12 August 2022 - Global Credit Wrap

Inflation reduction acts, EM + HY strength, private credit presence growing...

*TLDR*

MACRO:

Markets currently running high on the premise of a) a recession being pushed back due to last week’s strong NFP print and; b) lower than expected inflation readings on three different US indicators this week (PPI, CPI, Import prices).

Fed survey signaling tightening of financial conditions, while GS FCI data says tightening is not enough compared to where inflation is..

Corporate confidence seems to be running high with M&A volume registering the highest monthly total YTD in August

Some corporate earnings were signaling recessionary trends:

Advertising slowdown (as cited by likes of Roku, Warner Brothers, Paramount)

US Semiconductor firms warning (e.g. Nvidia and Micron). However note that Taiwan Semi (TSMC) reported an encouraging 50% increase in July sales YoY and Lenovo saw net income rise due to non-PC segments

UK macro seems particularly bleak due to a combination of the high cost of energy prices, possibility of drought-induced power shortages, rising household energy debt, a number of key worker unions striking (Felixstowe port, rail, tube, bus and postal workers, list goes on..) and the political uncertainty due to potential new leader Liz Truss's threatening to interfere with the BoE's mandate.

INFLATION:

A number of countries are now enacting “inflation reduction acts”

US consumer inflation expectations are falling

A number of property markets outside of the US are seeing slowing of growth - e.g. Sweden, Toronto and possibly even the UK

Ryanair CEO says budget flights are gone forever

HY/DISTRESSED:

US HY bonds are headed toward the sixth straight week of gains - BBG

More companies filing for Chapter 11, entering restructuring or discussing capital structure changes to deal with change in business circumstances.

EM/CHINA:

Standout week for EM risk assets, particularly high yielding EM

Meanwhile, China junk bond prices hit new record low

Ukraine's creditors agree on two-year freeze on $20-bn overseas debt

Kurdish oilcos keep pumping out cash (DNO/Shamaran reported this week)

RATINGS:

Moody's chopped Cruiseliner ratings - Carnival and Royal Caribbean

PRIVATE CREDIT:

Apollo mgmt reckon private credit could potentially replace 10% to 15% of the roughly $3tn market for HY loans and bonds

Brookfield stated that it is keeping its portfolio in a short duration and highly liquid position and finished the quarter with a record $111bn in unspent capital.

*WEEKLY MOVES*

CDS Indices - “Risk-on” evident in CDS indices moves: Xover (-56bps), CDX HY (-43bps), CDX EM(-37bps), Sub Fin (-25bps). The rally sparked a comment from highly successful HF Manager Boaz Weinstein, who made huge returns in 2020 after buying CDS of mispriced HY CDS single names. He was also famous for being on the other side of the JPM London Whale Trade.

Cash credit spreads - EM led the way here with HY sovereigns/credits taking off this week. EM HY (-54bps), EM Agg(-23bps), Euro HY (-21bps), US HY (-19bps), US IG (-9bps). US IG cash spreads look like they are trending towards pre Russia invasion levels (~120bps area vs ~132bps area currently). The “ski-slope” type decline in US HY spreads is notable (from 583bps in early July to 409bps this week), especially when framed against a backdrop of tightening financial conditions and a number of slowing economies. Spreads on $ Bank CoCos in aggregate were flat on the week.

Bond ETFs - TLT -2.37% and IGLT -1.8% were notable underperformers in a risk on week. Outperformers were Local EM Bond EMLC +2.29%, JNK +1.15%, Corporate EM Bonds CEMB +1.12%, HYG +1.06%.

*MACRO*

US semis cut guidance (NVIDIA, Micron) but Lenovo and TSMC figs better

Nvidia cut its revenue guidance for Q2 by $1.4bn and trimmed its gross margin guide:

Extract from Saxo Bank: “A little more than two months ago Nvidia announced FY23 Q1 results showing record revenue, but today the graphics card maker is pre-announcing Q2 results cutting its gross margin (GAAP) guidance for the Q2 quarter (ending 31 July) from 65.1% to 43.7% and expected revenue of $6.7bn compared to previously announced $8.1bn. The shortfall in revenue is driven by its gaming segment which Nvidia is saying is impacted by the macroeconomic backdrop. The fall in demand in its gaming segment has also meant that Nvidia has too much inventory and has been forced to adjust prices. The company is therefore booking a $1.3bn inventory write-down.”

