28 April 2023 Global Credit Wrap

Issuance ticking along in HY/IG, Bank results were ok, FRC problem lingers, Insurance debt redeemed, EUR RE APO/Vonovia transaction

*TLDR*

MACRO

Hedge funds are short US Treasuries, Asset Managers taking other side of the trade

US Jobless claims came in lower than expected:

Which represented a change from the last few weeks of upwards surprises.

The US labor market remains tight which challenges the assumptions of rate cuts towards end of ‘23/early ‘24

More job cuts in Cloud, Recruitment, Media & Banking sectors

PwC is making a $1 billion bet on business AI

US GDP for Q1 preliminary report came in significantly below expectations but still showing growth of 1.1% (Exp. 1.9%, Prev. 2.6%) h/t @macro_dose

German inflation slows unexpectedly after economy stagnated (Bunds rallied)

UK consumers absorbing Food price rises but Energy Bills’ debt rising

Japan's Life Insurers sticking to plans to reduce currency hedged foreign debt

INFLATION

Sov Inflation:

US Core PCE price index came in as expected at 4.6% YoY (Prev. 4.7%).

US Headline PCE came in light at 4.2% YoY (Exp. 4.5%, Prev. 5.1%)

US Employment Cost Index (ECI) came in higher than expected at at 1.2% (Exp. 1.1%), adding to the case for the Fed to keep hiking

Australia 1Q Trimmed Mean CPI Inflation came in light vs expectations

Singapore Core Inflation Slows as Food Prices Come Off Highs

Annual EZ Inflation eased to 6.9% in March from 8.5% the month before

But EZ core inflation (excludes food and energy prices) hit a record 5.7%

UK Govt gets record demand for Inflation linked Gilts

Corporate Inflation:

Chipotle paying less for avocados

Nestlé pushed up prices by an average of ~10% in the first 3 months of the year

Michelin CFO Sees Smaller-Than-Expected Inflation Hit This Year

Danone CFO sees inflation tailing off this year

IG

IG new issue summary - $65.7bn in US IG & €127bn in EUR IG in April

Cyclical issuers issuing in the IG market, e.g. Aircraft Lessors

FINS

AT1 bonds called for Lloyds & Unicredit, ease fears somewhat for AT1 market

DB is cutting its 2023 issuance plan due to higher borrowing costs

Investec Bank upsized its Syndicated Term Loan due to strong demand

Old style insurance bonds see more than $3bn of tender activity

Swiss regulator says two banks' crisis plans are insufficient - RTRS

CS & AT1News Recap

Fins Earnings recap and notable Equity moves

First Republic in trouble:

First Republic is the 14th largest bank in America—larger than Silicon Valley Bank was and would be the 2nd largest bank failure in US history: Joe Politano.

First Republic auction underway, with deal expected by Sunday | RTRS

HY & Lev Loans

US HY Issuance trends - $18.8bn priced in April 2023

European HY Issuance highlights - Around €3bn priced in the week

Bankruptcies:

68 large bankruptcies in the US as at 24 Apr, most for the period since 2009

The rate of small, private co bankruptcies is rising in the US - BBG

FC Barcelona Closes €1.45 Billion Deal to Fund Stadium Revamp

Cineworld Gets Competing Offer for $2.26 Billion Financing

American Air reports $14.4bn of total available liquidity, record FCF Generation

Hertz expects a strong Summer 2023

REAL ESTATE

UK Dept Store John Lewis to slash London office space as staff WFH

SBB to carry out rights issue for 2.6bn SEK ~$250m to reduce debt - Cision

Apollo to Provide €1 Billion Capital Solution to Vonovia

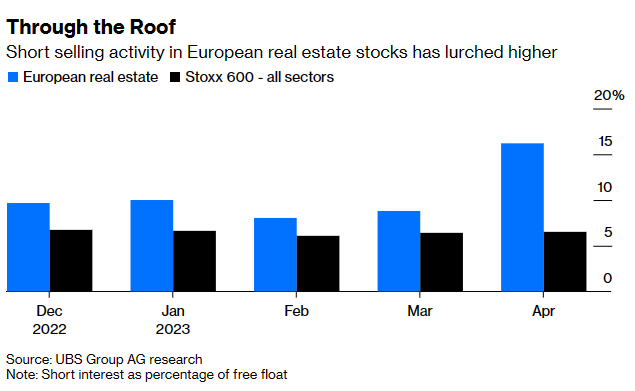

“Short European Real Estate? Beware. So Is Everyone Else”- BBG Opinion

Short Sellers Bet Against Blackstone and Starwood Mortgage REITs - BBG

Blackstone loan backed by Manhattan apartments enters special servicing - WSJ

Parts of Australia seeing some issues with CRE too - UrbanDeveloper

Pizza Chain Prezzo shuts 46 branches including four in London

RTTO Updates

EM

Cemex continues to take out debt

Sasol issues new $1bn bond

Egypt CDS surging, bond prices continue to trade at depressed levels

Sri Lanka Pushes Debt Restructuring Presentation to Mid-May

China’s Factory Sector Contracts as Recovery Concerns Linger

Erdogan cancels third day of election appearances ahead of May 14 Election

Indian firms - Vedanta pays debts due in April, Adani tender offer for Ports bonds

Ecuador launches debt buyback plan aimed at Galapagos protection

RATINGS

Nissan given BBB- rating at Fitch, now back in IG Index after being downgraded last month

Jaguar Land Rover upgraded by S&P to BB-

Moody’s downgrades certain Regional Banks in the US

S&P affirms Egypt's credit rating at B/B, lowers its outlook to negative from stable

BUYSIDE / TRADING

Blackstone Among Buyers of Kaiser $5b portfolio, includes Private Credit

Ares targeting HNWIs in latest $1.5B push into private credit market

Ex King St Partner highlights dangers of Private Debt Markets and Leverage

Good article in the FT re Electronic Credit Trading

Barclays FICC Trading Highlights from Q1

*MOVES*

Since I missed last week’s wrap, I’ll also chuck in some month end moves for those that might find it useful for month end commentaries.

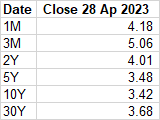

Rates

UST 1w moves - Rally across the board with biggest rallies in the front end. 2s and 5s rallied 18bps each and 10s and 30s rallied 15bps and 10bps respectively.

The 2 year being so far below the Fed Funds rate suggests the market is pricing in a series of cuts towards the end of this year and onwards.

UST 1 month moves - Biggest moves were in the very short end where 2m bills rallied 65bps, 3m bills rallied 30bps. Other notable moves were the 20bps tightening in 5s and 14bps tightening in 10s.

