19 August 2022 Global Credit Wrap

Rates vol returns, more Ch11 filings, EM idiosyncratic news

*TL;DR

MACRO:

Fed pivot chatter was largely faded this week as Gov bond yields rose

Dollar had its strongest week since April 2020

10 Year UST approaching 3%, after 40bps widening since end of July

2 year Gilt +46bps just this week

2 year bund +55bps mtd

More inflows into Credit this week

INFLATION:

Slowing in the US while EUR / UK continue to suffer high levels of inflation

UK CPI came in at a 40 year high.

Changes in UK RPI have direct impacts on things like London Tube fares.

5D MOVES:

Rate move +risk off resulted in many bond ETFs losing 2% or more

HY / DISTRESSED:

Cinemas: Cineworld said to file for Ch 11, meanwhile AMC Ape prefs set to start trading

RCL borrowed money for 2nd time in a matter of weeks via HY market

SAS Airlines - Apollo wants to lend a DIP loan, set to extract juicy terms

EM:

Big hope for China stimulus after poor data this week

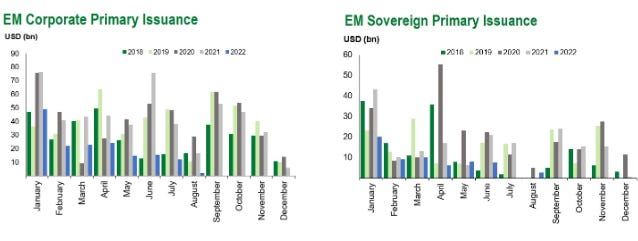

EM issuance continues to be subdued

Turkey cut its rates by 100bps, while Uruguay and Ghana hiked

European banks restart Russian bond trading according to the FT

Pakistan $ bonds rallied on IMF bailout bonds + EM beta rally

Colombia economy grew 12.6% in second quarter ahead of expectations

MENA Corps - HKN Energy reports net cash position + Brooge Energy possible take private

PRIVATE CREDIT:

Blackstone Private Credit - Q2 highlights

RATINGS:

Country Garden and Sino Ocean downgraded to Junk by Fitch

CREDIT TRADING:

European CDS sees busiest start to August since 2013

*MOVES OVER 5D*

FX - Dollar +2.3% this week which one bank highlighted was the biggest move since April 2020. Meanwhile EUR and AUD weakened on the week.

Rates - Material widening in UK Gilt yields over the week: 2y +46bps to 2.5%, 5y +34bps to 2.26% 10y +30bps to 2.41%. Short dated Bunds also put in wider moves (2y +28bps, 5y +28bps). German 2y has risen more than 50bps this month. The moves in Gilts and Bunds contrasted to US Treasuries where the short end was largely unchanged but the 5 to 10 year parts of the curve widened just short of 15bps each. 10 Year UST flirted with the 3% level but ended the week just short of it (Sidenote: lot of equity guys seem to focus on UST @ 3% for impact on S&P 500 levels…)

CDS Indices - Reasonable widening in Credit indices; Xover +62bps, CDX HY +50bps and CDX EM +42bps, CDX Sub Fin +25bps.

Cash Credit spreads - Most notable moves were EM HY +28bps and USHY+23 bps to +432. US HY spreads are still below +500bps but European HY is wider at +537bps. The differential in spreads is evident in the lagging issuance in European HY markets compared to US HY.

Bond ETFs - A tough week for Bond ETFs overall with many that I follow posting losses of minus 2% or more over 5 days. Worst performers were: EMB, IGLT, IHYG, EMLC, IEAC, JNK, HYG, LQD, TLT, EHYB. The sell-off in rates appears to be the main cause along with some credit spread widening. Interestingly AT1 (Invesco AT1 Capital Bond ETF) is up 1.3% over 5 days, showing some decent outperformance.

*MACRO*

Jackson Hole Symposium takes place 25-27 August

Could be a source of volatility this week in case there are “off-cycle” comments from Fed Chairman Powell. Previews:

Fed's Bullard tells WSJ he's considering support for another large rate hike (75bps?)

10 Year UST approaching 3%, after 40bps widening since end of July

BoE announces Corporate bond sales target of £200m per week..

It is set to start on the 19th of September and joins the ECB and the Fed in retrenching from their direct involvement in Credit Markets. More details here.