Micron comments spark sell off in its shares, but recover towards the end of the week:

Micron Said Q4 Revenue May Come in at or Below the Low End of the Revenue Guidance Range Provided in its June 30 Earnings Call

Micron Technology, says expectations for CY22 industry demand growth for DRAM and NAND have declined since June 30, 2022 earnings call

However, TSMC and Lenovo seemed to reports read better

Advertising Slump Spreads To TV Networks, Publishers -WSJ

Extracts: “Warner Bros. Discovery Inc., home of cable channels including CNN, TNT and the Food Network, on Thursday cut its outlook for this year and next in part because of a slowdown in advertising

Roku said it expects its advertising business to come under further pressure during the second half of the year.

Paramount Global on Thursday said revenue at its TV operations -- its biggest business, which includes such units as CBS, MTV, Nickelodeon and Comedy Central -- was essentially flat in the latest quarter, partly because advertising slid 6%.

New York Times Co. on Wednesday posted its first decline in digital advertising revenue since 2020, due in part to the macroeconomic environment.

Gannett Inc., the publisher of USA Today and a raft of local newspapers, posted a 8.7% drop in revenue from advertising and marketing services and cut its profit outlook for the year in part because of industrywide headwinds in digital advertising, as well as rising costs.”

US Bank lending standards see sharp tightening - Fed

Source: Wayne Wennick on Linkedin

However, GS FCI shows financial conditions are too loose compared to where inflation is…

Source: Wayne Wennick / Linkedin

*UK*

UK household energy debts reach all-time high of £1.3bn ahead of winter price cap hikes - City AM

Extract: “Household energy debt is standing at an all-time high of £1.3bn ahead of expected bill hikes this autumn, according to new research from Uswitch, the comparison and switching service. This is nearly three times higher than it was in September last year. Six million homes – almost a quarter of households (23 per cent) – owe an average of £206 to their energy provider this summer, which is a 10 per cent increase in just four months from April, when the average debt was £188. Traditionally, this would be a time of year when bill-payers would expect to have built up a war chest to cope with winter bills, making the debts more alarming.”

UK Felixstowe port workers to strike after talks fail - despite raise and £500 bonus

Extract from BBC - “Workers at Felixstowe, the UK's largest container port, will go ahead with an eight-day strike after pay talks broke down. Around 1,900 members of the Unite union will walk out on 21 August after rejecting an offer of a £500 lump sum on top of a 7% pay rise.”

New Car registrations fell in the UK in July - SMMT

UK new car registrations fall -9.0% to 112,162 units as supply chain shortage continues to frustrate order fulfilment. Read more here.

Yields on GBP-denominated IG credit had risen almost 250bps to 4.5%, their highest level for a decade - BBG

*INFLATION*

This week, CPI, PPI and import prices all came in below expectations

Bespoke Research summed the week’s inflation data up quite nicely:

“It doesn’t happen that often, but bulls hit the inflation superfecta. It started with Monday’s release of the July Survey of Consumer Expectations which showed a continued decline in inflation expectations. On Wednesday, the big bad CPI report for July was released and that came in lower than expected for a change. The weaker-than-expected CPI was followed by a weaker PPI Thursday and then a weaker-than-expected report on Import Prices Friday. After months where it seemed as though every inflation report was coming in hot, this week’s data on prices was cold, cold, cold, and cold. The heatwave has been broken!”

A number of countries are now enacting “inflation reduction acts”

Its not just the US, France’s parliament adopted a €20 billion inflation-relief package, lifting pensions and some welfare payments, and allowing companies to pay employees higher tax-free bonus payments, in a bid to boost household purchasing power. More from Euronews here.

Americans' expectations for future inflation plunged in July - Axios

Note that this was before the CPI data was released on Wednesday.