European Govt bonds rallied strongly to close the week due to an anemic German GDP print and softer than expected inflation data out of the nation. 2s rallied 19bps, 5s rallied 21bps, 10y rallied 17bps and 30y rallied 14bps.

Source for data: BBG

Credit

Bond ETFs

Best performers were Duration, EM, Munis, and HY over the week. Some highlighted leaders: EDV+2.4%, TLT+2.0%, EMB+1.6%, HY+1.2%, EUNH+1.2%, BIV +1.0%, HYLD+1.0%,

Laggards were Convertibles, Prefs, TIPS, Short dated JGBs (1-3 year). Some highlighted laggards: JT13 IM -1.8%, PFFD-0.7%, ITPS-0.7%. The weakness in prefs is unusual because normally they tend to rally with a rally in duration but holdings in Regional Bank Prefs are a drag on returns, e.g. the FRC 4.5% 25c prefs are now trading at below 2c.

Credit spreads

Weekly moves - Nothing of real interest in CDS other than Xover tightening 5bps to 435bps. Within cash credit, there seemed to be more of a widening trend (Pan EUR HY +18bps, EMHY+16bps, Bank CoCos +12bps).

Monthly moves - Over the month there was little movement in CDS. Within cash credit, GBP IG tightened in the most this is despite the BoE selling Corporate bonds as a part of its QT. Very low issuance, a seasonally strong month for Credit and new inflows as part of new tax year could be what is offering support in GBP credit. Bank CoCos tightened in 9bps continuing the tightening post the CS debacle. EM HY spreads were +16bps presumably due to weakness seen in Afri Sovereigns like Egypt and Kenya. I thought the below tweet was quite good in that it contests if credit spreads are actually a good leading indicator for future weakening:

https://twitter.com/SpreadThread1/status/1651994398299762695

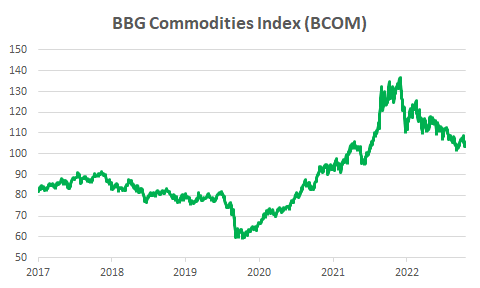

Commodities

Commodities complex very weak as judged by BBG Commodities Index

The weakness is reflected in Iron Ore, Oil and share prices of a number of resources and shipping names currently

Brent Crude has erased all price gains since surprise OPEC Cut. Also, Brent has been down for 6 months in a row now.

Notable Equity Moves

All major indices posting gains in the month led by FTSE 100 which returned 3.41% followed by the Dow Jones Industrial Average which returned +2.57%.

UK and US Homebuilders a huge area of strength:

Beazer Homes (HY Name) +24.8% just on Friday

UK Mid Cap Crest Nicholson linked with takeover talk +8.9% on the week

Better than expected updates from UK Builders; Persimmon and Taylor Wimpey also boosted the sector.

UPS closed down 10% in biggest one day drop since 2006

Northern Trust Down Over 9% on 25 April, largest % decrease since Mar 2020

Higher beta banks underperforming lower beta in Europe

A number of Insurers seeing price strength - E.g. Allianz 52w high, Hiscox 52w high, Prudential (UK listed) +4% on Friday alone

US Autos are weak (GM/Ford/Tesla) presumably due to mix of price cutting, higher lease costs and front running of recession worries

*MACRO*

Please check out FXMacro’s weekly macro comment for a more comprehensive take on macro.

Eurozone economy grew marginally in the first quarter of 2023, but divergence is high - ING

Extract - The eurozone economy grew by a meagre 0.1 % quarter-on-quarter in the first quarter of the year, from zero in the fourth quarter of 2022. On the year, GDP growth came in at 1.3%. Growth across the eurozone ranged from -2.7% QoQ in Ireland to +1.6% QoQ in Portugal. A homogenous monetary union looks differently.

German inflation slows unexpectedly after economy stagnated - BBG

Extract - German inflation unexpectedly eased in April after the economy struggled at the start of 2023, adding to a mixed bag of data for the European Central Bank to ponder before next week’s interest-rate decision. Consumer prices climbed 7.6% from a year ago — down from March’s 7.8% pace, which economists estimated would be maintained.

Hedge Funds Place Biggest Ever Short on Benchmark Treasuries - BBG

Extract from 24 Apr - Leveraged funds may expect sticky inflation, Westpac says. US yields rose in April after recording monthly drop in March. Hedge funds are betting on higher Treasury yields in a market that’s divided over whether the US economy can avoid recession and Federal Reserve interest-rate cuts.

Riksbank Hits Economy With Half-Point Hike to Tame Prices - BBG

Job losses recap

3M to Cut 6,000 Jobs in CEO’s Latest Restructuring Push - BBG

Lazard to cut ~10% of workforce - BBG

First Republic cutting jobs by about 20-25% in Q2 - BBG

Dropbox to lay off 500 employees, or about 16% of its workforce

Alteryx Plans to Cut 11% of Workforce

RapidAPI, valued at $1 billion last year, cuts staff by 50% (115 people)

Vroom (VRM) to cut 11% of workforce (120 people)

Red Hat To Lay Off Over 700 Employees

Flink has quietly eliminated 8,000 jobs (grocery delivery firm)

Vice Media Reportedly Cuts 100 Jobs

Amazon starts layoffs in HR and cloud units - CNBC

Extract - The layoffs are part of the previously announced job cuts that are expected to affect 9,000 employees, on top of the 18,000 job cuts that took place earlier this year and last November.

Source for most of these: https://www.trueup.io/layoffs

PwC is making a $1 billion bet on business AI: PwC

A development that is likely to lead to more job cuts but also job additions for those that can harness the power of Generative AI, extract:

April 26, 2023 — Today PwC US announced plans to invest $1B over the next three years to expand and scale its artificial intelligence (AI) offerings and help clients reimagine their businesses through the power of generative AI. The investment builds on PwC's long-standing commitment to AI, strengthening its ability to deliver human-led and tech-powered solutions and to build trust and drive sustained outcomes in line with its global strategy, The New Equation.

Japan's Life Insurers sticking to plans to reduce currency hedged foreign debt - BBG

I feel not enough attention is being paid to this news item, since Asia is such a large buyer of IG Credit:

Extract - Japan’s biggest life insurers are sticking with plans to reduce holdings of currency-hedged foreign debt this year and buying bonds at home amid speculation of central bank policy tweaks. With combined assets of $2.9 trillion including sizable holdings of securities from US government debt to corporate bonds, their allocation plans are closely watched by investors already worried about the impact of a Bank of Japan policy change on global markets. The insurers expect hedging costs will remain expensive in the current fiscal year from April, a key factor spurring them to cut overseas holdings further, and see BOJ changes coming as early as June.

