29 July 2022 - Global Credit Wrap

Earnings, inflation debate, strong July for DM Credit...

*TL: DR*

RECENT MARKET RALLY:

Bear market rally or the start of a bigger move higher? - This is the trillion Dollar question to which I do not have the answer! However, I would pose the following questions/thoughts regarding this rally in Credit:

How much of it is down to dealer positioning? - i.e. light positioning during Summer, “drying up” of sellers at unrealistically low levels resulting in a squeeze higher.

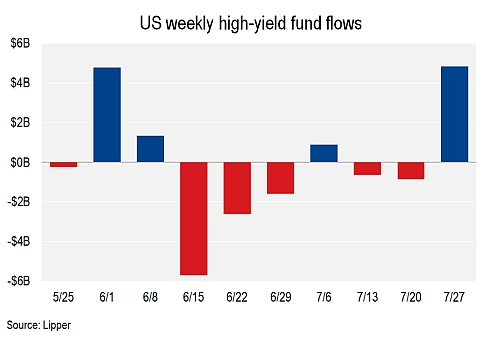

How much volume is behind this rally? - Just looking at HY, seems there appears to be volume behind the move based on this week’s flow numbers (US high-yield retail funds posted $4.83B inflow)

Large parts of the market belief in an early Fed Pivot - While its hard for one to argue against the size of the moves in this market, a lot of the narratives from Corporates this week has been of higher costs, but also a theme of passing on those costs to consumers. Furthermore, the Energy situation remains largely unresolved particularly in Europe.

Behaviourally when investors see positive returns, it tends to increase participation…

Thawing new issue /funding markets suggest confidence is increasing

For the rally to be sustained…I think several things need to line up - lower rates volatility, aggregate inflation stats cooling off, OK corporate profitability, improvement investor participation and a “shallow” recession.

INFLATION:

Despite the market getting excited about a possible decline in inflation, a number of corporate earnings suggest inflation is still a problem. Furthermore, many companies are passing on higher costs onto its consumers (e.g. McDonalds, Amazon, Unilever, Reckitt).

NEW ISSUES/TENDERS:

The new issue pipeline continues to thaw, particularly in IG. A number of companies came to market including Kinder Morgan (10 and 30 year), GM (Green bond) and SSE (Green bond). Outside of public bond markets, there was a financing done for HY European Telecom - Iliad. Oil companies continue to use their large FCF to retire debt (BP, DNO).

CYCLICALS:

Several Airlines/Cruiselines posted profits for the first time since the pandemic (Air France, United Airlines, IAG and Royal Caribbean) and reported strong liquidity positions

Autos posted solid earnings results - Stellantis, JLR, Ford, Mercedes and VW were just some of the companies that reported earnings that impressed analysts. JLR indicated a more positive outlook due to more chip availability

FINANCIALS:

UK/European Banks’ earnings on the whole have been better than expectations.

Private Credit / Asset Management firm Ares Capital Corp said that it has $91bn of drypowder to invest…

EM:

Flows picture in EM remains dreadful, which could be why EM Bonds are not in turbo-rally mode like DM Credit in July. The IIF via the FT pointed out that EM (Equity + bond) outflows over the past five months have risen to more than $38bn — the longest period of net outflows since records began in 2005!

Some notable LATAM corporates reported earnings: Pemex, Cemex and Gol Airlines

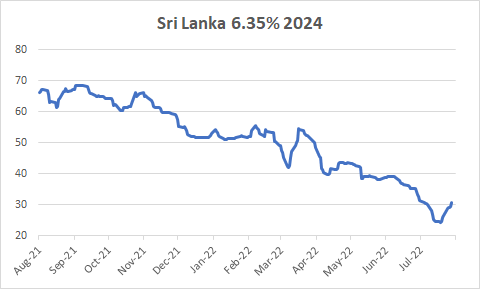

Nice little bounce in Sri Lanka Sovereign bonds on very little news. Pakistan continues to be a topical name as it looks to secure IMF financing.