Gas prices in U.S. fell below $4 per gallon average for first time since March

The fall in gas prices likely contributed to US consumers’ inflation expectations above. Yahoo Finance discusses the fall in gas prices further.

Stockholm Apartment Prices Fall Most Since Pre-Covid Era - BBG

The era of heavily discounted flights has come to an end, according to the boss of Ryanair - Travel Radar

UK - Online campaign “Don't Pay” gains momentum as 100,000 pledge to cancel energy bill direct debits - Sky

Egg Prices in US Jump 47% as Food Inflation Soars, IRI Says - BBG

In the UK, air fares in the first week of August, were up 30% on average for the top 36 routes compared with pre-pandemic levels - Kayak via BBG

Ford Increasing Prices of F-150 Lightning Models

*FINANCIALS*

UK / European Financials continue to call their bonds

This week € HSBC 5.25% AT1 and £ Hastings 3% 2025 were both called. Recall that HSBC did not see itself issuing any further AT1 in 2022. Hastings is a UK general insurer that got taken over by Nordic Insurance Group Sampo. Presumably Sampo can refinance cheaper, hence the call.

Senior $ issuance hums along at 5-6% area in USD

Credit Suisse issued a series of senior non preferred paper including a 2026 bond at 6.3% yield. Meanwhile Santander issued 2025 and 2027 bonds both with 5%+ coupons. Traditionally an unexciting area of the market, senior bank bonds are offering yields that sub financials were offering only a year or so ago…

New BNP AT1 was popular

Investment Grade rating (at bond level), large cap status, nearly 8% yield and solid reputation in European Banks sector saw a large book for BNP’s latest AT1:

The strength continued in the secondary with the bond closing 102.5/102.75 after being priced at par.

*DISTRESSED*

More debt distress noticeable despite headline rally in HY/EM

Certain companies that had been in trouble for a while announced Chapter 11 filings, debt restructurings and other similar actions this week. An assortment of these are outlined below:

Telco software company Avaya in battle to avoid a default - BBG

Extract: “Avaya’s debt and shares tumbled this week after the company said it had “substantial doubt” about its ability to continue as a going concern, delayed its financial results and reported a steep revenue drop.

The telecommunications software company has until mid-September to file the quarterly results before triggering an event of default under the loan, according to an estimate from CreditSights.

Creditors organized after Avaya sold a $350 million leveraged loan and a $250 million exchangeable note in late June, and weeks later predicted a sharp decline in its financial performance and ousted its chief executive.”

This last part seems nuts to me in that lev loans and a convertible were sold only in June, and shortly after they issued a profit warning. These sorts of occurrences should will likely increase the level of “professional skepticism” of the HY/Loan community when lending money in this environment.

Mexico’s biggest non-bank lender, Unifin Financiera, is halting bond payments and will restructure its debt - BBG

Extracts: “Unifin’s dollar bonds due in 2029 fell sharply to trade at about 10 cents from above 40 cents on Monday. The decision by Unifin comes as only somewhat of a shock to investors, who witnessed two other collapses by Mexican non-bank lenders -- Alpha Holding SA and Credito Real SAB -- within the past year. Still, money managers and analysts had been reassured by Unifin’s top leadership late last month that the company would seek alternative funding sources.”

Real Estate firm Corestate - exploring viable alternative refinancing solutions

Extract: “Management Board mandated specialized advisors in the second quarter to explore and advance a viable alternative refinancing solution jointly with a group of major noteholders”

Drugmaker Endo Says Bankruptcy Likely Imminent - WSJ

Extract: “The drugmaker has been in talks with lenders, but also faces thousands of lawsuits from government and private plaintiffs alleging it fueled opioid addiction”

Brookfield owned Altera Infrastructure files for bankruptcy

On August 12, 2022 (the "Petition Date") Altera Infrastructure FSO Holdings Limited filed a voluntary petition for relief under Chapter 11 of the United States Bankruptcy Code. Just last week, Tradewinds reported that: The company said it is in talks with secured lenders, with loans backed by its vessels to “better align terms of its debt with expected cash flows”. Those talks are focused on its business segments in floating production, storage and offloading units, floating storage and offloading units, towage vessels and units for maintenance and safety. Its shuttle tanker fleet was not listed in the asset-level finance talks.”