British Shopper Resilience Fuels Earnings Beats - BBG

Extracts - Consumers appear to be showing remarkable resilience to rising prices. Results this morning from Sainsbury and Unilever indicate customers are stomaching the increases. Defying market expectations, Sainsbury said it may even increase profits this year, indicating its efforts to cut costs and compete with discounters might be paying off.

Ballooning Customer Debt Is Next Problem for UK Energy Suppliers - BBG

Something of a counter to the previous article in that UK Household balance sheets are continue to be pinched by higher energy costs, despite the drop in wholesale prices. The news hasn’t stopped Centrica (British Gas owner) posting an 18% YTD share price move!

Extract -

(Bloomberg) -- Britain’s energy suppliers are facing a bleak year as hard-up customers struggling to pay bills leave them with mounting bad debt.

Energy prices have dropped from their record highs, but remain almost double the level of two years ago.

It’s stranding businesses and households — already swamped by surging living costs — with high energy bills that suppliers fear will never be recovered.

Overdue debt is estimated to have grown to £3.2 billion to £3.6 billion ($4 billion to $4.5 billion) from £2.5 billion last year, Emma Pinchbeck, chief executive officer of industry association Energy UK, said at Ofgem’s Vulnerability Summit on Monday.

Some suppliers were “providing over £500,000 per week in credit to their customers,” she said.

This year has seen a “continued squeeze on people’s finances, translating into a debt crisis which is going to be with us for a long time to come,” Clare Moriarty, CEO of charity Citizens Advice, said at the same summit.

*INFLATION*

Sovereign Snippets

Australia 1Q Trimmed Mean CPI Inflation comes in light of expectations but 1Q CPI comes in higher than expected

Singapore Core Inflation Slows as Food Prices Come Off Highs

Annual inflation in the eurozone eased to 6.9% in March from 8.5% the month before - AP

…but is well above the ECB’s goal of 2% considered best for the economy. So-called core inflation, which excludes volatile food and energy prices, also hit a record 5.7%.

UK Govt gets record demand for Inflation linked Gilts - BBG

Extract - The £46 billion ($57 billion) order book for £4.5 billion of so-called inflation-linked notes sold on Wednesday was far bigger than any previous UK sale of similar debt tracked by Bloomberg. Data last week showed consumer prices in Britain accelerated 10.1% from a year ago, driven by the strongest increase in food costs in more than four decades.

Corporate Snippets:

Chipotle outperformed expectations in part because of lower avocado prices - BBG

Nestlé pushed up prices by an average of almost 10% in the first 3 months of the year - FT via BBG

Michelin CFO Sees Smaller-Than-Expected Inflation Hit This Year

Danone CFO comments on Inflation:

Sees inflation rate decreasing throughout the year

Seeing inflation in wage costs, liquid milk and sugar,

Sees gradual normalization of prices going forward.

*FINANCIALS*

Banks New issues/tenders - AT1 called for Lloyds & Unicredit

As largely expected, there were two AT1s tendered this week for Lloyds and Unicredit. Unicredit were allowed by the ECB to call the UCGIM 6.625% without need to issue new AT1. Combined, the two tenders make up more than $1bn of which some is likely to be re-invested in the AT1 asset class. Virgin money tendered for its € VMUKLN 0 ⅜ 05/27/24 senior bonds.

Its interesting to note that DB is cutting its 2023 issuance plan due to higher borrowing costs (BBG).

Investec Bank got a $350m Syndicated Term Loan for GCP, according to the company:

“The Facility was initially launched at US$250,000,000 and achieved a substantial oversubscription of over 1.5x of the launch amount. Commitments were scaled back and the significant market demand further allowed the deal to be increased, closing at US$350,000,000. A total of 14 banks committed to the transaction from across North America, Europe, the Middle East and Asia.”

Recent new issues from midcap UK/Irish Banks PTSB (Senior) and OneSavingsBank (T2) are trading at a small premium in the secondary market.

Insurance bonds see surge in tender activity

Insurers: AXA SA, Assicurazioni Generali SpA, Ethias, Vienna Insurance Group AG and NN Group NV — have offered to buy back around $3 billion-equivalent of their old-school bonds in recent weeks. These bonds won’t count as capital by the end of 2025 according to Bloomberg. NN, Generali, and Ethias have all issued new bonds (mainly Green Bonds) to recycle some of the money coming back from tenders. In the UK, Insurer; Liverpool Victoria completed the partial tender of £150m of its £350m issue.

Swiss regulator says two banks' crisis plans are insufficient RTRS

Extract - Swiss financial regulator FINMA has labelled the recovery and resolution plans of two of Switzerland's five systematically important banks as insufficient, it said on Wednesday. FINMA questioned the ability of Zuercher Kantonalbank (ZKB)and PostFinance to continue functioning in case they experienced a crisis. It said "ZKB has not yet built up the required capital in full" and that "PostFinance must realign its emergency planning."

Earnings recap and notable Equity moves

The main themes I took away from European Bank earnings were as follows:

Most UK/European Banks which reported beat analyst estimates

Analysts continue to under-estimate the benefit of higher interest rates on banks

No major negative surprises from CRE, especially from Scandinavian Banks

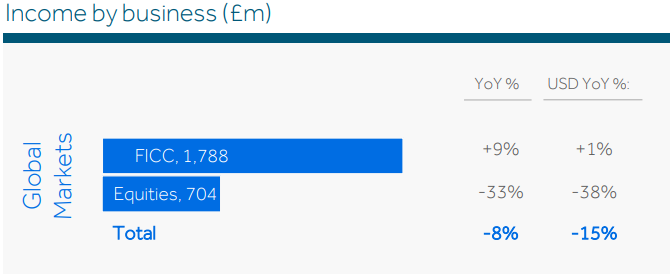

Barclays massive beat on FICC

Several Banks announced share buybacks - DB, Nordea, BBVA to name a few

Deutsche Bank recorded its best profit in a decade as the bank recorded its 11th consecutive quarter of profit

Job cuts are starting to happen (e.g. DB) due to underperformance in certain areas

This all reads quite well, but looking at the 5 day performance of stocks which reported, overall the performance was underwhelming bar a few exceptions (e.g BARC, SEB).