*KEY MOVES*

My feeds are playing up this weekend, so I will stick to bond ETF moves only. Month to date to 29 July this was the scorecard for ETFs I monitor:

TLT +2.4% - 20+ year Government bonds

IEAC 5.4% - European IG Credit

LQD +4.4% - US IG Credit

IHYG +6.6% - European HY

HYG +6.7% - HY US Credit

JNK +6.8% - HY US Credit

AT1 +5.8% - Bank CoCos

EHYB +8.3% - European Corporate Hybrids

EMB +3.6% - EM HC Sovereigns

CEMB +1.7% - EM HC Corporates

The strength in Fixed Income assets has been tilted mainly towards Developed Market (“DM”) Fixed Income. Within that, DM Credit has been a big beneficiary with European Credit and US HY leading the way. The “outsized” move in European Corporate Hybrids maybe due to a reversal of June’s “buyer’s strike” related losses. Recall, this was when the REITs Corporate Hybrid sector became “bidless” and when weakness spread to other sectors with sound fundamental backdrops like Energy and Telcos.

EM has lagged DM in July. A number of reasons could explain this difference including - record outflows (see below in EM section), higher level of current defaults/restructurings, exposure to Ukraine (which just announced a debt extension) and less of a clear connection to Central Bank actions unlike say US or European Credit.

*MACRO*

Decent summary of the Fed Meeting that took place last week:

Bonds rally on Fed Pivot belief…

Bloomberg covered this topic well. Extract of the article:

Peak inflation may or may not be here, but bonds are leading the way in declaring that the top is in for aggressive central bank tightening.

Global bonds are set for their best monthly gain since 2020, bouncing back from a record slump in the first half of 2022.

Fed's preferred yield curve drops at record pace from its peak

Bonds had already started pricing in a recession. A Powell-favored part of the yield curve is flattening at a record pace to sound the alarm.

Real yields check up…

Looking beyond the definition of recession…

Confidence issues…

Swiss National Bank lost CHF 48.7bn on foreign interest-bearing paper and instruments - SNB

Samsung’s Profit Is Latest Tech Casualty to Recession Fears - BBG

Extract:

“The world’s largest producer of smartphones and displays reported a less-than-expected 16% rise in net income, reflecting how it’s still navigating rising uncertainty around a potential global recession. Revenue from its semiconductor division, which as the world’s largest producer of memory is an indicator of electronics demand, missed analysts’ estimates by about 22%.

Samsung warned of weakening demand for PCs and mobile phones in the second half of the year, joining a growing cadre of tech giants sounding the alarm over global economic uncertainty”

Note, Best Buy echoed similar bearish sentiment on consumer electronics:

“As high inflation has continued and consumer sentiment has deteriorated, customer demand within the consumer electronics industry has softened even further, leading to Q2 financial results below the expectations we shared in May.” - CEO of Best Buy

* INFLATION / COMMODITIES*

Amazon Prime Plans Inflation-Busting 31% Price Hikes in Europe - BBG

The annual price of the free-shipping service will increase to £95 ($114.06) from £79 in the UK starting from Sept. 15, the company said in a statement on Tuesday. Prices will jump by 31% on average across the affected European countries and follows similar hikes in the US announced in February.

Amazon highlights various inflationary cost aspects on its earnings call

Extracts:

Electricity - “Our macroeconomic issues are principally on inflation, and we've been pretty transparent on that. I think the new thing this quarter is additional pressure on the energy electricity rates in our data centers because of the ramp-up in natural gas prices”

Wages #1 - “AWS operating income was $5.7 billion in Q2. As a reminder, this includes a portion of our seasonal Q2 step-up in stock-based compensation expense. AWS results included a greater mix of these costs, reflecting wage inflation in high-demand areas, including engineers and other tech workers as well as increasing technology infrastructure investment to support long-term growth.”

Wages #2 - “Other cost pressures are principally on our cost and employees. If you look at our stock-based comp as a percent of revenue, it's gone up 150 basis points quarter over quarter as we stepped up from Q1 to Q2. We see that pattern every year, but we don't see that magnitude, and that's where a lot of our wage inflation is for, particularly our technical employees”

Iceland Supermarket - Will be hit with £140m bill to run its freezers this year

Extract: “Iceland is set to see soaring energy bills this year because a third of its sales are frozen food. According to money experts, Iceland’s profits this year could fall below £100m, compared with £126m last year, as it will not be fully able to pass on the increasing energy costs” - Retail Gazette

BT’s profits were helped by it raising tariff prices above inflation earlier in the year.