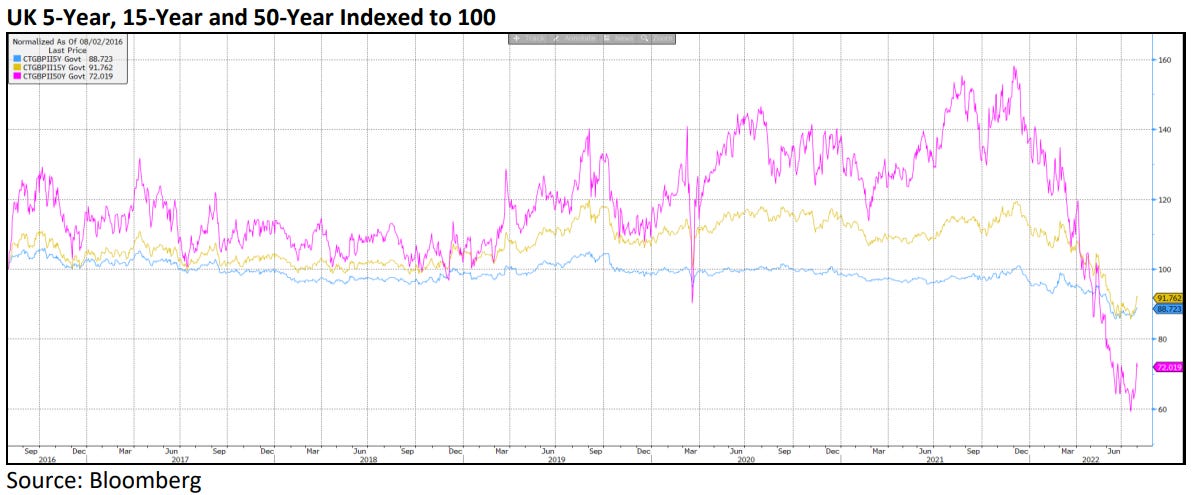

UK Real Wages Plunge Most on Record - BBG

UK long dated Index Gilts have lost 62% since the peak in late 2021 - Patronus

Norges Bank hiked 50bps as expected to 1.75%

Australia Surprisingly Sheds Jobs, Giving RBA More Flexibility - BBG

Extract: Australian employment unexpectedly dropped in July, giving the Reserve Bank scope for a more flexible approach in its tightening cycle. The economy shed 40,900 roles from a month earlier, confounding expectations for a 25,000 gain, statistics bureau data showed Thursday. The surprise reduction sent the Australian dollar and government bond yields lower.

Lipper flows showed more inflows for IG/HY and Loans this week

Loans broke a 9 week run of outflows too.

*NEW ISSUES*

Decent bump in US perps issuance this week after a long dry spell

Issuers that came to market included: Key Corp, PNC, Prudential, and Morgan Stanley

Financials continue to be active issuers with over 80% of issuance in Europe

Credit Suisse issued short date senior USD paper for the second time in 2 weeks

Royal Caribbean raised more money but this time in the HY market

After initial price talk of around 12%, RCL raised 5NC2 bonds at 11.625%.

They had only recently raised money from the Convertible bond market to pay near term maturities. Seems RCL’s Treasurers were making use of tightening credit spreads in their paper to issue new bonds. E.g. its existing RCL 7 ½ 10/15/2027 bonds have tightened in ~400bps vs July wides.

Russia’s Polyus looks to raise a 5 year CNY denominated bond at 4.2%

*INFLATION*

Grocery prices in Great Britain rise 11.6% as inflation hits highest level since 2008 - Guardian

Basics such as butter, milk and poultry show biggest increases.

UK CPI - In pictures

In the UK, nearly 600k customers have cancelled their Amazon Prime subscription in the second quarter of 2022 as the company prepares for a price hike on its streaming service, the Telegraph reports. Ladbible.

As ECB mulls another big hike, Schnabel says inflation outlook hasn’t improved - RTRS

Extract: “The euro zone inflation outlook has failed to improve since a July rate hike, European Central Bank board member Isabel Schnabel said, suggesting she favours another large interest rate increase next month even as recession risks harden.”

Wheat sinks to lowest price since early 2022 - Successful Farming

Extract as of 18 August 2022: “CBOT wheat has sunk to its lowest price since last September and is down 32¢ from the last market close. KC wheat is 38¢ down and hasn't had a price lower since early in 2022.”

If these lower prices successfully make it to nations that are big consumers of wheat, this could be positive for large parts of EM.

*FINANCIALS*

UK banks on firm footing after strong Q2 interest income growth: S&P Global

Extract: “The U.K.'s biggest banks can weather a weakening economic environment, supported by strong second-quarter revenues driven by rising rates, according to analysts. Aggregate net interest income, or NII, at the country's four biggest banks — HSBC Holdings PLC, Barclays PLC, Lloyds Banking Group PLC and NatWest Group PLC — reached its highest level since the first quarter of 2020, S&P Global Market Intelligence data shows, due to multiple central bank rate hikes since December 2021.”