This could be because of two reasons, a strong run-up for some banks going into earnings and also the rally in European Government bonds which normally are inversely correlated to the performance of European Bank stocks. Other moves in Fins which I thought were interesting this week:

Spanish Banks Santander & Sabadell closed 10-11% down over 5 days

Some UK listed Insurers/Asset Mgrs posting ~5%+gain over week:

Lancashire (had good trading update)

Prudential (+4.2% on Friday alone after strong biz update)

ABRDN

Strength in Lloyds Insurance Syndicates (Lancashire up nearly 6% on the week, Hiscox hit new 52w high)

Nomura fell 7.9% after 4Q net missed estimates - BBG

Allianz Hit 52-Week High at 224.40 Euros

25 April: Northern Trust Down Over 9% (largest decrease since Mar 2020)

Greek elections coming up, could see Greek Banks move

Election is on 21st May, check out this thread from the GreekAnalyst.

CS & AT1News Recap

Oxford Uni Biz Law Blog analyses legal challenge of CS AT1: Blog

MUFG Says Credit Suisse AT1 Debt Sold to Help Clients Diversify - BBG

NOMURA CFO: DECIDED AGAINST SELLING CS AT1 BONDS TO INDIVIDUALS - BBG

UOB CFO: TOLD CLIENTS TO GET OUT OF CREDIT SUISSE AT1 LAST YR -BBG

Deutsche Bank CFO Says AT1 Market Needs Time to Heal - BBG

UBS CEO: BANK TO LOOK AT WAYS TO RE-ENTER AT1 MKT, NOT PRIORITY - BBG

First Republic Recap

I’ve not written much on First Republic as its covered very well elsewhere. The latest seems to be that it maybe auctioned on Sunday 30th April to see which other firms would look to buy it. According to Joe Politano; “First Republic is the 14th largest bank in America—larger than Silicon Valley Bank was and would be the 2nd largest bank failure in US history.

While problems like this are happening, its likely to keep a safety bid on safe havens and caution when it comes to risk assets generally.

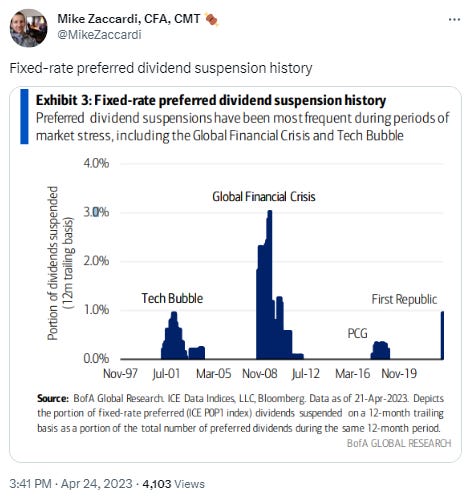

Good chart on Fixed-Rate Pref dividend suspensions

*IG*

IG new issue summary - $65.7bn in US IG & €127bn in EUR IG in April

In the US, April saw $65.7bn of US IG issuance which is underwhelming vs prior years but shows that the market is still clearing risk.

In terms of issuance patterns, Aircraft Lessors are active with BoC Aviation pricing debt during the week and Irish Aircraft Lessor Avolon roadshowing with a view to potentially issuing new debt.

European IG printed more size (including SSAs though) with a total of €126.7bn.

Corporate Reporting summary

Investors really liked Big Tech earnings which kept the main indices higher. Check out this cool little summary from a guy called Stock Market Nerd who covers Microsoft, Google, Amazon, Visa and Mastercard amongst others.

Other news snippets for IG issuers:

Caterpillar Earnings Crush, But CAT Stock Falls Below Key Level - IBD

Iliad, Vodafone Are Said to Revive Talks on European Tie-Ups

Vodafone opts for insider (CEO) after rigorous search - RTRS

Nissan Motor Raises FY Net View to Y220.00B

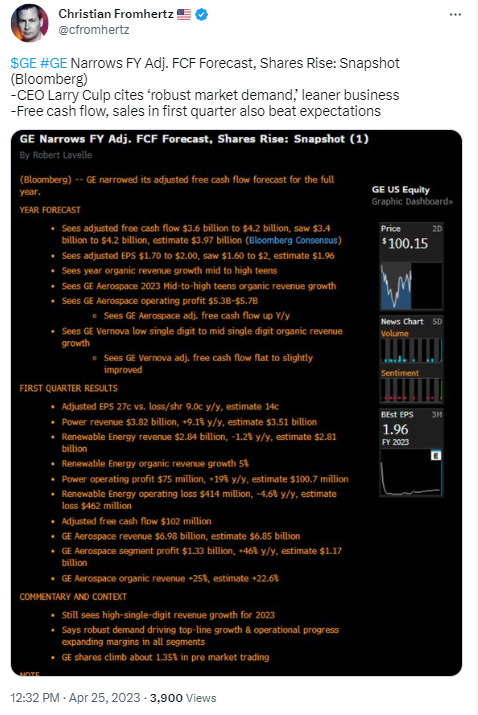

GE reported good figures via @CfromHertz

*HY / Lev loans*

HY Issuance trends - $18.8bn priced in April 2023

US HY saw $18.8bn of debt issued vs $11bn in April 2022

There are deal upsizings going on, e.g Talen Energy boosted its bond sale from $825m to $1.25bn and reduced the amount it was going to issue in the lev loan markets. Other deals that priced during the week included (bbg):

The average coupon across the deals shown above are nearing 10%, which shows the cost of getting business done. Trident TPI is a CCC, Six Flags single B, Benteler BB- and Talen Energy BB.

BBG’s Michael Gambale commented that the strength in US HY issuance has been due to inflows into the sector during the month.

In the lev loan market, I note that Signature Aviation brought a $400m add on deal and Agiliti (medical equipment) raised more than $1bn in the TLB market after previously postponing a deal. Source for all the above: BBG.

European HY Issuance highlights - Around €3bn priced in the week

European HY issuance also has been ticking along in less “householdy” type names.

Source for all the above: BBG.

68 large bankruptcies in the US as at 24 Apr, most for the period since 2009 - BBG

Extracts -

There were three large bankruptcy filings last week, including those of David’s Bridal and Structurlam Mass Timber

With the addition of Bed Bath & Beyond’s filing on Sunday, there have been 68 large bankruptcies in the US so far this year as of April 24, the most for that period since 2009

BBG reported that smaller, private businesses seeing rise in bankruptcy rate

FC Barcelona Closes €1.45 Billion Deal to Fund Stadium Revamp - BBG

Extract - Spanish football club FC Barcelona has closed a financing deal earmarked to revamp its Camp Nou stadium. The €1.45 billion ($1.6 billion) in funding will be provided by a group of 20 investors and is to be repaid in five installments over 24 years, the club said in a statement on its website late Monday. The stadium’s poor conditions have led to fines for failing to meet European competitions requirements. The club’s assets weren’t used as a guarantee and no mortgage was taken out on the stadium, Barcelona said. It’ll start to pay down the debt once the revamp works are completed, using the income generated by the stadium, which is expected to be about €247 million annually.