Higher Menu Prices Lift McDonald’s U.S. Sales but Consumer Outlook Uncertain - WSJ

McDonald’s on Tuesday said higher prices and value menu offerings pushed same-store sales up 3.7% in the U.S. from last year’s period, outpacing analysts’ expectations.

Reckitt Raises Forecast as Shoppers Absorb Higher Prices - BBG

The maker of Lysol and Dettol cleansers said sales growth will be in a range of 5% to 8% this fiscal year, up from a previous guidance of 1% to 4%, according to a statement.

Unilever hikes prices for products due to inflation, expects strong sales - Business Standard

“The makers of Coca-Cola beverages, Dove shampoo, Huggies diapers and Big Macs have been raising prices as their costs increase on everything from wood pulp to wages” - WSJ

Miners encountered higher costs in Q2

Newmont Corp on Monday raised its annual cost forecast and warned that inflationary pressures would persist into 2023 after its second-quarter profit missed Street estimates, sending the world's biggest gold miner's shares down 12% - Reuters

Rio Tinto - ..$8.9 billion of net earnings, 28% lower than 2021 first half, reflected the movement in commodity prices, the impact of higher energy prices on our operations and higher rates of inflation on our operating costs and closure liabilities. -Rio Tinto

First Quantum - First Quantum reported a $0.13/lb quarter-on-quarter increase in C1 cash costs to $1.74/lb, as inflation drove up the prices for consumables, including explosives, fuel and steel, and freight charges climbed - Mining weekly

The United States became the world’s largest LNG exporter in the first half of 2022 - EIA

In certain respects, the USA has been a key beneficiary of the Ukraine/Russia war, i.e. stronger Dollar and higher LNG exports.

Shell Says Plan for North Sea Gas Project Will Proceed - Link

Extract: “Shell plc stated Monday that it’s transferring ahead with its Jackdaw natural-gas growth within the North Sea, saying the mission—which has been opposed by environmental teams—might produce greater than 6% of anticipated U.Ok. North Sea gasoline by mid-decade.”

*NEW ISSUES / TENDERS*

UK Utility SSE issued a 7 year green bond that was 9x oversubscribed - Statement

Company: SSE plc has successfully issued a €650m 7-year green bond maturing 1 August 2029 at a coupon of 2.875 per cent. Notwithstanding the current challenging market conditions, today’s new green bond has been extremely well received, and was considerably oversubscribed

Eni Signed EU6b Sustainability-Linked Revolving Credit Line

The iliad Group (Telco) puts in place three new financing facilities representing an aggregate €5 billion - Link

Extract: The iliad Group has successfully placed three bank financing facilities, representing an aggregate €5 billion, with a pool of 23 leading international banks. This operation has enabled the Group to strengthen its financial structure, increase its liquidity and extend the average maturity of its debt. The significant liquidity available under the facilities will help support the Group’s growth and development.

UK Bond Market Finishes Slowest July on Record - BBG

One firm is currently marketing a deal; Annington Ltd., one of the biggest private owners of residential property in the UK, is marketing a sterling benchmark-sized note due in 11 years.

BP Announces Redemption of $2.85b of Outstanding Notes - Release

DB 4-part tender offer for senior $ notes - DB

Kurdish oil firm DNO bought back 25.2 million of its 2024 bond after calling $200m of its bonds earlier this year - Statement

*IG*

The “bear market” in Walmart shares seems short lived!

*HY*

US high-yield retail funds post $4.83B inflow, largest in 2 years - S&P Global

Extract: “U.S. high-yield retail funds reported inflows of $4.83 billion for the week to July 27, or the largest positive weekly reading since the period to June 10, 2020, according to data from Lipper. “

Note that Loans and Investment Grade saw outflows in the same week.

US HY sector having a great July 2022 despite recession talk

Jaguar Land Rover reports sound liquidity position expects chip supply situation to improve - Statement

Semiconductor related production constraints compounded by slower than expected production ramp up of New Range Rover and Range Rover Sport

Covid-19 lockdowns in China also impacted production and sales in the quarter

Loss before tax of £(524)m, excluding an exceptional £155m pensions benefit but including £(236)m FX and commodity revaluation year on year

Demand remains strong with a record 200,000 client orders, with Range Rover, Range Rover Sport and Defender accounting for over 60% of client orders.

