever (-16.7%) - Charlie Bilello

…and a 60/40 portfolio of the S&P 500 and 10-Year bond (-21%) is on pace for the 2nd worst year ever, trailing only 1931.

Bill Gross & Pimco believe rates are peaking and that bonds are attractive - BBG

Pimco beating the drum to buy bonds:

-Core Bond Funds ‘Quite Positive’ in Medium Term: Pimco’s Balls

-Pimco's Crescenzi: Bonds Increasingly Attractive Amidst 'Volckeresque' Fed

That Sound You Hear Is the Fed Breaking Something - Guggenheim Investments

This is a super read…

Cute list ranking the aggressiveness of PE firms and their deals

H/T Octavian Adrian Tanase

Office REITs just took out their March 2020 low - Jim Bianco

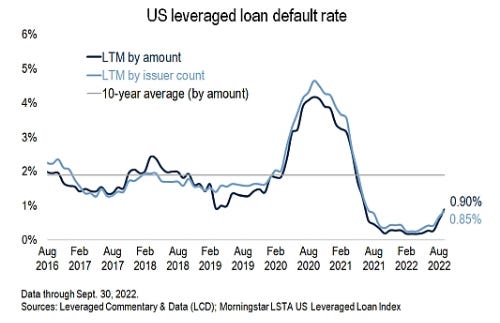

Leveraged loan default rate, distress ratio climb amid volatility - Pitchbook

When will this feed through to official inflation economic statistics?

These summaries are Gold!