Cineworld Gets Competing Offer for $2.26 Billion Financing - BBG

Extract - Some lenders to Cineworld Group Plc are putting together a competing bankruptcy exit financing package that they argue is superior to the theater chain’s existing $2.26 billion proposal. A group of lenders that includes Avenue Capital Management, Jefferies Leveraged Credit Products LLC and Greywolf Capital Management unveiled their proposal in court filings and a bankruptcy hearing Thursday. The creditors argue Cineworld’s current exit financing plan unfairly benefits a majority lender group they were blocked from joining.

The competing group has commitments for an exit term loan facility of as much as $1.46 billion that would be cheaper than.

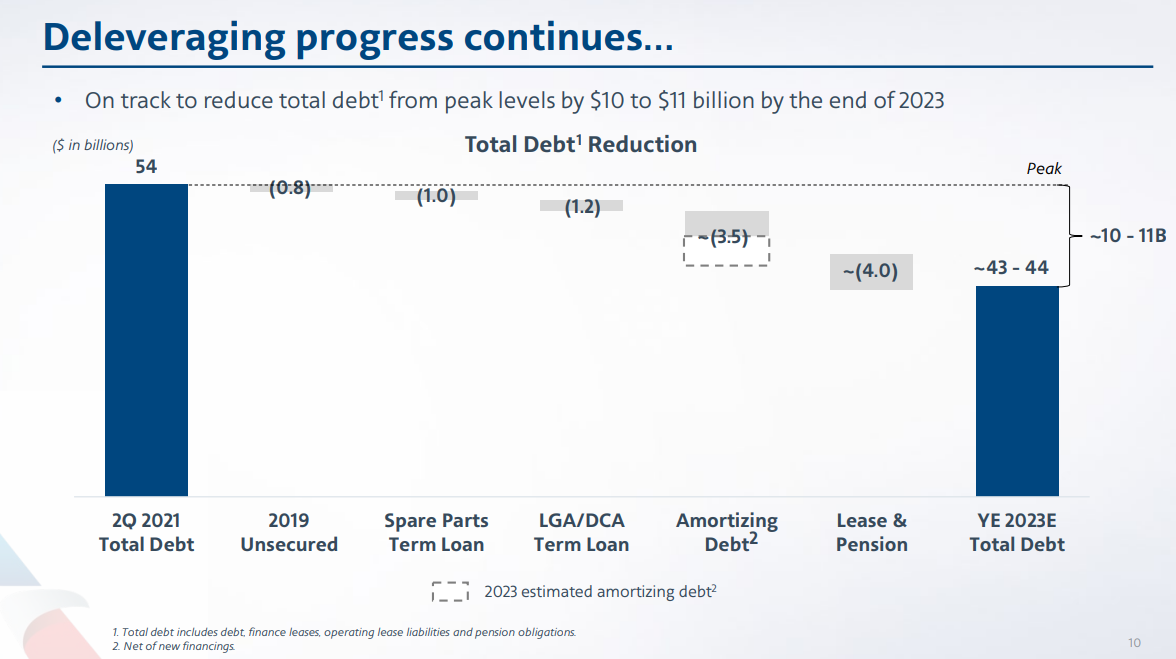

American Air reports $14.4bn of total available liquidity, record FCF Generation

Highlights from conf call, TLDR; OCF of $3.3bn in Q1, $14.4bn of total available liquidity. Extracts of Report & conf call:

In the first quarter, we generated operating cash flow of $3.3 billion. Our adjusted net investing cash flows were $317 million resulting in record quarterly free cash flow generation of $3 billion.

We ended the quarter with $14.4 billion of total available liquidity, $2.4 billion more than our year-end 2022 liquidity balance driven by booking strength and APL growth in the quarter. We continue to make progress on strengthening our balance sheet, reducing total debt by more than $850 million in the quarter. This debt reduction combined with the improvement in liquidity, resulted in a $3.4 billion decrease in net debt during the first quarter.

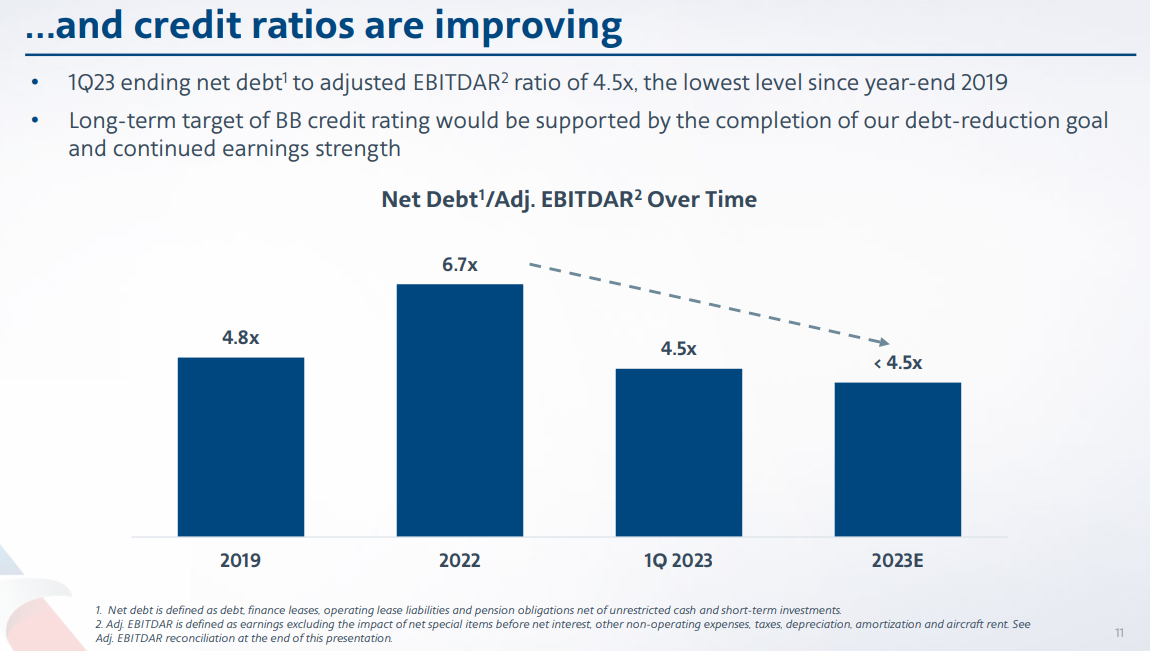

We now have reduced total debt by more than $9 billion from peak debt levels in mid-2021. Importantly, we ended the first quarter with a net-debt to EBITDA ratio of 4.5 times, which is lower than our net-debt to EBITDA ratio at the end of 2019. By the end of 2023, we continue to expect our total debt to be $10 billion to $11 billion lower than peak debt levels in mid-2021. And we remain committed to our goal of reducing total debt by $15 billion by the end of 2025.