Liquidity of £5.2 billion, including £3.7 billion cash at June 30, 2022 and £1.5 billion undrawn revolving credit facility from July

Outlook: Financial performance is expected to improve significantly over the year with chip supply expected to improve….as well as ramping up New Range Rover and Range Rover Sport production.

We continue to target achieving a 5% EBIT margin and £1 billion positive free cash flow in FY23.

Our medium- and longer-term financial targets…include improving EBIT margins to 10% or more by FY26 and improving free cash flow to achieve near zero net debt by FY 24.

Ford H1 2022 figures were better than market expectations

Ford posted revenue of $40.2 billion on a 35% increase in wholesale shipments together with favorable pricing and vehicle mix.

Company net income was $667 million, a margin of 1.7%, which included a mark-to-market loss on Ford’s stake in Rivian.

Adjusted earnings before interest and taxes was $3.7 billion, an adjusted EBIT margin of 9.3%.

Operating cash flow was $2.9 billion and adjusted free cash flow was $3.6 billion, with solid automotive EBIT of $3.3 billion.

Ford ended the quarter with $29 billion in cash, $45 billion in total liquidity and the persistent financial strength and flexibility to fund Ford+ priorities.

Pimco bought second tranche of Morrisons Supermarket paper at a discount - BBG

Extract: “Pimco took the lion’s share of the 800 million euros of loans, priced in the mid-to-high 80s, that banks offloaded, according to people familiar with the deal who asked not to be identified because the transactions are private. The remaining 200 million euros was sold to funds, they said, without naming them.”

Moody's: Acquisition of Spirit Airlines will strengthen JetBlue's business profile, increase leverage…

….though closing not expected before 2024. Moodys: JetBlue Airways Corp.'s Ba2 and Spirit Airlines, Inc.'s B1 corporate family ratings are unaffected by the companies agreement to merge announced on July 28, 2022. JetBlue will acquire Spirit in an all cash transaction valued at $3.8 billion. The acquisition of Spirit would be a leveraging transaction, a credit negative. However, the DOJ's stance on the transaction is uncertain and the companies expect that the transaction would not close before 2024.

Above extracts from Moodys’.

Fortescue Posts Third Consecutive Year of Record Exports - MarketWatch

"Fortescue's outstanding operating performance continued in 4Q FY22, with mining, processing, rail and shipping combining to deliver record shipments of 189.0 million [metric] tons in FY22, 4% higher than FY21 and exceeding the top end of guidance of 188.0 million tons. FY22 represents the third consecutive year of record shipments, reflecting strong performance across the entire supply chain and the successful integration of Eliwana which commenced operations in January 2021."

Airline IAG reports robust liquidity position and returns to profit in Q2 following strong recovery in demand

Profit after tax and exceptional items for the second quarter €133 million

Net debt at June 30, 2022 was down €688 million since December 31, 2021 to €10,979 million, reflecting the seasonal benefit on cash of bookings for travel in the second half of the year

Total liquidity increased to €13,489 million (December 31, 2021: €11,986 million)

“We see a very strong yield, and we see demand recovering and load factor increasing,” IAG Chief Executive Officer Luis Gallego said on a media call. While visibility deeper into the year is limited to key dates such as Christmas, “what we see is very strong,” he said.

BA dismissed 10,000 workers during the coronavirus pandemic. The UK carrier hired 4,000 people this year to help fill the gap, 80% of whom are now in operational roles, according to Gallego. It has also poached KLM’s chief operating officer to help improve operational resilience.

Air France figures better YoY, leverage down meaningfully

Revenues +144% to €6.7bn (vs. €6.2bn BBG)

Net Income €324m (vs. €39m BBG)

Adj Op FCF €1.5bn (+€1.3bn vs. 2Q21)

Net Lev 2.6x (vs. 5.4x 1Q22)

Air France-KLM had €11.9 billion in liquidity available at the end of June

Royal Caribbean H1 - Return to positive cash flow, liquidity of $3.3bn

Extracts of statement

Second quarter results were meaningfully ahead of the company's expectations driven by accelerating and strong close-in demand, further improvement in onboard revenue and better cost performance.