Life Insurer Phoenix reports cash generation at upper end of target - Release

Strong first half cash generation of £950m in H1 2022 (H1 2021: £872m);

Now confident of delivering at the top-end of our £1.3bn-to-£1.4bn target range for the year

Fitch leverage ratio reduced to 27% at 30 June 2022 reflecting active deleveraging (FY 2021: 28%).

Phoenix manages a high-quality c.£34bn shareholder credit portfolio, which is 98% investment grade and with only 19% in BBB; our exposure to cyclical sectors is low at only c.3% and high quality with an average credit rating of A-.

Phoenix has no material exposure to inflation, with our key product and cost exposures hedged.

Assets under administration decreased to £269bn as at 30 June 2022 (FY 2021: £310bn) due to £38bn of adverse market movements..

Bank of Cyprus Rejects Takeover Proposals From Lone Star - BBG

*CHINA*

China Summary - There are big hopes and dreams about what China might do with regards to stimulus to restart the economic engine. Earlier in the week there were misses on retail sales, industrial output data and youth unemployment ticked up to 19.9%, which the media reported was a new all time high. On the property/credit side; home prices slid for an 11th consecutive month and lending data showed falls in new yuan loans in July. China applied a 10bps rate cut to its 1yr MLF rate and 7-day Reverse Repo rate. Economists polled by BBG expect the one-year loan prime rate - the de facto benchmark lending rate for banks to be cut by 10bps to 3.6%, That would be the first reduction in that rate since January 2022. Better quality China Property issuers rallied in the week but the mood was tempered by a profit warning and a rating downgrade for Country Garden and then Sino Ocean.

Moody's – China's AMCs to provide selective support to property sector given capital and commercial factors

Extract: Moody's expects AMCs to support the sector mainly through investing in property projects that face liquidity issues instead of providing direct financing to distressed property developers. AMCs can set up real estate funds with third-party investors or use their own funding to support unfinished property projects. Regulators encourage AMCs to support the property sector by expanding the scope of assets that AMCs can acquire and lowering the risk weight for these acquired assets.

*EM*

EM issuance continues to be subdued (Gramercy Chart)

Uruguay Central Bank raised rates for 9th consecutive month (+50bps to 10.25%)

Bank of Ghana increased its policy rate by 300bps to 22.0%.

Sri Lanka kept its key lending rate on hold at 15.5%

Turkey cut its rates by 100bps, some takes from EM Twitter

Egypt's central bank governor resigns a year early - RTRS

IMF to visit Sri Lanka in late August: CBSL Chief - Newsfirst

Extract: “Central Bank Governor Dr. Nandalal Weerasinghe said on Thursday that an IMF Mission is expected in Sri Lanka later this month. "The IMF mission is planning to come here towards the end of the month, with an intention to complete and reach a Staff-Level Agreement on the Policy Package," said the Governor adding that thereafter Sri Lanka will start approaching the creditors on restructuring its debt.”

Pakistan Assets Rally Amid Bets for IMF Bailout This Month - BBG

Extract: “[Pakistani] Dollar denominated bonds due in December 2022 were indicated at about 95 cents on the dollar on Tuesday from a low of 85 cents in July, as investors turn more confident the debt will be repaid. The rupee surged 11% this month to 213.87 per dollar as of Monday, the biggest gainer in the world.“

Pakistan has adopted austerity measures to win approval from the IMF to resume its stalled bailout package….Fitch Ratings and Moody’s Investor Service said in late July they expect the nation to secure $1.2 billion from the IMF, while Saudi Arabia is said to renew its $3 billion deposit in assistance, easing financing pressure on Pakistan.

There were larger moves in longer dated bonds like the Pakistan 2031s which rose nearly 20 points from lows seen in middle of July. A key difference between Pakistan and Sri Lanka appears to be the number of nations still willing to lend money to Pakistan (e.g. Saudi Arabia) and the more advanced state of debt distress in Sri Lanka.

Colombia economy grew 12.6% in second quarter, beating expectations - RTRS

Turkey based Pegasus Airlines reported strong figures - Report

Total cash reserve grew to €789mn as of 2Q22-end, primarily supported by the cash generated from operations

2022 estimated jet fuel consumption is hedged by 46% between $60-78 bucks (Brent equivalent).