Additionally, a constructive financing environment in February allowed us to proactively refinance at 2025 maturity. Our $1.75 billion term loan primarily collateralized by our South American portfolio of slots, gates and routes. The refinancing transaction efficiently derisked our 2025 debt maturity towers by nearly 20%. We will continue to balance debt reduction opportunities and investments in the business while meeting appropriate liquidity levels.

We will continue to hold ourselves accountable to produce stronger margins, generate free cash flow, strengthen our balance sheet, and run a reliable operation, ultimately creating more value for our customers and shareholders.

In response to an analyst question re debt reduction plan; Devon May, Chief Financial Officer said this:

Yes, so, to start this year, we have talked about our total debt paydown being at approximately $10 billion to $11 billion from our peak levels of summer of 2021. For this year, we expect total debt to be down about $3 billion versus 2022. In terms of where our cash will be at the end of the year, obviously, we've talked a lot about a $10 billion to $12 billion target for liquidity, we're well ahead of that at the end of the first quarter. When we think 10 to 12, I generally think of it as, and we'd like to be around $10 billion of liquidity as we are late in the year at 0.4 liquidity that arise to $12 billion during the year. At this point, we're well ahead of our target liquidity, I expect we would definitely be on the high end of target liquidity if we hit the midpoint of our guidance this year. And then just longer-term 2024, we have a little bit of a step-up in maturities. I think most people understand in 2025, we have a higher debt tower. We proactively addressed some of that with refinancing in the first quarter. The remainder of it, we will seek to either stay down or refinance a portion of it depending on our cash-flow production over the next couple of years.

Hertz readies for strong summer demand after upbeat quarter - RTRS

(Reuters) -U.S. car rental company Hertz Global Holdings Inc said on Thursday it was preparing for strong summer travel demand and projected a 20% jump in second-quarter revenue from the first, driving its shares up as much as 4%..

"The demand and pricing dynamics are there," CEO Stephen Scherr said in a post-earnings call.

Hertz, whose sales are closely tied to the airline and hotel industry, is also benefiting from more people hiring vehicles for their daily commute as more companies mandate work from office.

Demand for Hertz's rental services was boosted by its electric vehicle fleet as consumers looking to buy a car with an alternate powertrain opted to rent those vehicles before deciding to purchase, said Tigress Financial Partners analyst Ivan Feinseth. Hertz had about 50,000 electric vehicles, or 10% of its fleet, at the end of the first quarter.

Hertz itself provided a decent summary of its key metrics:

*REAL ESTATE*

UK Dept Store John Lewis to slash London office space as staff WFH- Telegraph

Similar announcement to HSBC a few months ago regarding downsizing its office footprint in the Capital.

Extract - John Lewis is slashing the size of its central London headquarters by more than half, after thousands of staff left their desks to work from home. The John Lewis Partnership, which also owns Waitrose, is understood to have hired property experts from Tuckerman to help it find new offices in central London, with plans to move next year. Sources suggested that the partnership is looking for offices which are less than half the size of its current headquarters. It occupies around 220,000 square feet of space at its offices in London Victoria, according to industry sources, and is seeking a location with about 100,000 square feet of office space.

SBB to carry out rights issue for 2.6bn SEK ~$250m to reduce debt - Cision

Extract: The Board of Directors of Samhällsbyggnadsbolaget i Norden AB (publ) (“SBB”) today announces its intention to carry out a rights issue of class D common shares of approximately SEK 2.63 billion at a subscription price of SEK 16 per class D common share (the “Rights Issue”). The Rights Issue is carried out for the purpose of lowering the company’s indebtedness…

Apollo to Provide €1 Billion Capital Solution to Vonovia - Apollo

An interesting transaction of which my main take-aways are:

Decent size transaction at a time when transaction data is rare in EU RE sector

Yet more involvement of US Investors in European RE of late, others:

Blackstone bid for MLI in the UK (Industrials)

Brookfield’s SEK10.4bn (€962.4m) acquisition of a 49% stake in SBB Nordics public education portfolio in 2022

Residential RE in Europe appears to be an are of strength due to the chronic under-supply of homes

Extracts of Apollo and Reuters commentary on the deal below:

Apollo today announced that, on behalf of its affiliated and third-party insurance clients and other long-term investors, it has agreed to invest €1 billion in a portfolio of high-quality real estate assets controlled by Vonovia. Headquartered in Germany, Vonovia is a leading global residential real estate company with assets of approximately $100 billion. SRC: APO

Vonovia has agreed to sell a minority stake in its Suedewo residential portfolio to U.S. investor Apollo for 1 billion euros SRC: RTRS

The transaction could have a signal effect on the struggling German real estate market, where hardly any major sales have occurred in recent months in the face of high interest rates and falling real estate prices. SRC: RTRS

The transaction values the Suedewo portfolio in the southwestern state of Baden-Wuerttemberg at 3.3 billion euros, which is a discount of less than 5% to Suedewo's fair value as of December 31, Vonovia said. SRC: RTRS

The German group, which will continue to manage the portfolio of more than 21,000 residential units, has agreed to a long-term buy-back option without an obligation to do so, at an internal rate of return (IRR) of 6.95%-8.30% including dividends received, it said. SRC: RTRS

With the proceeds, Vonovia will generate around half of the targeted 2 billion euros in free cash flow from asset sales. SRC: RTRS

Short European Real Estate? Beware. So Is Everyone Else - BBG Opinion

I thought this was a really well put together article that offers some food for thought in a sea of negativity on European RE.

Extract - The continent’s property stocks are overrun by short sellers and the bear case is obvious. But crowding in a relatively small sector creates risks of its own.

Short Sellers Bet Against Blackstone and Starwood Mortgage REITs - BBG

Extract -Wagers against commercial mortgage REITs have soared recently. Regional bank turmoil has added to headwinds facing borrowers. Short sellers have ramped up bets against commercial mortgage REITs, wagering that more borrowers will default on office debt as interest costs increase and property values fall. Short interest in the largest mortgage real estate investment trusts focused on business properties, including Blackstone Mortgage Trust Inc. and Starwood Property Trust Inc., hit post-pandemic highs in the past month, according to data compiled by S&P Global Market Intelligence. Hedge funds have been using credit derivatives and equities to bet that the rise of working from home will cripple demand for poorer-quality properties and hurt landlords.