We reached two important milestones in our recovery this quarter – returning our entire global fleet back to operations and delivering positive operating cash flow and EBITDA

Load factors in the second quarter were 82% overall, with June sailings reaching almost 90%.

Based on the continued strength in consumer demand, the company expects load factors will average approximately 95% in the third quarter and increase to triple digits by year-end.

Booking volumes received in the second quarter for the back half of 2022 sailings remained significantly higher than booking volumes received in the second quarter of 2019 for the back half of 2019.

The second half of 2022 is booked below historical ranges but at higher prices than 2019, with and without future cruise credits (FCCs).

For 2023, all quarters are currently booked within historical ranges at record pricing.

For the third quarter of 2022 and based on current currency exchange rates, fuel rates and interest rates, the company expects to generate approximately $2.9 billion - $3.0 billion in Total Revenues, Adjusted EBITDA of $700 million - $750 million and Adjusted Earnings Per Share of $0.05 - $0.25.

RE Liquidity & short term maturities: ”As of June 30, 2022, the Group's liquidity position was $3.3 billion, which includes cash and cash equivalents, undrawn revolving credit facility capacity, and a $700 million commitment for a 364-day term loan facility. During the second quarter, the Group generated operating cash flow of approximately $0.5 billion. The scheduled debt maturities for the remainder of 2022 are $1.6 billion.”

*FINANCIALS*

European Bank Earnings season in one Tweet:

Ares Capital Corp earnings highlights - Seeking Alpha

Extracts:

“Approximately 64% of our invested assets are in credit investments,

While every cycle is different, I would note that the direct lending asset class outperformed other credit investments such as high-yield bonds, syndicated bank loans and investment-grade bonds during the past two full cycles, encompassing the Fed tightening, recession and recovery.

Our credit portfolio also provides meaningful benefits to both our fund investors and Ares during rising interest rate environments as roughly 90% of our credit group debt assets are in floating-rate instruments.

Within our significant funds in credit, our direct lending credit strategies continue to outperform liquid market alternatives. Ares Capital Corporation generated a net return of 1.2% in the second quarter and 13.4% for the last 12 months. Similarly, our two largest direct lending strategy composites in the US and Europe also had steady returns. Our US senior direct lending strategy had a gross return of 2.3% for the second quarter and 15.5% for the last 12 months and our European direct lending strategy generated gross returns of 2.6% for the quarter and 11.3% for the last 12 months.

Our dry powder of $91 billion provides a significant opportunity to deploy in an increasingly attractive investing environment.

[Re how pricing has evolved this year]… if you were to look at the market today factoring in OID and credit spread adjustment and the new SOFR environment, first lien loans in the middle market are probably somewhere in the 500 to 550 range with 90 to 95 OID. So kind of pricing 7% to 875 [ph] all-in for first lien piece of paper. That's significantly wider than we saw coming into the beginning of the year.”

Paragon Grp of Companies -Q3, credit quality of loan book remains "exemplary."

Extract: “The Group has delivered another strong performance over the quarter in line with the Board’s expectations with continued momentum in lending volumes, improved margins and an exemplary credit performance.”

Credit Suisse hires a New CEO, changes are afoot..

CS says it will carry out comprehensive strategic review

Costs cuts may include further shrinking of IB.

Targeting ~ at least another CHF1bn of cost cuts and evaluating its securitized products trading unit.

Said it wants an IB that uses less capital and is more tied to its wealth franchise

CS experienced net outflows of CHF7.7bn

*EM*

Emerging markets hit by record streak of withdrawals by foreign investors - FT

Extract: Foreign investors have pulled funds out of emerging markets for five straight months in the longest streak of withdrawals on record… Cross-border outflows by international investors in EM stocks and domestic bonds reached $10.5bn this month according to provisional data compiled by the Institute of International Finance. That took outflows over the past five months to more than $38bn — the longest period of net outflows since records began in 2005.