*HY*

Shipping/Container corner - Seaspan and Hapag Lloyd reported earnings

Seaspan key highlights (subsidiary of Atlas Corp):

Adj EBITDA of $273m on revenues of $413m represented a 5% increase q-o-q

Newbuilding program is already fully financed, and all vessels will commence long-term contracts with major liners.

No “new” news on the take-private proposal from Poseidon

Robust balance sheet with liquidity of $1.1bn, total borrowings to total assets of 51.2%

Approx. 70% of Seaspan's debt is fixed rate, protecting against an unpredictable inflationary and rising interest rate environment

Some of Seaspan’s Nordic HY bonds rallied on the potential prospect of the Investor put option being triggered at 101.0. Full H1 statement.

Hapag Lloyd’s H1 headline figures were exemplary (Revenue: €16.97B, +94% Y/Y - EBITDA: €10.00B VS €3.52B Y/Y). However its shares sold off on Friday after its management said that demand is easing but not collapsing and that ships are still oversubscribed just not as much. This article from Freightwaves was superb re Hapag Lloyd H1s and wider container demand.

*EM*

GBI-EM posted its second highest daily return in 2022 on Wednesday…

after the soft U.S. CPI print as EMFX rallied substantially. For context, the GBI-EM did not rally more than 1.2% on a single trading day in 2021. GBI-EM refers to the JPMorgan Government Bond Index-Emerging Markets. Source: Gramercy

Ukraine's creditors agree on two-year freeze on $20-bn overseas debt - Business Standard

Extract: “With no sign of peace or a ceasefire on the horizon nearly six months after Russia's invasion began on Feb. 24, bondholders have agreed to postpone sovereign interest and capital payments for 13 Ukrainian sovereign bonds maturing between 2022 and 2033. Ukraine said it would save around $5 billion over the next 24 months as it manages its dwindling financial resources.”

Kurdish oil companies DNO and Shamaran reported - Cash & Debt highlights

DNO - reduced its interest-bearing debt through a $200m bond redemption and exited the quarter with cash deposits of $801m. With $671m in bond and reserves-based lending debt, its net cash position stood at $129m. DNO does not hedge its oil production, so has likely benefited from full uplift in oil prices.

Shamaran -EBITDAX for Q2 2022 was double that of Q2 2021. Net debt position was well under one-time EBITDAX at the end of the first half of 2022.

Kosmos Says Phase One of Tortue LNG Project Is 80% Complete

Oil Storage firm - Brooge Energy says floods in the Port of Fujairah did not affect its facilities and they are secure - Statement

*CHINA*

China: trade surplus hit a record US$ 101bn last month as exports grew a surprisingly robust 18% YoY - BBG

China Junk USD Bonds Hit New Low - BBG

Average price fell to 56 cents on the dollar this week (BBG). Meanwhile, The median dollar-bond price of Chinese real estate firms bonds was 16 cents, versus 40 cents in March, with about 80% of issuance trading below 50 cents.

Builder Logan Group missed an interest payment which cross-defaulted into the $3.7bn debt stack

…and will increase default rates as $3.2bn of the debt was index-eligible. Source: Gramercy

*RATINGS*

Ukraine Cut to Default by S&P After Creditors OK Debt Delay

Fitch Downgrades Ukraine to 'RD'

Turkey Downgraded to B3 by Moody’s, Outlook Stable

Moody's chops Cruiseliner's ratings:

Moody's downgrades Royal Caribbean's CFR to B2; outlook is stable

Carnival Downgraded to B2 by Moody's, outlook is negative

X-S&PGR Lowers Kosmos Energy ICR To 'B' On Ghana Dwngrd, Outlk Neg

Coinbase Downgraded to BB by S&P

*PRIVATE CREDIT / BUYSIDE*

Apollo boasting its credentials in financing markets vs public credit

In its earnings call, Apollo made some insightful comments about how it is increasing its share of Debt Capital Markets:

Apollo handled 11 transactions of at least $1bn each this year through July 2022

The number of firms who can do $1 billion deals is shrinking - John Zito

Private credit could potentially replace 10% to 15% of the roughly $3tn market for HY loans and bonds, Zito said

Private Debt firms lend $2.5bn for Vista’s Avalara Buyout Deal - BBG

It is one of the largest funded by private credit this year

Firms - Blue Owl Capital, Apollo and HPS are among lenders for tax-software deal

Brookfield ended the second quarter with a record $111bn in unspent capital, or dry powder- WSJ

Other highlights from its earnings call on Credit:

“Purposely keeping our portfolio in a short duration and highly liquid position, maintaining approximately $25 billion of assets in the form of cash and liquid securities”

“Our $16 billion flagship opportunistic credit fund is moving to 80% invested or committed and we expect to start fund raising for the next vintage later this year…Accordingly, we are now in an excellent position to invest capital for value and drive outsized returns.”

“We have seen spreads widen and liquidity tightening in the leveraged loan market, we are seeing term premium come back across the capital stack in both new public issuances and the secondary market and we continue to see numerous private credit opportunities at much better returns than just 8 months ago.”

On Pension Risk Transfer (“PRT”) business: “we continue to scale our Canadian Pension Risk Transfer or PRT business. We have built this business over the last 6 years, growing to more than $3 billion in insurance assets….This year's activity included closing on the single largest PRT transaction ever completed in the Canadian market for approximately $1 billion. We expect to further grow our PRT efforts through expanding into the US and European markets. Editor: This is interesting since there are already some fairly well established PRT businesses in the UK like L&G, Phoenix, Aviva, PIC, Rothesay and so on

CLO Managers Need to Offload some Aging Loans - BBG

Extract: “Money managers bought billions of dollars of leveraged loans in the US and Europe earlier this year, expecting to package them into bonds. Now the value of the debt has dropped, and firms are struggling to find ways to offload it without taking big losses.”

*CREDIT TRADING*

Liquidnet results - Highlights from Q2:

“Credit revenue increased by 11%, outperforming the wider market, with total US corporate bond trading volumes decreasing by c.3% in H1 2022

Total MarketAxess Post-Trade Eurobonds volumes also declined, by c.17%

We believe Liquidnet Credit in the D2C market provides a meaningful opportunity for us.

Our objective, as articulated at our Capital Markets Day in 2020, is to achieve a 3% - 6% market share of total corporate bond trading by the third full year post completion.

Sidenote: TP ICAP ( Liquidnet’s parent company) shares are up 47% over 1 month to 13th August 2022.

Chart of Credit activity in H122 shows high growth in ETF and CDS volumes

Source: Wayne Wennick

*LINKS*

Money flowing back into Credit, will it sustain momentum into the rest of 2022?

Full Transcript of Pimco’s Dan Ivascyn Interview on Odd Lots Podcast - BBG

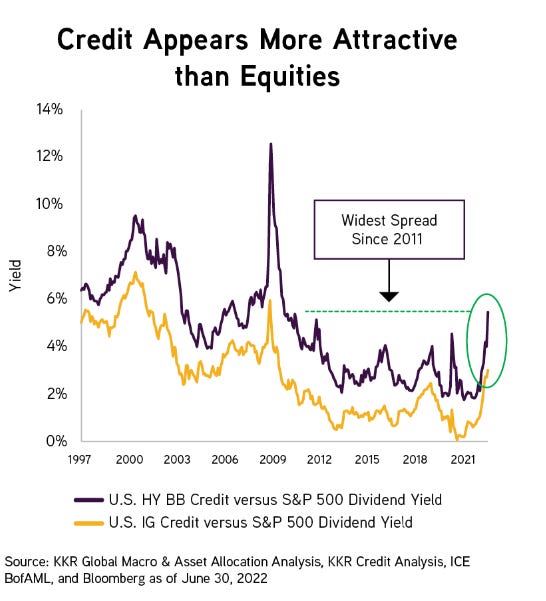

KKR asks the question “Why Credit now” in its latest publication - KKR

New lev loan deals are clearing at serious discounts - LCD News

Corporate confidence on a high in August, judging by M&A at least..