Blackstone loan backed by Manhattan apartments enters special servicing - WSJ

Extracts - Blackstone Inc. risks losing a portfolio of Manhattan apartments…

[Blackstone] is in danger of defaulting on a $270 million loan backed by 11 apartment buildings in New York’s most expensive borough.

Cash flow from the properties isn’t enough to cover the cost of all the debt, according to a report from Moody’s Investors Service.

…The rental boom hasn’t been enough to cover Blackstone’s growing maintenance costs on the 11 buildings, which were built between 1900 and 1987 and are mostly located in the Chelsea and Upper East Side neighborhoods.

Parts of Australia seeing some issues with CRE too - UrbanDeveloper

Pizza Chain Prezzo shuts 46 branches including four in London - City AM

Extract - Prezzo will shut 46 loss making sites across the UK including three in London and place 810 workers at risk of redundancy, as soaring energy and a hike in food costs rattle the business. The Italian restaurant chain, which is owned by private equity firm Cain International said that the closures will impact sites where “the post-Covid recovery has proved harder than we had hoped”. The strategy will reduce its portfolio to 97 sites across the UK and Ireland and a workforce of around 2,000.

RTTO Updates

Lloyds orders staff back to the office – for two days a week

Lyft Employees Told to Return to Office as New C.E.O. Lays out vision

Amazon’s Jassy said in a February memo that he will require corporate employees to spend at least three days per week in the office beginning May 1.

Meta has stopped offering remote work when it lists new jobs, at least for now.

Sources: Business Insider, Bloomberg, NY Times

*EM*

EM New issues / Tenders

New issue from Sasol to raise $1bn at a yield of 8.75%.

Cemex continues its debt reduction plans by redeeming its 7.375% notes due 2027, interestingly Cemex’s shares are up more than 30% ytd.

Mongolian Mining Corp. announced the termination of its exchange and tender offer with respect to 9.25% senior notes due 2024

Egypt’s Doomsayers Pay More Than Ever to Protect Against Default - BBG

Egypt bonds seems to be front and centre as the next concern for EM focused investors. Without being an expert in Egypt debt, here are some of my main takes based on BBG Data:

DDIS Function on BBG shows nearly $50bn of face value hard currency debt across ~40 issues

Short term $ debt is trading at a discount to par, i.e Nov 2023s indic 93/94 and March 2024s ~ 87/88

Lowest cash price bonds are indicated as low as 49/50, i.e EGYPT 2061s

I haven’t spoken about its local bonds, but Egypt is also a heavy user of the local bond market. Its yet another EM issuer with too many bonds outstanding and the frequent problem of who is the next marginal buyer, which results in multiple “buyers strikes” for these types of bonds.

Will be interesting to see how Egypt negotiates its debt maturities over the short term and next few years. Extracts of BBG article:

Extract - Five-year CDS at a record discount to the one-year contract

Traders pricing in a higher chance of a near-term default risk

Egypt debt markets are on edge like never before, increasingly consumed by the threat of it missing a payment on its bonds within a year. The IMF has delayed its review of a US$ 3bn rescue program and billions of dollars in promised funding from Gulf Arab nations have yet to materialize as they seek greater evidence that authorities are moving ahead with implementing reforms announced last December.

The lack of clarity is making it even harder for the government to move ahead and get the money it needs to cover its spending needs. Adding to the pressure, S&P Global Ratings lowered the outlook on Egypt’s B credit score to negative at the end of last week, taking a far more downbeat view of the nation’s finances than the IMF.

Sri Lanka Pushes Debt Restructuring Presentation to Mid-May - Business Times

SRI Lanka pushed back the release of its debt restructuring plan to investors to the middle of May from this month.

The government will present a comprehensive plan for treating foreign as well as local debt, PKG Harischandra, director of economic research at the central bank, said late on Tuesday (Apr 25), without explaining the delay.

Foreign creditors want to include local debt in the restructuring, which some Sri Lankan banks oppose, President Ranil Wickremesinghe told lawmakers on Wednesday during a debate on the International Monetary Fund (IMF) bailout. The government seeks to avoid talks that include pre-conditions, he said.

China’s Factory Sector Contracts as Recovery Concerns Linger - BBG

Extracts - Manufacturing PMI contracts for first time since December

Services activity expands on consumption, construction growth

The official manufacturing purchasing managers’ index fell to 49.2 from 51.9 in March, the National Bureau of Statistics said Sunday. The gauge dropped below the level of 50 — which signals contraction from the previous month — for the first time since December. Economists surveyed by Bloomberg had forecast 51.4.

A non-manufacturing gauge of activity in the services and construction sectors declined to 56.4 from 58.2 in March. Economists had forecast the index to hit 57. A reading above 50 indicates expansion.

China’s Industrial Profits Keep Plunging as Prices Decline - BBG

Extract:

Profits at industrial firms in China continued to plunge in the first three months of the year, as a pickup in factory production failed to offset a further decline in prices.

Industrial profits in the January-March period declined 21.4% from a year earlier, the National Bureau of Statistics said Thursday.

The drop narrowed only slightly from a fall of 22.9% in the first two months of 2023.

Profits for the single month of March fell 19.2% from a year ago, according to official figures.

Turkey’s leader Erdogan cancels third day of election appearances ahead of May 14 Election - Al Jazeera

Extract - Turkish President Recep Tayyip became ill during a TV interview with what Health Minister Fahrettin Koca later said was a ‘gastrointestinal infection’.

Turkish President Recep Tayyip Erdogan has cancelled his election appearances for a third day after falling ill with what officials described as an intestinal infection.

Erdogan is seeking a third presidential term in Turkey’s May 14 elections. He had been due to appear at a bridge opening and a political rally in the southern city of Adana, but his schedule changed on Friday to show he would attend the opening ceremony via video link.

Indian firms - Vedanta pays debts due in April, Adani tender offer for Ports bonds

RTRS - Vedanta Resources Ltd, the parent of Indian resources major Vedanta Ltd (VDAN.NS) on Monday said it has trimmed its gross debt by $1 billion as the firm seeks to allay concerns over its ability to meet financial obligations beyond September.

Vedanta Resources has paid all its maturing loans and bonds due in April 2023, the billionaire Anil Agarwal-led company said in a statement.

Adani Ports launches tender offer for bonds worth $130 mn - Financial Express

Adani Ports and Special Economic Zone (APSEZ) has launched a tender offer for bonds worth $130 million, which the company will use to partly pre-pay near-term debt maturities.