2Q22 EBITDA reached EUR104mn on 20.6% margin compared to EUR14mn (9.0% margin) in 2Q21.

Pegasus sees a significantly improved outlook for operating profitability in the remainder of the year

…2022 EBITDA is now foreseen to surpass the 2019 figure, with EBITDA margin reaching ‘around 30% level

Brooge Energy: Majority Holder Interested in Taking Co. Private (announcement)

The Midstream oil storage and service provider located near Fujaira in the Middle East has seen its main shareholder look to take the company private.

HKN Energy (Kurdish E&P) 1H22 results - Enters net cash position

Similar to other E&Ps that have reported in the region for H1 2022, HKN sat on a net cash position. Other highlights:

80% increase in operating revenues y-o-y

EBITDA adj. came in at USD 179m,

Beat driven by increased average production, high oil prices and low-cost structure. Cash and cash equivalents totalled $292m vs debt of $149m.

*ESG*

EDF Plans Green Financing Framework Global Investor Call - BBG

*PRIVATE CREDIT*

Blackstone Private Credit Q2 - Highlights

Total Investment income of $1.29bn vs $0.15bn in 6m ended June 2022, mainly due to increased deployment

Investment portfolio fair value grew from $11.3bn to $46.2bn

Percentage of debt investments at floating rate, at FV: 99.6%

FV of debt investments decreased 1.9% in the half YoY

The Fund’s portfolio is 96% senior secured with an average loan-to-value (LTV) of 43% and an average issuer EBITDA of $167 million(

During the quarter, the Fund had zero defaults

Highlighted transactions - lender to Unified Women's Health and Zendesk

Sources: 10q and Portfolio commentary July 2022

*RATINGS*

Glencore's long-term rating was affirmed by S&P at BBB+, outlook positive

Fitch upgrades Ukraine to CC

Ukraine Upgraded to CCC+ by S&P, Outlook Stable

Ecuador: S&P affirmed the B- rating, outlook stable

Jordan Affirmed at BB- by Fitch

Oman Upgraded to BB by Fitch, outlook stable

S&P has downgraded Sri Lanka’s rating from CC to D on four bonds

X-S&PGR Revises Tullow Outlook To Negative; Affirms 'B-' Rating

China Property - Two new fallen; Angels Sino-Ocean & Country Garden:

Fitch Downgrades Sino-Ocean to 'BB+'; Ratings on Negative Watch

Fitch Downgrades Country Garden to 'BB+'; Maintains Rating Watch Negative

*HY/CONVERTS*

Cruise liners report positive data

Carnival said Tuesday that Carnival Cruise Line's booking activity for Monday was nearly double the level for the equivalent day in 2019 after it revised pre-cruise COVID-19 vaccination and testing requirements to allow more guests to sail. Also seems to be some positivity from Tui Cruises too. Maybe that’s why RCL and CCL were in the market this week to issue/re-term their debt.

Just Eat Takeaway Sells IFood Stake to Prosus for Up to EU1.8B

Just Eat’s 1.25% convertibles are up ~ 20 points from the July lows to trade just above 80 now. Just Eat’s had also planned to sell part of Grub Hub, but instead the stake sale of IFood seems to have pleased the market. Just Eat’s top shareholders include Activist Cat Rock and Baupost.

*DISTRESSED*

Airline SAS secured $700m of DIP Financing - Release

This news is interesting for a number of reasons:

SAS effectively filed for Chapter 11 due to surging labour costs for Pilots

SAS’s competitors probably thought that it was done for when it filed for Ch11

Apollo is the party looking to lend funds to SAS as a part of the DIP Financing

Looking through the release, it seems Apollo are set to make money in a number of way due to the proposed transaction structure (not an exhaustive list):

“Loans under the DIP Facility will bear interest at a rate pa equal to adjusted term SOFR plus 9.0%, payable in cash or in kind at the borrower’s election, which maybe increased by 2.0% pa during the continuance of any event of default under the DIP Term Loan Agreement

The DIP Term Loan Agreement requires the payment of certain fees to Apollo on the Closing Date; an upfront fee of 1.0% of the Total Aggregate Commitment, an advisor fee of 1.0% of the Total Aggregate Commitment, an unused commitment fee of 2.0% of the unused amount of the Total Aggregate Commitment per annum and an initial work fee of USD 1 million….” and the list goes on!

For non credit people, some of these terms are akin to how Warren Buffet made money out of the bespoke preference share investment in Goldman Sachs during the GFC.