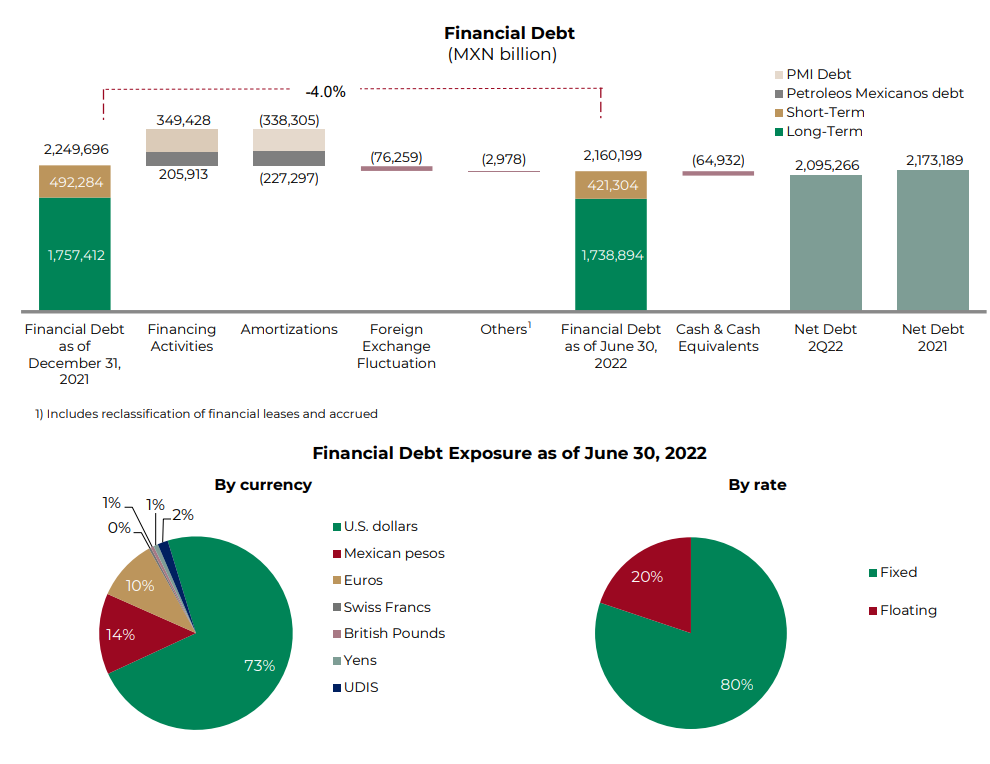

Pemex H1 2022 - Improvements in sales, ebitda margins and lower debt

Total revenue +32% q/q mainly due to high crude oil prices

Upstream EBITDA +26% q/q, in line with crude yet offset somewhat by higher cash costs at US$29/bbl.

Downstream refining utilization rates were stable at 49%, with revenue +33% q/q from higher prices and volumes sold. Note that downstream EBITDA was breakeven in 2Q22 which is the first time since 2018.

Consolidated EBITDA +23% q/q to US$14 bn with an EBITDA margin of 42%.

Though FCF burn was US$4.1 bn from higher capex and WK expansion, it was offset by Govt. tax credits related to downstream subsidies and Govt. contributions. As such, net debt decreased q/q with the annualized net leverage ratio improving to 1.9x.

Total financial debt decreased by 4.0% as compared to December of 2021

Despite the implicit backing of the Mexico Sovereign and robust oil prices many of Pemex’s bonds trade on double digit yields beyond the 7 year tenor.

Cemex reduces its debt load, gets closer to IG rating

Q2 reports - Slide deck quite useful for credit investors

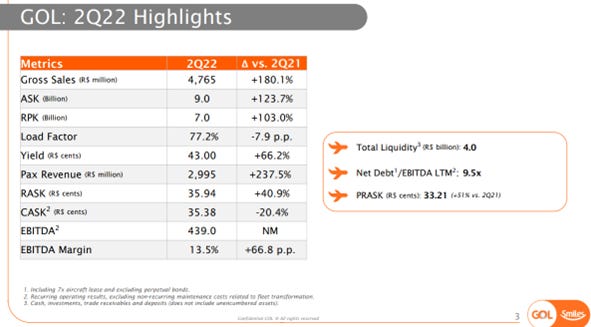

Gol Airlines reports Q2 Figures

Key takeaways:

Liquidity up to BRL 4bn now

Leverage remains elevated (9.5x ND/EBITDA), but is expected come down by early 2023

Gol stated that seasonally, second half of year is stronger, particularly Q3

Earnings in Q2 were affected by higher oil prices and weakening BRL

Some of the higher oil prices were offset by more efficient planes (~8%

reduction in fuel consumption per flight hour mainly due to 737 max)

Bahamas Gov’t hires Rothschild for $11.8bn debt help - Tribune

Extracts: “The Government has hired Rothschild & Co, a major global financial group, to advise on what could become a “massive refinancing” of much of the country’s $11.8bn national debt, it was revealed yesterday.”

Fitch, Moody’s Expect Pakistan to Get $1.2 Billion From IMF - BBG

Extract: “Pakistan is expected to secure $1.2 billion from the International Monetary Fund, which may help ease pressure on the nation’s currency and bonds, according to Fitch Ratings and Moody’s Investor Service. “We assume IMF board approval of Pakistan’s new staff-level agreement” with the lender, said Krisjanis Krustins, a Hong Kong-based director at Fitch. “This will unlock significant additional financing from the IMF and other multilateral and bilateral sources and may well provide a significant confidence boost to the markets.””

Sri Lanka Sovereign Bonds +5pts off the lows on no real news

Feel free to comment below if you have any views on why Sri Lanka Sovereign is rallying other than “more buyers than sellers.”

*CHINA*

China Evergrande offers restructuring principles as debt crisis grows - Business Times

“CHINA Evergrande Group, the world’s most indebted developer at the centre of a broader debt crisis in the country’s property industry, unveiled preliminary principles for the restructuring of its offshore debt. The company said that it will offer some assets outside of China to repay creditors including shares of its electric vehicle and property management services, adding that it plans to announce a full restructuring plan within 2022, according to a filing. “

*RATINGS*

S&P cuts Pakistan's credit outlook to negative

Georgia Affirmed at BB by Fitch

Italy - S&P has revised its outlook from positive to stable, BBB rating affirmed

Ukraine cut to CC from CCC+ by S&P

Albania Affirmed at B+ by S&P

Fitch Downgrades Ukrainian Railways to 'C' on Sovereign Rating Action - Fitch

Fitch Downgrades 25 Turkish Banks; Outlook Negative - Fitch

Follows Sovereign downgrade.

Intermediate Capital - S&P raised its credit rating to BBB, outlook stable.

Alcoa Wins Back Investment-Grade Status in Moody’s Upgrade

Alcoa has secured its second investment-grade rating Moody’s gave Alcoa’s bond-issuing subsidiary a score of Baa3

S&P AFFIRMS SOUTHWEST AIRLINES 'BBB' RTG; OUTLOOK POSITIVE

Moody's Downgrades Bausch Health Companies Inc.'s CFR to Caa1; Outlook Negative

Teva Outlook to Positive by S&P; L-T Rating Affirmed

S&PGR Affirms Uniper 'BBB-' Ratings; Outlook Negative

Hovnanian Upgraded to B- by S&P, Outlook Stable

S&P AFFIRMS BOEING CO. RTGS; OUTLOOK NEGATIVE

*LINKS*

PCE broken down into its components

German container liner Hapag Lloyds is raising expectations for 2H 2022

Oaktree - Performing Credit Quarterly 2Q2022

Oaktree with its comprehensive review of various sub sectors within credit and its outlook each of those same sectors. Some good charts in there like this one:

TwentyFour AM asks the question - What is the AT1 market pricing in?

This interesting note touches on a number of topics including; how current levels in the AT1 sector compare to previous sell-offs, touching on NIMs and cost of risk from banks that have reported and extension risk.

TwentyFour AM -Why 85 is the new par in HY

Good post here speaking about recent deals in the European HY market and state of the market including this fact: “The weighted average price of all the bonds included in the ICE BofA European High Yield index was 85.6 at the end of June

PwC Debt Watch Europe Q2 2022 Review "

A document with some good charts like the one below:

Thanks, I appreciate your exhaustive summary! Best