Ecuador launches debt buyback plan aimed at Galapagos protection - RTRS

Extract - April 26 (Reuters) - Ecuador has launched a long-awaited debt buyback plan that will free up money to protect its Galapagos Islands, one of the world's most precious ecosystems and the inspiration for Charles Darwin's Theory of Evolution. Ecuador's bankers, Credit Suisse, laid out the offer on Wednesday to buy back three of the country's four main government bonds for a total of $800 million, refinance them more cheaply and then funnel the savings into the Galapagos.

*BUYSIDE /PRIVATE CREDIT*

Blackstone Among Buyers of Kaiser $5b portfolio, includes Private Credit: WSJ

Extract - (Bloomberg) -- Blackstone, Apollo and Ardian are among a group of buyers set to acquire ~$5b of private fund positions from Kaiser Permanente, Wall Street Journal reports, citing unidentified people familiar with the matter. The assets are held by the California-based health care provider pension plan, which is seeking to raise cash for new investments The positions include interests in private credit, venture capital funds and buyout funds.

Ares targeting HNWIs in latest $1.5B push into private credit market - Pitchbook

Extract - Ares Management has collected billions for a new private debt fund tailored to high-net-worth individuals, the latest sign that private asset managers are tapping into the vast retail market for fundraising. The Los Angeles-based firm launched a private business development company, which has lined up nearly $1.5 billion in investable capital to make direct loans to US middle-market companies, according to an SEC filing from Monday. The BDC, dubbed Ares Strategic Income Fund, has collected $847.1 million from several investors and has secured a $625 million credit facility from JP Morgan, the filing shows.

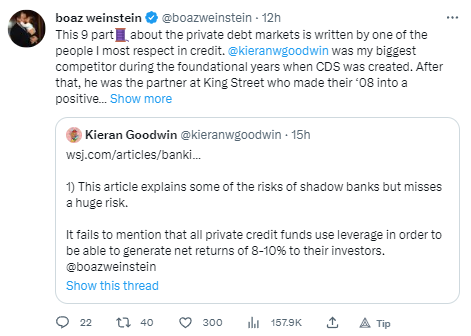

Ex King St Partner highlights dangers of Private Debt Markets and Leverage

Link to original Tweet + Thread below.

https://twitter.com/kieranwgoodwin/status/1651691441020715010

*RATINGS*

DM SOV

UNITED KINGDOM OUTLOOK TO STABLE FROM NEGATIVE BY S&P

Italy Affirmed at BBB by S&P

Moody's Upgrades Ireland to Aa3, Changes Outlook to Stable

X-S&PGR Revises Greece Outlook To Positive; Affirms At 'BB+/B'

IG

AB InBev Upgraded to A- by S&P, Outlook Stable

Nissan given BBB- rating at Fitch, now back in the IG Index after being downgraded last month

HY

X-S&PGR Upgrades eDreams To 'B-'; Outlook Stable

S&P lowered Altice France's rating by one notch to B-, and revised the outlook to stable from negative.

Jaguar Land Rover upgraded by S&P to BB-

FINS

Saxo Bank has received a BBB rating with a positive outlook from S&P Global Ratings, according to the bank’s first-ever rating report

S&P Changes Banco de Sabadell's Outlook to Positive on Enhanced

American Express Affirmed at A2 by Moody's

Discover Financial Affirmed at BBB+ by Fitch

Moody’s downgrades certain Regional Banks in the US:

U.S. Bancorp Downgraded to A3 by Moody's, Outlook Stable

Moody's downgrades Western Alliance's ratings (bank deposits to Baa1 from A2); outlook stable

Washington Federal Downgraded to Baa2 by Moody's

Moody's downgrades Zions Bancorporation, National Association's ratings (long-term bank deposit ratings to A2 from A1); outlook

Moody's downgrades Comerica Incorporated (senior unsecured to Baa1 from A3)

Moody's downgrades Associated Banc-Corp (subordinate to Baa2 from Baa1); outlook stable

Moody's downgrades UMB Financial Corporation (issuer rating to Baa1 from A3); outlook stable

Moody's downgrades Bank of Hawaii Corporation (preferred stock to Baa3(hyb) from Baa2(hyb))

KeyCorp Outlook to Negative by Moody's; L-T Rating Affirmed

EM

X-S&PGR Affirms Sri Lanka Ratings; LC Rating Outlook Negative

X-S&PGR Upgrades Tata Motors, TML Holdings to 'BB'; Otlk Stbl

MHP: S&P upgraded to CC/negative from D;

S&P affirms Egypt's credit rating at B/B, lowers its outlook to negative from stable

Benin Affirmed at B+ by S&P

*TRADING*

Credit trading finally exits the Dark Ages | Financial Times (ft.com)

I thought this was a good piece talking bout the advances in E-Trading written by Steven Zamsky, a former head of global credit trading at Morgan Stanley. Extract

The long-fitful growth in the portion of trading volumes conducted on electronic venues has surged since the pandemic, and now stands at around 40 per cent in the US. As one trader puts it, “it’s as if everyone working at home suddenly decided to trade credit electronically”. And it stuck, even if WFH is fading.

Tradeweb Markets in talks to acquire Australia's Yieldbroker for AUD 125M - TW

Extract - “Tradeweb is in advanced discussions to acquire Yieldbroker, a leading Australian government bond and interest rate derivatives trading platform covering the institutional, wholesale, and primary markets. Tradeweb anticipates that the acquisition would be an all-cash transaction with a purchase price of AUD 125 million.

Barclays FICC Trading Highlights from Q1

Extracts:

Barclays Corporate & Investment Bank delivered second best quarter on record

Global Markets income of £2,492, down 8%, against a record prior year comparator FICC up 9% driven by strength in credit

Source: Barclays Investor presentation

CEO: Coming back to markets, I would say two things. As far as the first quarter goes, it was a case of great volatility in fixed income markets both before March and in March, right? So if you remember in the early part of the year, interest rates started rising, and then there was a big view that actually that things were going to, that the Fed was going to stop making, having interest rate rises after a certain point. And there was a bunch of sort of, shall we say, bearish trades on rates and bullish trades on spreads in January.

That reversed in March. So you see volatility. But I think the important thing that I would like to say about our fixed franchise is that our market share has continued to grow in that franchise and as it has in equities over a number of quarters and years based on deepening client relationships, investment in technology, investment in people, right?

So I expect as we go forward in the next quarter and the one after that for that market share to be sustained if not to grow and we did well in the first quarter of this year. We did and the second quarter I would also remind you that Q2 of '22 was a very strong point of comparison with the volatility that you had post Russia-Europe. I mean so far we have not seen that in this quarter.

So diligent work! Thank you

Awesome summaries across the board -- thanks for providing so much detailed information!