AMC - “APE” Preferred stock set to start trading Monday

Reminder: these are the preferreds that CEO Adam Aron said could be used to help de-leverage the company. This is what Aron said on 4 Aug:

“The dividend of AMC Preferred Equity units exclusively to our shareholders in our opinion is perhaps the single biggest action we will take in all of 2022 to fundamentally strengthen AMC for the long term. This new AMC Preferred Equity gives AMC a currency that can be used in the future to strengthen our balance sheet, including by paying down debt or raising fresh equity.”

Cineworld - Said to file for Chapter 11 according to WSJ

In stark contrast to AMC, the second largest Global Cinema Chain Cineworld is said to file for bankruptcy according to the WSJ. Here are some key figures from its last Annual Report:

What is not included above is the claim from rival firm Cineplex for $1bn (which Cineworld is disputing) and lease liabilities of $4bn. Debt for Cineworld comprises Term loans, RCF, Private Placement loan and Convertible bonds. The news of a potential filing follows an announcement from Cineworld earlier in the week (extract):

…the Group has been taking proactive steps to ensure it has the balance sheet strength and flexibility to adapt to market conditions. This includes significant previously disclosed operational and financial initiatives to manage costs and enhance liquidity. The Group believes these steps are required to optimize its ability to maximize enterprise value as part of the recovery in the cinema industry. In connection with these initiatives, the Group remains in active discussions with various stakeholders and is evaluating various strategic options to both obtain additional liquidity and potentially restructure its balance sheet through a comprehensive deleveraging transaction. Any deleveraging transaction will likely result in very significant dilution of existing equity interests in Cineworld.”

Key phrases here are “deleveraging transaction", “additional liquidity” and “restructuring” of its balance sheet.

The WSJ then said this later on in the week:

“The London-based cinema company has engaged lawyers from Kirkland & Ellis LLP and consultants from AlixPartners to advise on the bankruptcy process, these people said. Cineworld is expected to file a chapter 11 petition in the U.S. and is also considering filing an insolvency proceeding in the U.K., they said”

Cineworld is a name that is much less understood by market participants compared to AMC. The latter benefits from a high-profile and (generally) highly regarded CEO, ratings agency reports for its HY debt and an army of Apes on Reddit! Cineworld is a listed stock and has equity analyst coverage, but they don’t tend to understand the debt aspects of the business well.

There are a number of interesting dynamics to this situation:

The $1bn legal claim from failed takeover target Cineplex (and what happens to this in a Ch11 scenario).

Large shareholdings by the founders - Mooky and Israel Greidinger via the “Global City Theatres B.V” entity

Recent financing in the Cinema sector:

Vue Cinemas lenders took full control of the biz - Vue’s 1st lien lenders took 100% equity ownership of the business. Under the new deal, around £465 million of debt will be converted into equity. The recapitalization will help Vue raise £75 million of additional liquidity.

AMC’s The 10Q report had a snippet about possible refinancing of its 11.25% Odeon Term Loan

The official filing of the Chapter 11 should reveal more details around why the firm is filing and what their objective is. As a side note, once confirmed, Cineworld’s Ch11 filing will add to the bankruptcy stats for 2022.

*CREDIT TRADING*

European banks restart Russian bond trading according to the FT - RT

Extracts: “UBS, Barclays and Deutsche Bank have all reportedly resumed allowing clients to sell their Russian debt holdings.” …The sources explained that the decisions to restart Russian bond trading had not been motivated by trying to profit from the reopening of the market, but instead were intended to allow clients to wind down their exposure in accordance with sanctions rules. “This is chiefly for clients who continue to want to unwind,” an unnamed employee of one of the banks that has restarted Russian debt trading told the outlet. “The volumes aren’t that remarkable,” he added. In July, the US Treasury published guidelines that allowed US banks to facilitate, clear and settle transactions with Russian securities if it helped US holders to gradually dispose of them.

European CDS sees busiest start to August since 2013 - BBG

Extract: “Almost 120 billion euros of iTraxx Europe and Crossover index contracts changed hands in the first half of this month, based on Depository Trust and Clearing Corporation data compiled by Bloomberg. Volumes in that two-week period were almost double the 10 year average.”

*LINKS*

Pimco’s Dan Ivascyn interview with Advisor Perspectives - Advisor perspectives

“The case for EM Corporates in today’s dislocated markets” - Gramercy

Pictet - More pain ahead for credit

(Editor: Read beyond the title, its actually not a bad short read).

Global Monetary tightening - Charted

Lev loan fundamentals

Is Private Credit a Bubble, or Just a Little Frothy? - II

Decent article, leans on side of Private Credit.